5 thoughts on the market’s tariff tantrum

U.S. Head of Investment Strategy

Market update

We won’t waste your time with a market update. It could be irrelevant by the time you are reading this anyway.

Spotlight: 5 takeaways from the tariff tantrum

Ever since “Liberation Day,” markets have been under pressure. In this week’s note, we wanted to share five of our most important takeaways.

1. Stock markets hate tariffs, for good reason. Tariffs are taxes that importers pay. They can either take the hit in their margins or share the costs with suppliers and consumers. The government siphons the cash. Even after President Donald Trump paused his “reciprocal” tariffs for 90 days, the duties left in place are at their highest levels since the Great Depression. Businesses are scrambling to adapt. Apple, the largest goods company in the world, chartered airplanes to transport 1.5 million iPhones from India and China to the U.S. before duties hit. Reasonable people can debate the pros and cons of tariffs. However, it seems clear that the proposed duties are antithetical to the business models of the multinational corporations that make up the U.S. stock market. Our rough math suggests that the high-teens effective tariff rate currently in place could wipe out most of the real economic and S&P 500 earnings growth that we expected this year. The hit could be worse for goods companies reliant on multinational supply chains. This matters for both the high tech (the semiconductor index is down over -20% so far this year) and the low tech (so is Yeti – the cooler company).

Work with an advisor

Our advisors can provide ongoing financial advice on how your portfolio can adapt to the changes in the market, your life and your goals.

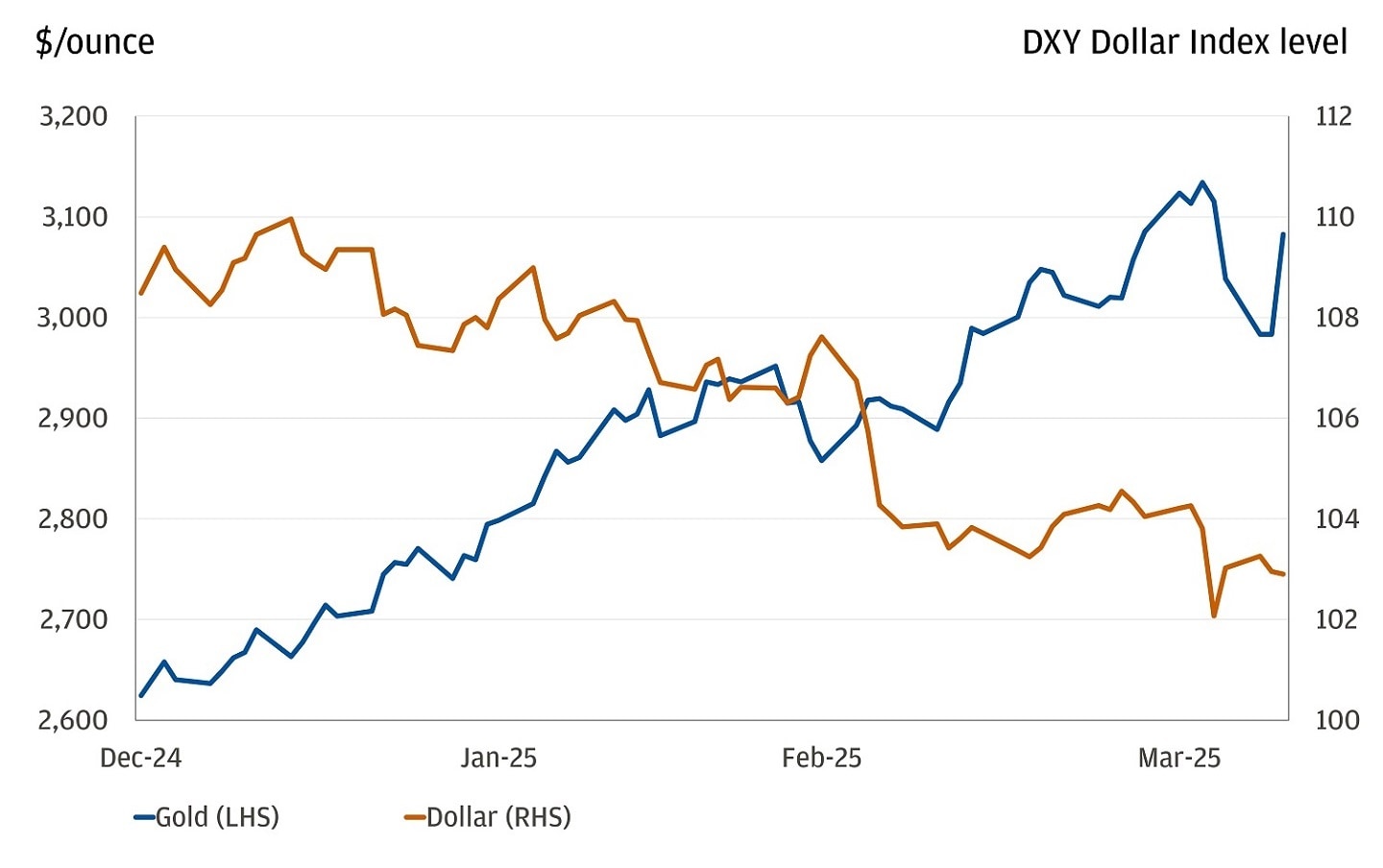

2. Global investors are asking questions about U.S. assets. What is the ultimate goal of White House trade policy? Will tariff revenue collected help to offset the nearly $6 trillion increase in the budget deficit that the House and Senate agreed on in the budget reconciliation process? Will regulatory and tax uncertainty curtail business investment and spending within the United States? Can the U.S. consumer power through the tariff shock? Does the return on investment of artificial intelligence (AI) capital spending still make sense given higher potential input costs of technology hardware, which is largely sourced from South Asia? When those questions get louder, it manifests as simultaneous poor performance from U.S. stocks, U.S. bonds and the U.S. dollar. Historically, the U.S. has had the lowest share of trading days where the currency, bond market and stock market all sold off across countries that we track. Last week, the dollar, Treasury bonds and the stock market all lost value. Global diversification seems like a prudent strategy, as does an allocation to gold.

The dollar is declining while gold gains

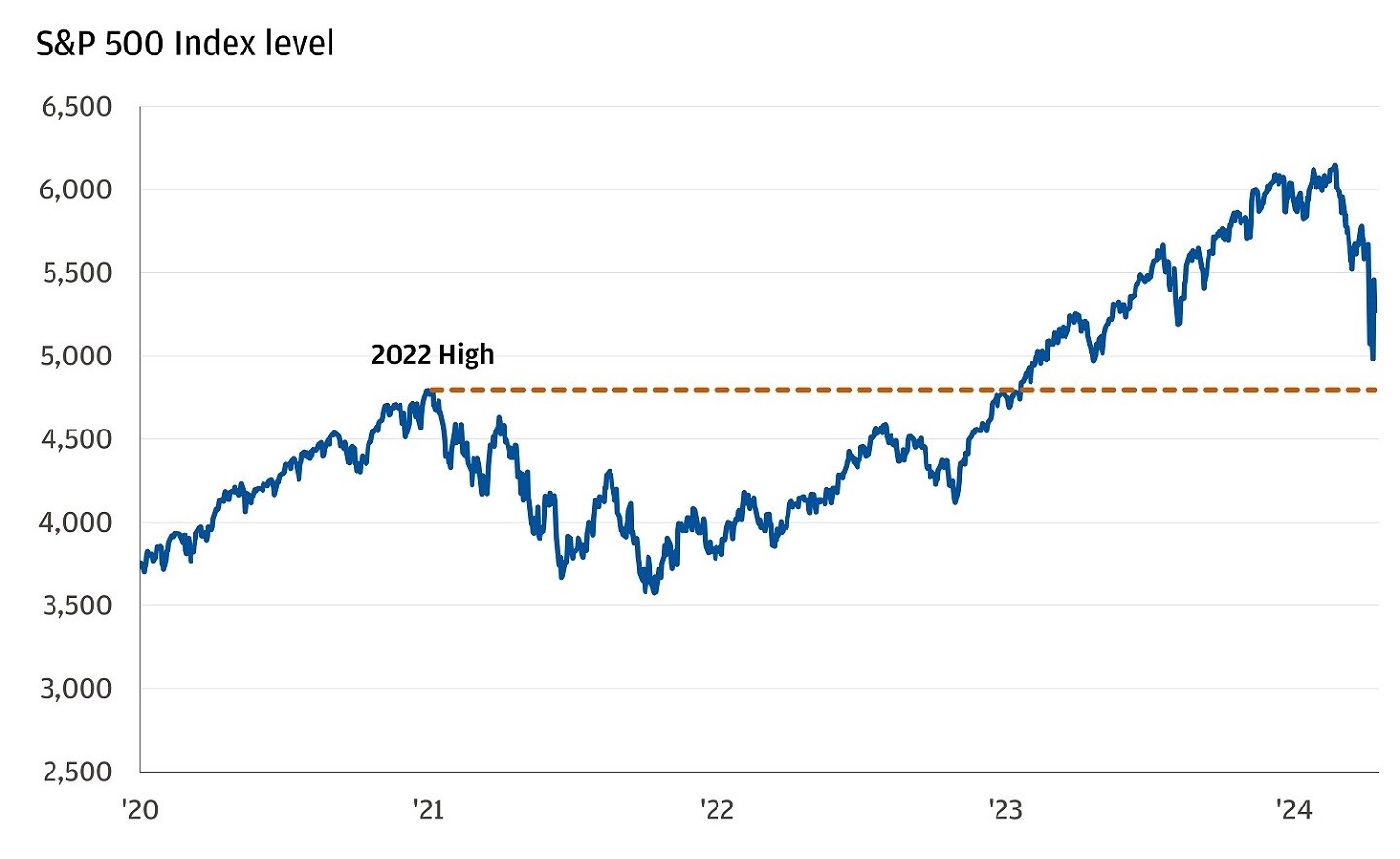

3. Market volatility can drive a policy response. Based on the commentary from the administration and subsequent reporting, it does seem like excess market volatility, especially in fixed income and currency markets, drove a policy pivot this week. Investors should remember that the tariffs are not codified into law. The administration is relying on the 1977 International Emergency Economic Powers Act (IEEPA) to levy these duties. There is already some speculation that this use case is illegal and would be struck down by the Supreme Court. However, legal clarity could take weeks or months and it seems like further market volatility would stimulate further de-escalation from the White House before the courts weigh in. The chances of further de-escalation or judicial intervention are why it doesn’t seem prudent to make wholesale portfolio changes with equities already down over 15% from peaks. Investors may root for a policy pivot, but they also have to focus on what the potential downside for stocks could be. It is encouraging that the S&P 500 tested the old highs (about 4800) from early 2022 and bounced during intraday trading. The next level of support could be at 4500, or about 15% below current levels. To get there, we assume that investors would apply an 18x trailing multiple (where previous troughs have been over the last 10 years) to the about $250 of earnings per share that the S&P 500 generated in 2024. Further, about 4500 on the S&P 500 would imply a about 30% peak to trough drawdown, which is consistent with the experience of past cyclical and event-driven bear markets.

The S&P is still holding up against the 2022 highs

4. Volatility creates opportunities across the risk spectrum. This week, we saw record activity from investors who trade on a tactical basis. Municipal bonds (a traditionally sleepy corner of the investment landscape by design) had one of their worst days on record on Tuesday. Forced liquidation from institutional holders generated the opportunity to buy bonds with nearly 5% coupons at par value. Activity among our clients was five to 10 times “normal” levels. We saw similar interest in equity linked structured notes. Right now, investors can potentially generate coupons of over 10% if equity markets are higher over the next 54 weeks, while potentially maintaining full principal protection down to a barrier 10% below current levels. This strategy allows investors an opportunity to increase market exposure without the full volatility of equity markets. Finally, we are looking for opportunities in both the banks and software space. Software valuations have corrected at a time when AI adoption could benefit from rapidly declining compute costs. Banks would benefit from a greater focus from the administration on the deregulatory agenda that should incentivize a handoff in borrowing from the public sector to the private sector. Opportunities also exist outside of markets. It could be an opportune time to consider a Roth IRA conversion, to gift to family members, to optimize asset location or to exercise stock options.

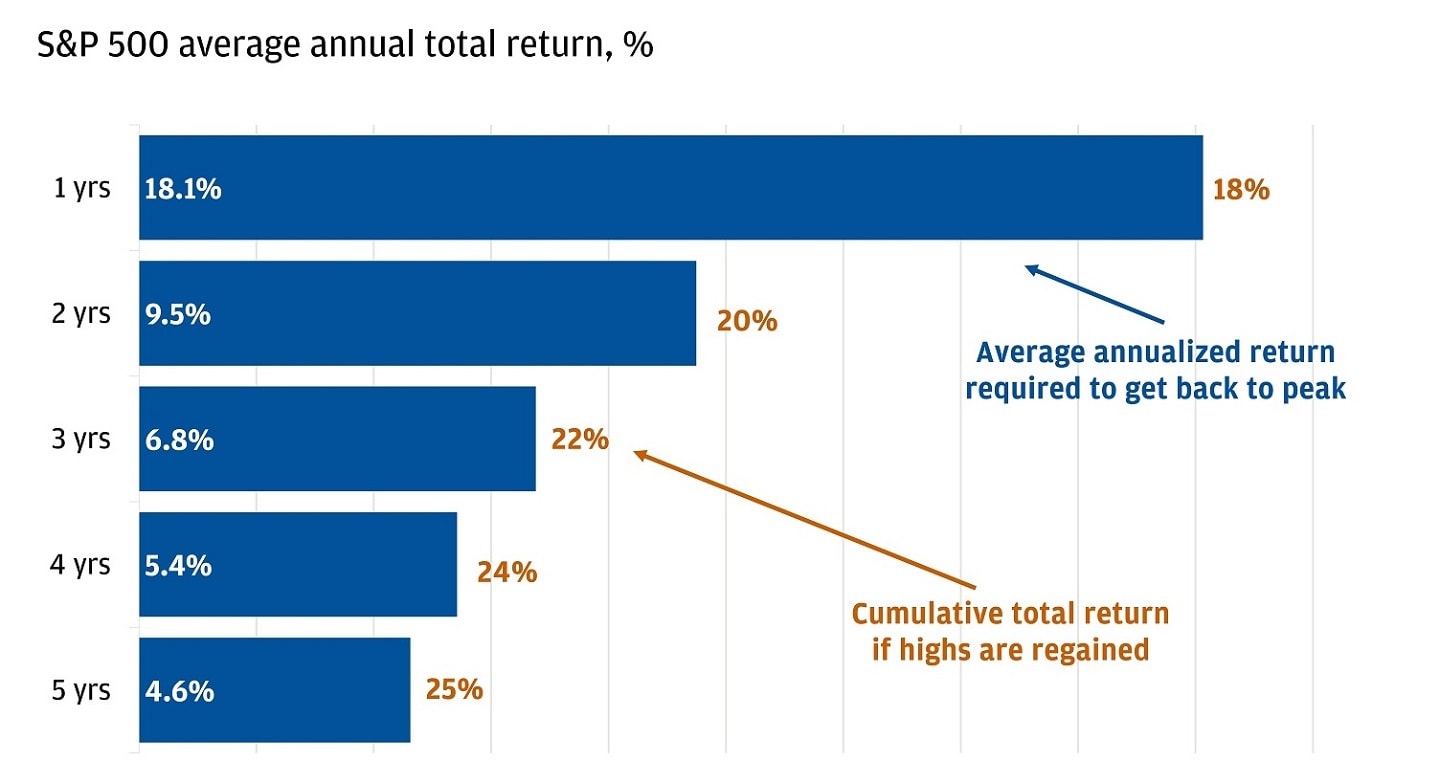

5. Market timing is futile and staying invested is paramount. Over the last 20 years, seven of the 10 best days in markets occurred within 15 days of the 10 worst days. Said differently, days with significant stock market losses cluster with days that see outsized gains. Last Friday, the S&P 500 lost -6%. On Wednesday, the S&P 500 gained +9.5%. Missing Wednesday’s gain is equivalent to missing nearly 1.5 years of equity returns based on our Long-Term Capital Market Assumptions (LTCMAs). Good luck timing this market. So how should investors think about the prospects of future returns? The S&P 500 has never failed to make new all-time highs after sell-offs and bear markets. If you think it will take three years to get back to the all-time high, you would expect to earn a +6.8% average annual return including a 1.5% dividend yield, just ahead of our long-term assumption of +6.7% per year.

Even if it takes 3 years to regain highs, returns are in line with our LTCMAs

Perhaps the most important thing investors can do during times of market volatility is to revisit their plan. A clear definition of investment success is a critical input for portfolio construction. Your J.P. Morgan advisor is here to help you navigate market volatility in the short-run while focusing on your success in the long-run.

All market and economic data as of 04/11/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

Explore ways to invest

Take control of your finances with $0 commission online trades, intuitive investing tools and a range of advisor services.

U.S. Head of Investment Strategy