Is it a golden era for gold?

Vice Chairman, J.P. Morgan Private Bank

By: Yuxuan Tang and Stephen Jury

Gold prices have more than doubled since late 2023, repeatedly hitting all-time highs in a sustained rally. The precious metal outperformed major equity benchmarks in 2025 with an eye-popping 65% return, its strongest single year since 1979, then built on those gains in early 2026.

A sought-after commodity for centuries, gold has been a popular component in investment portfolios in modern times, and has delivered attractive annual returns of approximately 12% over the 20 years ending in 2025. That said, its price can be volatile: Gold sank 9.8% on January 30, surrendering about half its prior 2026 gain in the biggest one-day loss since 2013. Weakness in gold prices can be prolonged, as gold tumbled approximately 40% from September 2011 to December 2015, and did not fully recover until August 2020.

This combination of a historic rally and historic volatility would seem to challenge the case for investing in gold today. However, we remain firmly bullish on gold in 2026 and recently raised our outlook to a range of $6,000 to $6,300 per ounce. The recent sell-off may present a potential entry point for long-term investors, and there may be potential for further upside as investors look to diversify dollar exposure, hedge geopolitical risk and guard against inflation surprises.

To explain why, we’ll dig into the complex interplay of macro factors and supply and demand dynamics that influence gold prices.

Understanding gold’s unique characteristics and benefits is crucial for investors who are looking to establish portfolios that endure through cycles. We will show how the key drivers of gold prices have evolved in recent years, and how an appropriately sized allocation to gold can add value to a portfolio.

What drives gold prices?

The level of the US dollar

As gold is denominated in U.S. dollars, gold prices have often exhibited a negative correlation with the value of the dollar. When the dollar weakens, gold becomes more relatively attractive for holders of other currencies, increasing demand. Conversely, gold prices tend to weaken as the dollar strengthens. The decline in gold prices in January may have also been impacted by the Trump administration’s Federal Reserve chair announcement because Kevin Warsh is perceived as an inflation hawk.

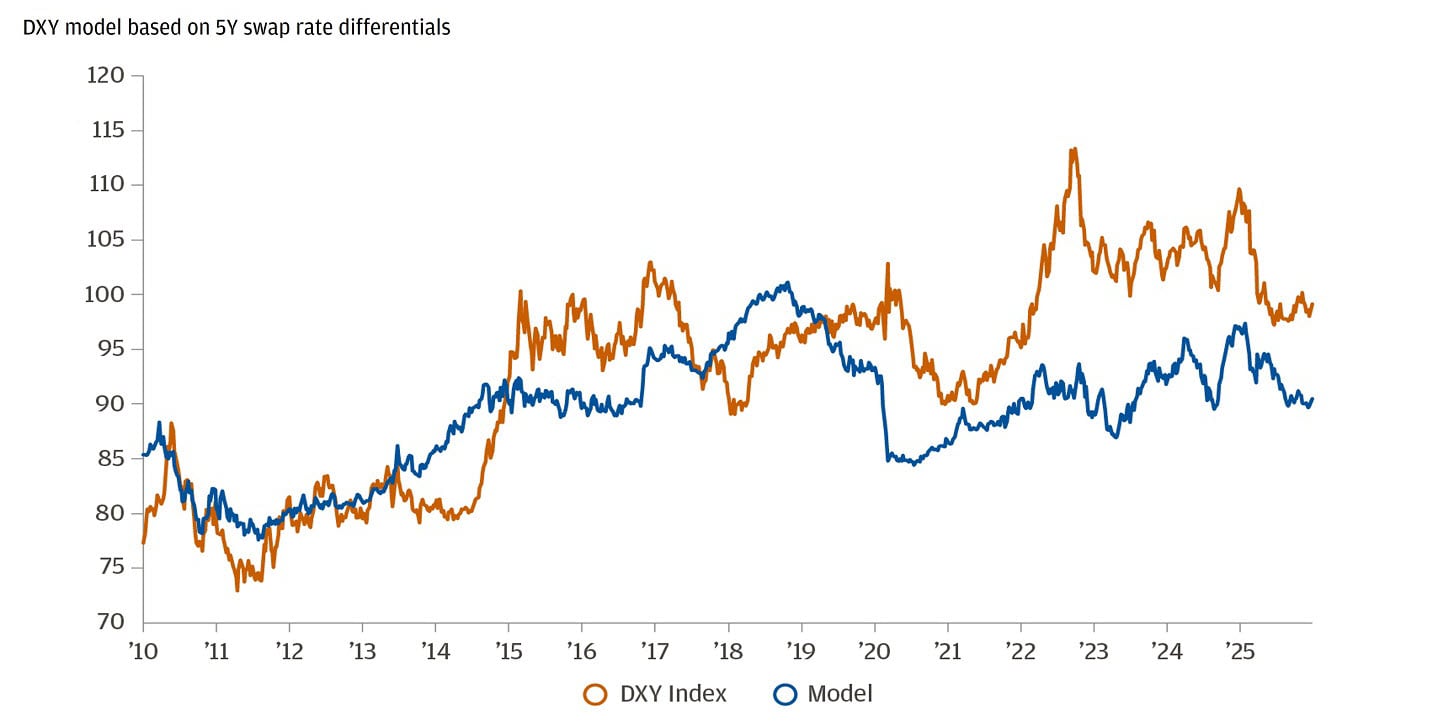

However, there are instances when this relationship does not hold. For example, in 2012-13, gold lost 18% of its value even though the dollar remained relatively stable, rising less than 1%. We think a relatively weak dollar will present a stable and benign backdrop for gold prices over the next six to 12 months. Following a year of significant weakness, the dollar is entering a bumpy process of bottoming, as shown in the chart below. In our base case, we anticipate that the U.S. economy could gradually recover over the second half of the year, potentially coinciding with improvements in other major economies such as Europe and Japan. Lingering concerns over Federal Reserve (Fed) independence and U.S. fiscal sustainability may also limit the dollar’s strength.

US Dollar to stabilize, tracked via interest rate differential

Change in real yields

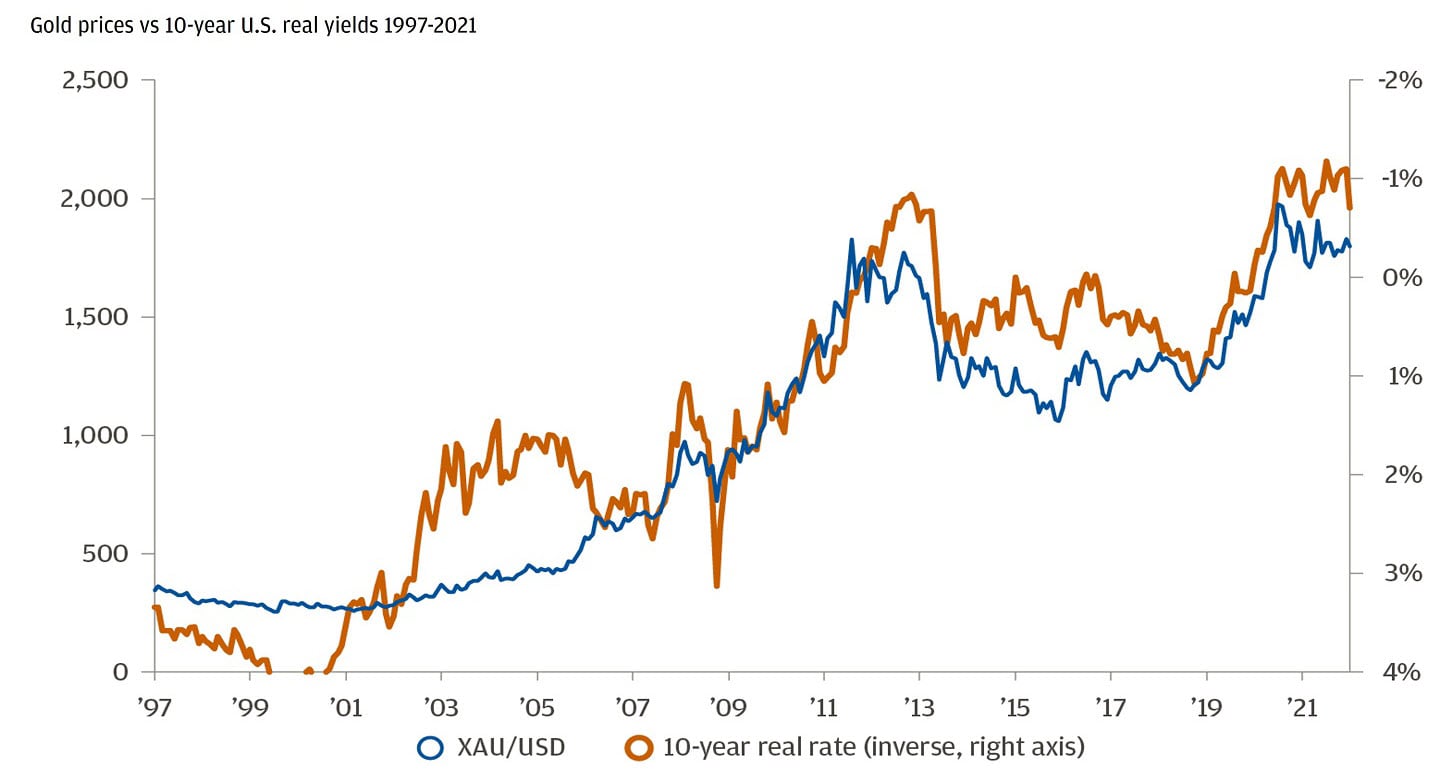

Historically, gold prices have generally had an inverse relationship with real yields (inflation-adjusted interest rates). As gold does not generate interest income, real yields can be seen as the opportunity cost of holding it. When real yields go down, gold becomes more attractive relative to interest-bearing assets such as cash and fixed-income securities.

This relationship explains a large part of the price increase in gold since the 1990s, a period of structural decline in real yields. Large gold rallies such as those in 2008-2012 and 2019-2021 can also be attributed to real yields turning negative due to global quantitative easing and zero interest rate policies. This chart tracks the relationship.

Traditional inverse correlation before 2022

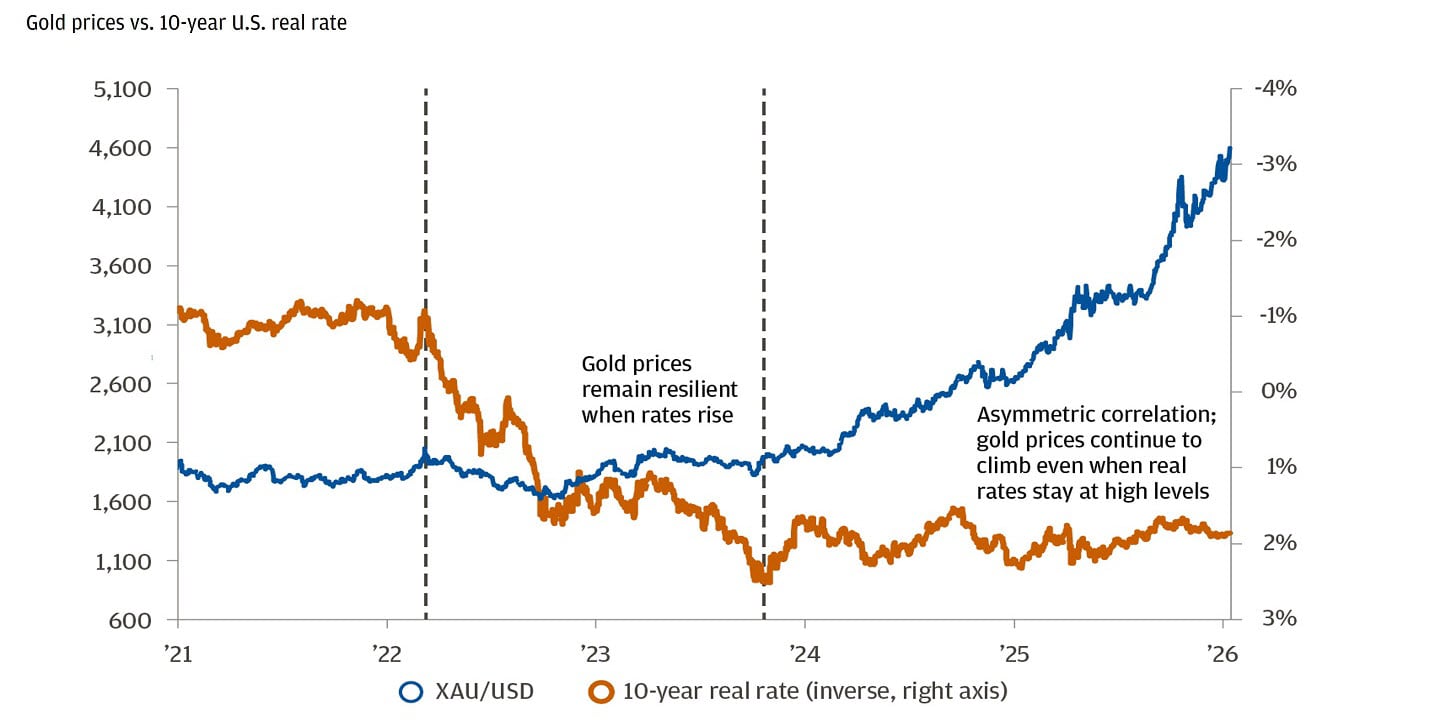

However, there are periods where this relationship breaks down, and as the chart below shows, that’s been the case over the past two years. In early 2022, the Fed began raising interest rates at an unprecedented pace in response to stubbornly elevated inflation and global supply disruptions following Russia’s invasion of Ukraine. Real yields rose from deeply negative territory to the highest levels seen since the global financial crisis of 2008. Yet gold remained very resilient: Prices were little changed in 2022, although with significant volatility, and in 2023 posted a +13% return, ending the year at a record high of $2,068 per ounce.

We believe this correlation is not broken and will likely reestablish itself. At present, gold still reacts to the movements in real yields, only in an asymmetric manner: It rises when yields decrease, but declines to a smaller degree when yields increase. Why? The primary reason is a recent shift in supply and demand dynamics.

Since 2022, gold prices stayed incredibly resilient despite much higher real yields

Supply and demand dynamics

All commodities prices are driven by supply and demand. Demand for gold is particularly important because supplies (in the form of gold mining) have been fairly stable for many years. This sets it apart from other commodities. There are three key sources of demand for gold: industrial, investment and reserve management.

Jewelry fabrication accounts for around 50% of total annual gold consumption. Demand is particularly strong in Asia, especially from India and China. Industrial and technology uses account for around 10% of gold demand, with significant sources including electronics, dentistry and aerospace.

While investment and reserve management demand accounts for a smaller portion of total gold demand, at times they are significant drivers of gold prices. This has been the case in recent years.

Central banks have been significant buyers of gold for centuries. Under the Gold Standard, central banks were required to hold sufficient gold reserves to back their currencies and allow currency to be exchanged for gold. When this system proved unworkable during times of crisis, governments adopted the Bretton Woods system, which fixed the dollar to gold at a set price and fixed international currencies to the dollar.

Strains began to emerge as the United States began to run large deficits, and the United States fully abandoned the link to gold in 1971, allowing the price of gold to float freely on international markets.

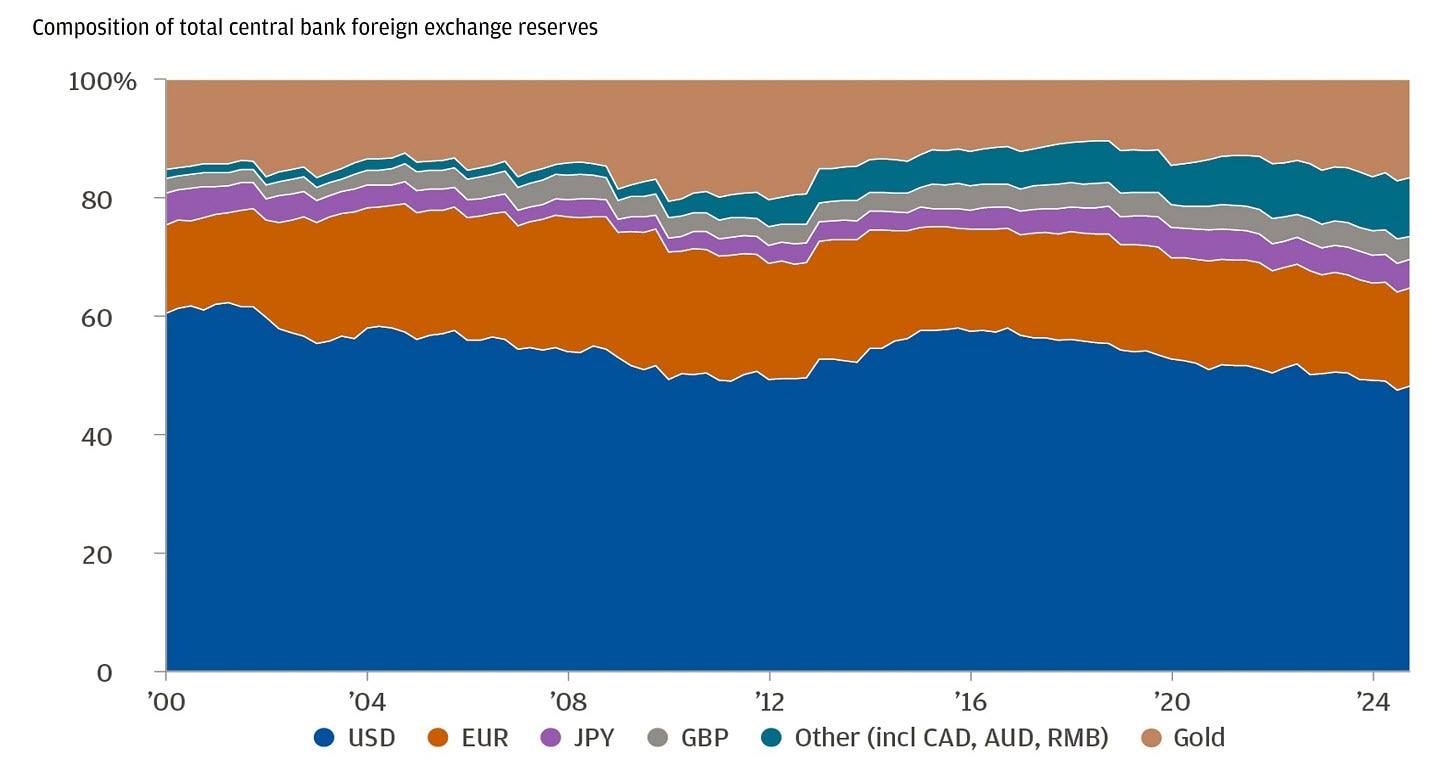

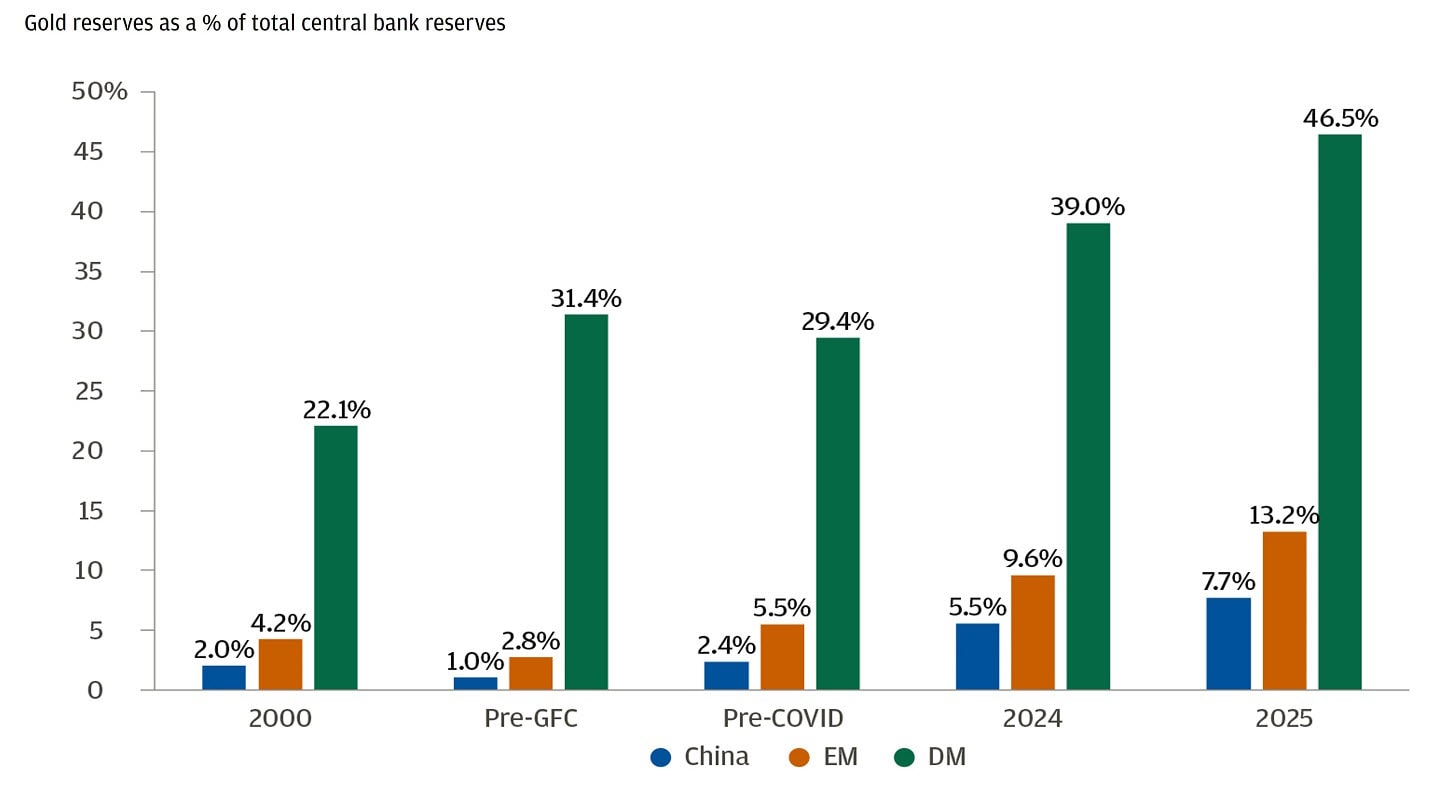

Still, central banks find gold to be an appealing store of value because it is scarce. Over the past 20 years, central banks worldwide have generally kept around 20% of their foreign exchange reserves in gold. However, emerging market central banks tend to hold much less gold than their developed market peers, as this chart shows.

Central banks hold ~20% of FX reserves in gold

EM central banks may catch up on gold allocations

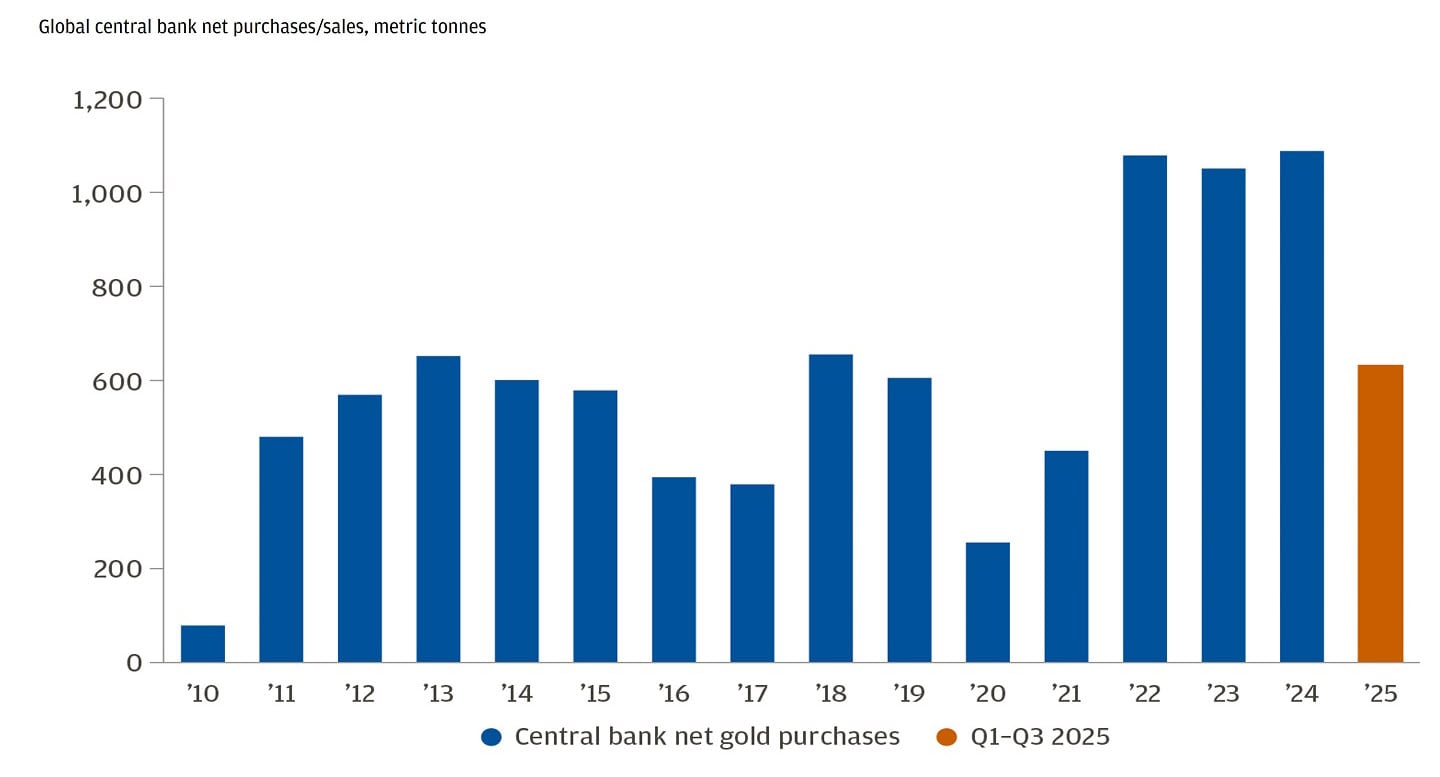

After a long hiatus, central bank purchases have risen notably in recent years. Net purchases by central banks reached a record 1,082 tons in 2022, more than doubling the average over the previous 10 years. They sustained that breakneck pace in 2023 and 2024, and purchases slowed only slightly over the first three quarters of 2025 despite the sharp price rally. Demand remained broad-based and driven by emerging market central banks.

The outlook of central bank purchase remains strong, as a record of 43% of 73 global monetary authorities believe their own gold reserves will increase over the next year. There are several reasons for this, but it has become apparent that countries facing elevated geopolitical risks (such as those on the borders of the Russia-Ukraine war) are increasing their gold reserves.

Some nations that are not allied with the United States are looking to reduce their reserve mix away from dollars to make those reserves less vulnerable to sanctions. Other governments aim to add some protection against a backdrop of higher and more volatile inflation worldwide. The scarcity of gold sometimes makes it useful as an inflation hedge, although this is often transitory.

Central bank demand has doubled since 2022

Retail and institutional investors

Many investors hold positions in gold through exchange-traded funds (ETFs), futures markets, options or structured notes. Some prefer to hold the physical metal and invest in bars, coins and claims linked to individually numbered bars. Institutional investors often hold physical gold and are more long-term oriented. Pension funds and foundations, in particular, tend to hold the metal for decades. Hedge funds and commodity trading advisers are more speculative in their approaches but can have prolonged impacts on price movements.

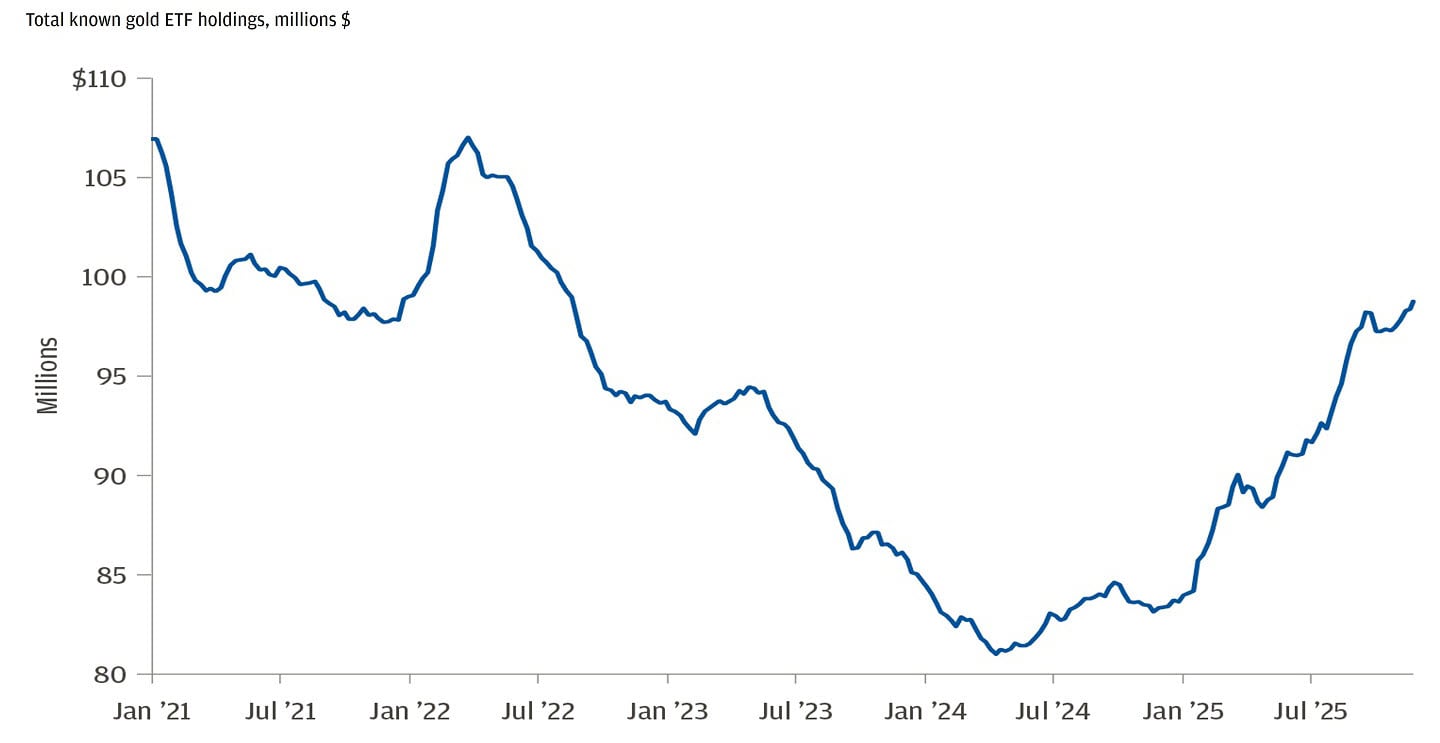

Holdings of gold ETFs have become popular with retail investors since their inception in 2004. Retail flows in gold ETFs are often short-term and tend to be driven by fears of inflation, conflict or crisis (they hit a record high during the COVID-19 pandemic), as well as interest rates. As the chart below illustrates, ETF demand picked up in mid-2025 and accelerated rapidly. It was a main driver for the sharp rally in 2025. This trend has exhibited a clear inverse correlation with movements in cash rates.

Retail investors typically shift into cash when the Fed maintains elevated rates. As the Fed reduces interest rates and cash yields decline, investors reallocate into fixed income or alternative strategies, including gold. This explains why holdings reached a trough in 2024: As the market began to price in imminent rate cuts by the Fed, cash returns declined, prompting a rotation into other asset classes.

Retail participation in gold ETFs has increased since mid-2024

Get up to $1,000

When you open a J.P. Morgan Self-Directed Investing account, you get a trading experience that puts you in control and up to $1,000 in cash bonus.

Gold in a portfolio

In our view, a key rationale for considering gold is its role as a portfolio diversifier. Historically, gold has exhibited a low correlation to both global equities and global bonds, and while this trend may persist, future correlations can vary depending on market conditions. Over the last five times the S&P 500 declined 20%, gold has averaged a 6% return. Gold has also tended to perform well during periods of higher inflation. Historically, when U.S. year-over-year Consumer Price Index (CPI) inflation has been between 3% and 4%, gold has averaged a one-year return of 13%.

As the steep decline seen in late January shows, gold is fundamentally a risky asset. Its annualized volatility over the past 20 years has been around 17%, slightly higher than that of large-cap equities. Since 1975, gold has experienced 91 distinct drawdowns of more than 10% – about one every seven months on average. The S&P 500 has seen 68 such drawdowns, or roughly one every nine months. This is not an asset class for the faint of heart.

Despite its high standalone volatility, gold generally lowers overall portfolio risk when funded from a mix of stocks and bonds due to its low correlation with both asset classes. According to J.P. Morgan Asset Management’s Long-Term Capital Market Assumptions (LTCMAs), adding a ~5% position to gold funded pro rata from a balanced allocation (55% stocks/45% bonds) keeps expected return unchanged, but modestly reduces expected volatility.

Our outlook on gold

As shown by our price outlook of $6,000 to $6,300 per ounce, we have a positive outlook on gold based on current market dynamics. Demand dynamics are robust: Broad-based central bank purchases are expected to persist as emerging market central banks continue to increase allocations. These institutions remain under-allocated to gold relative to their developed market peers. Further inflows from retail investors could occur if cash rates decline.

We expect to see sustained support for gold over the longer term due to concerns regarding fiscal discipline globally. In last year’s update, we expected gold to perform well under a Trump administration, based on certain economic factors: persistent concerns over the U.S. deficit amid expansionary fiscal policy, and a potential increase in dollar reserve diversification in response to trade tensions and heightened geopolitical risks. These factors may continue to influence gold prices in the coming year.

Invest your way

Not working with us yet? Find a J.P. Morgan Advisor or explore ways to invest online.

Vice Chairman, J.P. Morgan Private Bank