The 2026 Social Security COLA increase has been announced: Here’s what it means for your benefits

J.P. Morgan Wealth Management

- The Social Security Administration announced that the 2026 cost-of-living adjustment (COLA) increase will be 2.8%, up slightly from 2025’s COLA of 2.5%.

- The COLA is intended to help Social Security benefits keep pace with inflation over time.

- Beyond the COLA, 2026 changes to Social Security include an update to the full retirement age, an increase in wages required to earn credits, and a higher taxable wage base and earnings limit.

For millions of Americans, Social Security plays a critical role in retirement planning by providing a monthly income that can help cover living expenses. And every year, the Social Security Administration (SSA) reviews and considers updates to the program based on inflation and wage growth. One of those potential changes is the cost-of-living adjustment (COLA), which is designed to help maintain beneficiaries’ purchasing power over time.

The federal government shutdown delayed the announcement of the 2026 Social Security COLA, which relies on data from the U.S. Bureau of Labor Statistics. Originally scheduled for October 15, 2025, the announcement was postponed to October 24. Despite the delay, the SSA has now confirmed that everyone receiving Social Security or Supplemental Security Income (SSI) benefits will see a 2.8% increase in their monthly payments starting in January 2026. This means the average retired worker will see their monthly check increase from $1,976 to $2,032 – a boost of about $56.

“Social Security is a promise kept, and the annual cost-of-living adjustment is one way we are working to make sure benefits reflect today’s economic realities and continue to provide a foundation of security,” SSA Commissioner Frank J. Bisignano said in a statement.

“The jury is still out regarding how the 2.8% COLA increase will help with some inflation and higher health care costs,” Greg Farber, Executive Director and Wealth Planner at J.P. Morgan Wealth Management said. “I feel it is an important time to check in with one’s financial advisor and review your personal plan.”

This article will walk through the 2026 Social Security COLA, including what it is and how it’s calculated, as well as some other Social Security updates for 2026. If you’re a Social Security recipient, understanding these changes can help you better financially plan for the coming year and beyond.

How the Social Security COLA is calculated

Each year, the SSA calculates the next year’s COLA – a figure designed to help benefits keep pace with inflation – using the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). Specifically, the agency compares the average CPI-W from the third quarter of the current year with the same three-month period in the previous year to determine whether consumer prices have gone up. If they have, then the SSA adjusts Social Security benefits accordingly for the coming year.

In 2025, the average third-quarter CPI-W rose by 2.8% over the previous year. The corresponding Social Security COLA for 2026 will help offset the effects of inflation on food, housing, transportation and health care costs, among other common beneficiary expenses.

Thinking about retirement?

No matter what life stage you’re at, it's always the right time to plan for retirement.

How the 2026 Social Security COLA adjustment compares to past years

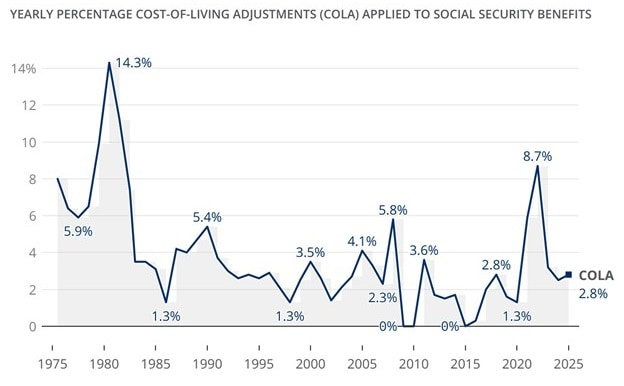

The 2.8% increase in 2026 is slightly higher than 2025’s 2.5% increase, reflecting moderate but steady inflation over the past year. Over the past decade, the COLA increase has averaged about 3.1%.

Historically, COLA adjustments have varied widely depending on economic conditions. For instance, there was no COLA in 2010, 2011 or 2016, when inflation remained low.

In comparison, 2021 and 2022 marked the largest benefit increases in four decades, when inflation drove COLAs to 5.9% and 8.7%, respectively. The 2026 adjustment indicates that inflation is returning to more typical patterns, staying closer to the Federal Reserve’s long-term goal of 2%.

Social Security COLA increases: 1975–2025

What other changes are coming to Social Security in 2026?

In addition to the COLA, the SSA announced several updates for 2026 that affect both beneficiaries and workers actively contributing to the Social Security program. Here’s an overview of the other Social Security changes you can expect to see in 2026:

- Full retirement age (FRA): In 2026, after years of gradual changes to the program, the FRA reaches 67 for those born in 1960 or later.

- Taxable wage base: The taxable wage base determines how much of your annual income is subject to Social Security taxes. For 2026, that number will rise to $184,500, up from $176,100 in 2025.

- Earnings limit: You can still work while collecting Social Security benefits, but they may be reduced if you earn more than a certain income. The earnings limit for those below the FRA will rise to $24,480 in 2026; for every $2 earned above that amount, the SSA will withhold $1 in benefits. If you will reach the FRA in 2026, the limit increases to $65,160; for every $3 earned above that limit, the SSA will withhold $1 – but only through the month before you reach the FRA.

- Social Security credits: In 2026, the income needed to earn one credit will be $1,890, up from $1,810 for one credit in 2025.

Will Social Security be taxed in 2026?

Social Security benefits will continue to be taxed at the federal level as they have for decades, although a new deduction could affect individuals’ taxable income.

If you file as a single individual and earn between $25,000 and $34,000, you may have to pay federal income taxes on up to 50% of your Social Security benefits. If your income exceeds $34,000, up to 85% may be subject to federal tax. For married couples filing jointly, the thresholds are $32,000 to $44,000 for partial taxation and more than $44,000 for the maximum 85%. These thresholds have not changed since 1993.

At the state level, the tax treatment of your benefits varies depending on your location. While most states don’t tax Social Security benefits at all, the following states tax a portion of them: Colorado, Connecticut, Minnesota, Montana, New Mexico, Rhode Island, Utah, Vermont and West Virginia. Of note, West Virginia is phasing out its state income tax on Social Security benefits and will fully eliminate it starting in 2026.

In 2026, one change that could affect how much you pay in taxes on your Social Security benefits is the One Big Beautiful Bill Act’s new deduction for seniors. Signed into law on July 4, 2025, this legislation provides a $6,000 deduction for qualifying seniors age 65 and older, or $12,000 for an eligible married couple. If you’re eligible, you can claim this deduction in addition to the standard deduction.

The senior deduction doesn’t change how Social Security benefits are taxed – or the exclusionary income thresholds mentioned above – but it can help lower your overall taxable income, thereby making it possible for you to reduce your Social Security taxes.

How to get help with your Social Security benefits

If you have questions about your Social Security benefits, it’s best to reach out to the SSA directly. You can manage your benefits online at SSA.gov using the agency’s free “my Social Security” online service.

Log in to request a new Social Security card or manage your benefits. And if you don’t have internet access, you can call the SSA at 1-800-772-1213 or schedule an appointment at one of the agency’s local offices.

The bottom line

Every year, the SSA evaluates the COLA and earnings limits to determine whether changes to Social Security benefits are needed based on inflation and rising wages. Staying informed about these annual updates can help you understand how they might influence your income and overall financial outlook.

Signing up for the free “my Social Security” online service is the best way to check your benefits information and review payment schedules. You’ll also be notified about COLA updates in your account. Remember, even minor changes can make a big difference in how much of your income you keep.

Frequently asked questions about changes to Social Security for 2026

In many ways, Social Security is similar to an insurance program: Workers contribute to it throughout their careers so they’ll have financial protection later in life. Contributions are automatically deducted from workers’ paychecks under the Federal Insurance Contributions Act (FICA), and the money is pooled into two large trust funds managed by the U.S. Treasury – the Old-Age and Survivors Insurance Trust Fund and the Disability Insurance Trust Fund.

The Social Security benefits you’re eligible for depend on your work history and age. Every worker earns credits based on their income: In 2025, you earn one credit for every $1,810 you earn, up to a maximum of four credits per year. Each year, the earnings required for credits increase slightly as average wages increase. Earned credits stay on your record regardless of whether you switch jobs or leave the workforce for a period of time.

Most people need at least 40 credits to qualify for retirement benefits, which you can claim as early as age 62. In fact, the amount of money you receive from Social Security every month is based on both the age you start claiming benefits and your lifetime earnings, adjusted for inflation.

The 2026 COLA takes effect in January 2026, and payments are typically distributed based on your date of birth. You can check the Social Security payment schedule for 2026 to see when you’ll receive your benefits.

The SSA automatically applies the COLA to your benefit amount. You can view your updated benefit by logging into the “my Social Security” online service. The SSA typically sends COLA notices by mail and electronically in December outlining your new monthly benefit and net payment amount.

The COLA is tied to inflation, so an increase directly affects the dollar amount of current recipients’ benefits. And even if you haven’t yet claimed Social Security, yearly COLAs indirectly help maintain the purchasing power of your future benefits.

Invest your way

Not working with us yet? Find a J.P. Morgan Advisor or explore ways to invest online.

J.P. Morgan Wealth Management