How to prepare to enroll in Medicare

Wealth Planner, Wealth Planning and Advice at J.P. Morgan Wealth Management

- Enrolling in Medicare early – ideally three months before the month you’ll turn 65 – ensures your coverage starts on time and may help prevent gaps.

- Fully understanding Medicare eligibility and coordinating with your current employer’s plan if you have coverage this way is crucial for a smooth transition.

- Once enrolled in Medicare, you’re prohibited from contributing to a health savings account (HSA). To avoid tax penalties, individuals should stop making HSA contributions six months before enrolling in Medicare.

Enrolling in Medicare – the federal health insurance program in the U.S. for people age 65 and over – is a significant milestone for many individuals as they approach retirement age. It marks the transition to a health care system that provides essential coverage for medical expenses, ensuring peace of mind in the golden years.

This article will guide you through the steps to prepare for Medicare enrollment, highlighting key considerations such as timing, eligibility and what to consider if you’re nearing Medicare age and still working.

How to prepare to enroll in Medicare

There are several steps you can take to prepare for the transition to Medicare before you actually enroll. For more information, check out J.P. Morgan’s Wealth Planning & Advice team’s white paper on Navigating Health Care Before and During Retirement. Here are some of the considerations to make.

Understand your Medicare eligibility

Most people qualify for Medicare at age 65. Exceptions include those with certain disabilities, end-stage renal disease (ESRD) or amyotrophic lateral sclerosis (ALS), who may qualify earlier.

Plan for enrollment timing

Enrolling during your birthday month or later means coverage will start the first day of the following month, which could leave you temporarily without coverage. Enrolling early – ideally in the three months before your birthday month – ensures your coverage starts on the first day of your birthday month and prevents any coverage gaps.

If your 65th birthday falls on the first day of the month, the Social Security Administration considers it to be in the previous month, shifting your enrollment period a month earlier.

It’s important to note that delaying enrollment without creditable coverage can result in lifetime penalties. Creditable coverage is employer-provided insurance that matches Medicare’s level of benefits.

Coordinate with your current coverage

If you’re still working and have employer-sponsored health coverage, you’ll need to understand how those benefits interact with Medicare. You may have a “special enrollment period” after your employer coverage ends.

Weigh if you need to plan for international retirement

Medicare generally does not cover medical services outside the U.S. Explore local insurance options if you are retiring abroad or traveling internationally.

Keep the open enrollment period in mind

From October 15 to December 7 each year, you can review and adjust your Medicare coverage to better suit your needs.

Thinking about retirement?

No matter what life stage you’re at, it's always the right time to plan for retirement.

How to sign up for Medicare

Once you’ve evaluated your options, thought about your coverage needs and are ready to enroll in Medicare, you may want to take the following steps to sign up.

1. Prepare for automatic enrollment (if applicable):

If you’re already receiving Social Security or railroad retirement benefits, you’ll be automatically enrolled in Medicare Parts A and B. You’ll receive an enrollment kit several months before you become eligible.

2. Enroll manually (if applicable):

If you’re not already receiving Social Security benefits, you’ll need to manually sign up for Medicare. You can enroll online, which is the fastest option, or in person at your local Social Security office. Have your Social Security number, current health insurance information and a form of personal identification ready. You may also need your employment details if you’re still working.

3. Take note of any special enrollment periods:

If you’re still working at 65 and have employer-sponsored health coverage, you’ll likely have an eight-month special enrollment period after your employer coverage ends to sign up for Medicare Parts A and B without penalties.

4. Choose your Medicare coverage:

Decide which parts of Medicare you’ll need: Part A (hospital insurance), Part B (medical insurance) and/or Part D (prescription drug coverage). Note that Medicare Part C, or Medicare Advantage, is an alternative to Original Medicare offered through private insurers. If you have other health coverage, such as through an employer, consider how that plan will interact with Medicare.

Enroll in Medicare Parts B and D for prescription drug coverage during your Initial enrollment period to avoid penalties.

5. Review and confirm your Medicare enrollment:

After you enroll, you should review your Medicare information to ensure all details are correct. You’ll receive a Medicare card in the mail confirming your enrollment.

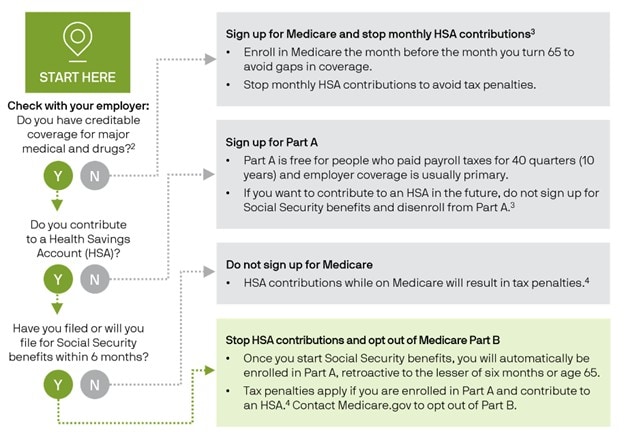

65 and still working: Should you sign up for Medicare?

If you’re approaching age 65 and still working, deciding whether to sign up for Medicare can seem like an overwhelming choice – and it will be influenced by your current employment benefits and your assessment of your future health care needs.

The following illustration provides a step-by-step “map” to help you navigate this decision. Please note, this information is not offered as personal tax or legal advice. Individuals should make benefits decisions in consultation with a qualified tax or legal professional.

Key issues to consider as you prepare to enroll in Medicare

In addition to deciding the right Medicare enrollment route to take, it may be helpful to consider the following:

Try to avoid coverage gaps

Don’t wait until the month you turn 65 to enroll in Medicare. Instead, plan to enroll during the initial window, which starts three months prior to the month of your 65th birthday, to avoid a 10% lifetime penalty.

Be aware of lifetime penalties

Failing to enroll in Medicare at 65 without creditable coverage can result in penalties. Creditable coverage is employer-provided insurance that matches Medicare’s level of benefits. If you or your spouse are still working, coordinate with the employer plan to alert Medicare; the latter may be able to provide secondary insurance coverage for expenses that the employer plan doesn’t cover.

Once enrolled in Medicare, you can’t contribute to an HSA

Once enrolled in Medicare, you can’t contribute to an HSA. Excess contributions incur a 6% penalty, so stop HSA contributions six months before signing up for Medicare to avoid violations.

The bottom line

Fully understanding your available health care options – and their implications – before you become eligible for Medicare is critical for ensuring your health-related needs are adequately covered in retirement.

A J.P. Morgan professional can help you integrate your health care considerations into a holistic wealth management plan in conjunction with guidance from your personal tax and legal professionals.

Invest your way

Not working with us yet? Find a J.P. Morgan Advisor or explore ways to invest online.

Wealth Planner, Wealth Planning and Advice at J.P. Morgan Wealth Management