Answering some FAQs about the economy right now: Tariffs, the government shutdown and European markets

Global Investment Strategist

I recently had the great opportunity to meet with clients, prospects and advisors in Atlanta and Houston. What I enjoy most about going out on the road is learning from the people that I meet based on the questions they ask about our outlook. Many questions from my recent trip revolved around our views on artificial intelligence (AI), which our team covered in a separate article and can be found here. With that, I thought it would be helpful to answer three other frequently asked questions below.

Have we actually seen tariff-driven inflation in the U.S.?

The short answer is, yes, we have seen tariff-driven inflation. Our estimate is that tariffs have contributed around 0.5 percentage points to inflation this year, and we expect that impact to increase into the beginning of next year. Tariffs are the primary reason why we see year-over-year core Personal Consumption Expenditures (PCE) inflation reaching close to 3% this year, rather than the 2% outlook that we had at the start of the year.

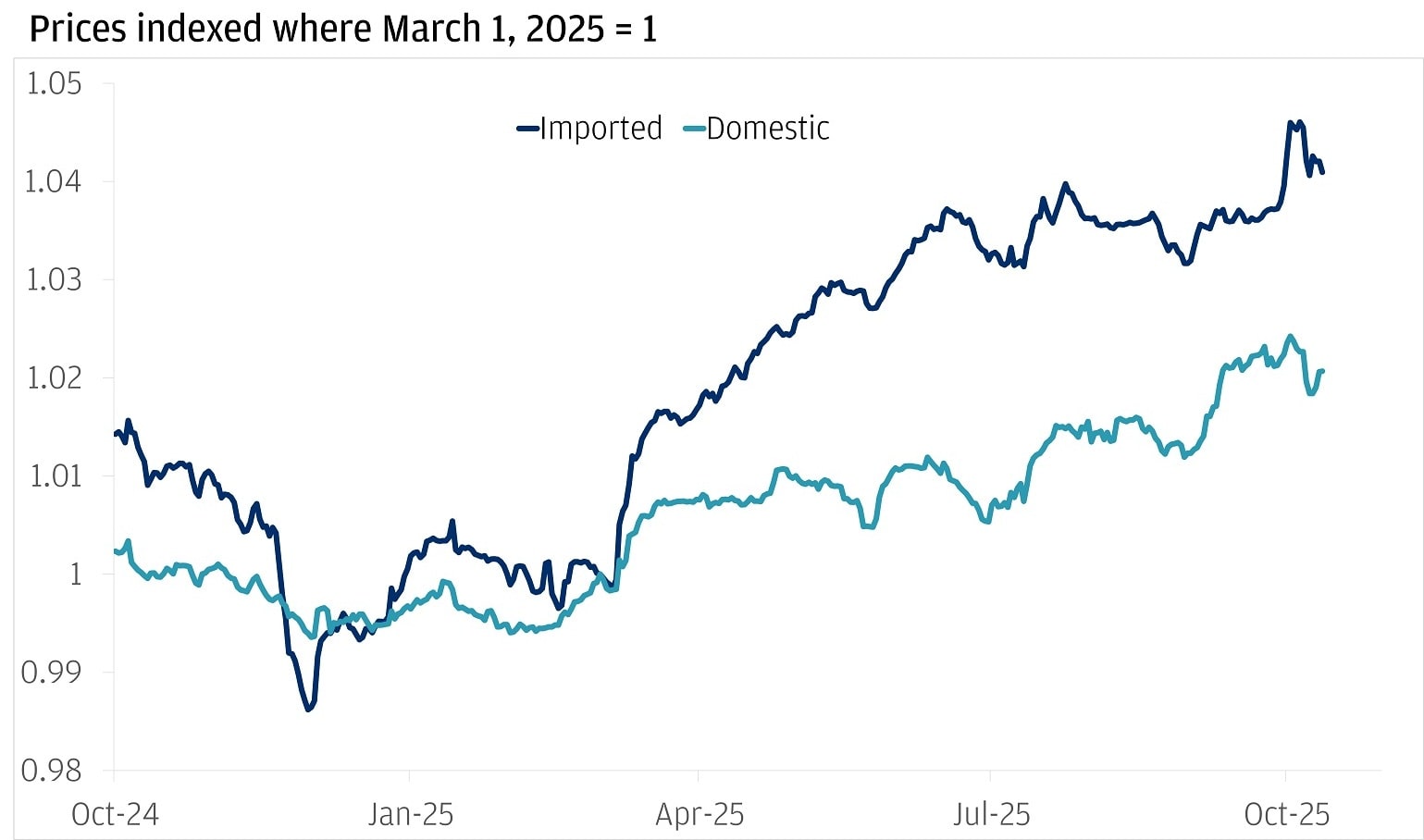

While the official statistics have shown an increase in goods prices driven by tariffs, alternative measures of price data help bring this to light. The below chart is from the Pricing Lab at the Digital Data Design Institute at Harvard University. They collect daily prices on goods sold from four major retailers in the U.S. and only include goods where they can directly classify the data as imported or domestic. The chart shows that, since March 1, 2025, imported goods prices have increased by 4%, and domestic goods prices have increased by 2%. Relative to the deflationary trend from last year in both imported and domestic goods, it’s clear that tariffs are pushing prices higher, with imported goods seeing a more direct impact.

Importantly, we see tariffs as a one-off increase in prices and not a persistent source of inflation. To get that persistent inflation pressure like we saw during 2021 and 2022, we think you’d need to see an increase in services inflation, primarily driven by strong wage growth. With the labor market still weak, we see this as a lower probability, which could give the Federal Reserve (Fed) confidence to continue lowering interest rates and focusing on the full employment side of its mandate.

Tariffs have pushed imported and domestic goods prices higher since March

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

Does the length of the government shutdown matter?

Yes and no. It matters because we temporarily lose availability of certain official government statistics regarding the state of the economy. The labor market is in a precarious situation, and while we can proxy its health through private data sources such as the ADP employment report or regional Federal Reserve estimates, the official data remains the best source. Without it, more guesswork is required to understand how the labor market is evolving.

The shutdown matters for how we think about near-term economic growth. For each week of the shutdown, it’s estimated that annualized quarterly gross domestic product (GDP) growth would be lower by 0.1–0.2 percentage points. With the shutdown extending close to a month (and going), it would shave off around 0.4–0.8 percentage points from growth this quarter. Essentially, if we thought growth would be 2% annualized this quarter, it would be 1.2%–1.6%, all else equal. It will likely make Q4 2025 growth look weaker, but if the shutdown ends later this quarter, the first few quarters of 2026 will probably look stronger as furloughed workers receive backpay of wages withheld during the shutdown.

The next milestone to keep in mind is November 1, the date on which funds for the Supplemental Nutrition Assistance Program (SNAP) are expected to run out. The lack of November SNAP benefits could impact over 40 million Americans and could further weigh on economic growth this quarter.

The shutdown also matters for how we interpret the quality of the October inflation data that would be released in November. This is because most of the Consumer Price Index (CPI) data is collected in the field, and with employees from the Bureau of Labor Statistics (BLS) remaining furloughed, those prices cannot be collected. How the BLS handles data collection in the weeks ahead remains an open question, and it’s possible that the October data may not be released at all.

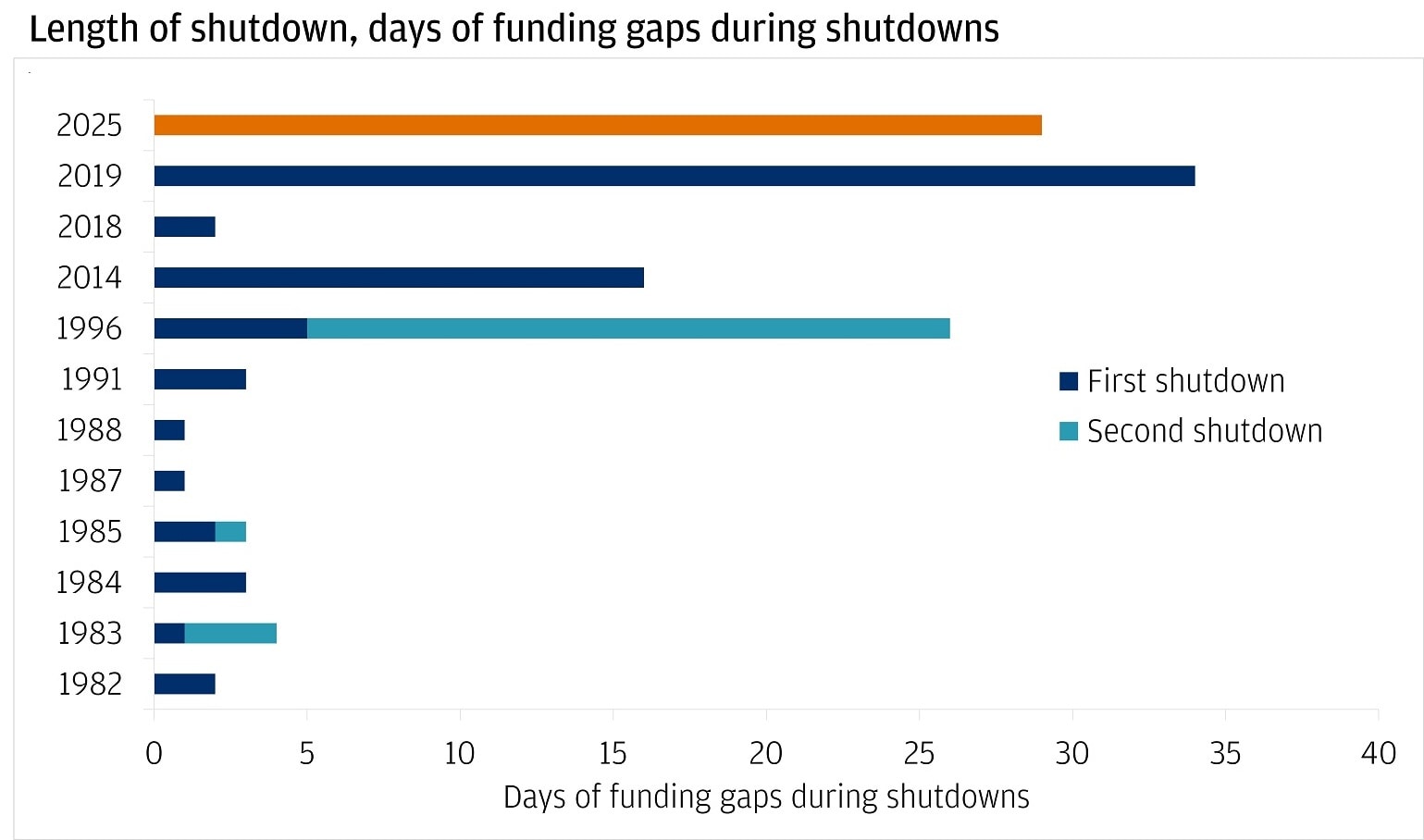

All of this said, for U.S. asset markets, despite the length of the shutdown (now the second longest in history), it’s had a minimal direct impact on equity or bond markets. That’s because U.S. asset markets are more focused on key narrative drivers like additional Fed rate cuts and the continued buildout of the AI ecosystem. The risk going forward is that asset markets interpret the shutdown as a more ominous signal of political dysfunction and begin to question the state of the U.S. economy absent official economic statistics, but for now, investors are content to focus on prevailing narratives without interruptions from constant government data releases.

U.S. shutdown is currently second longest in history

What could make Europe an attractive investment opportunity?

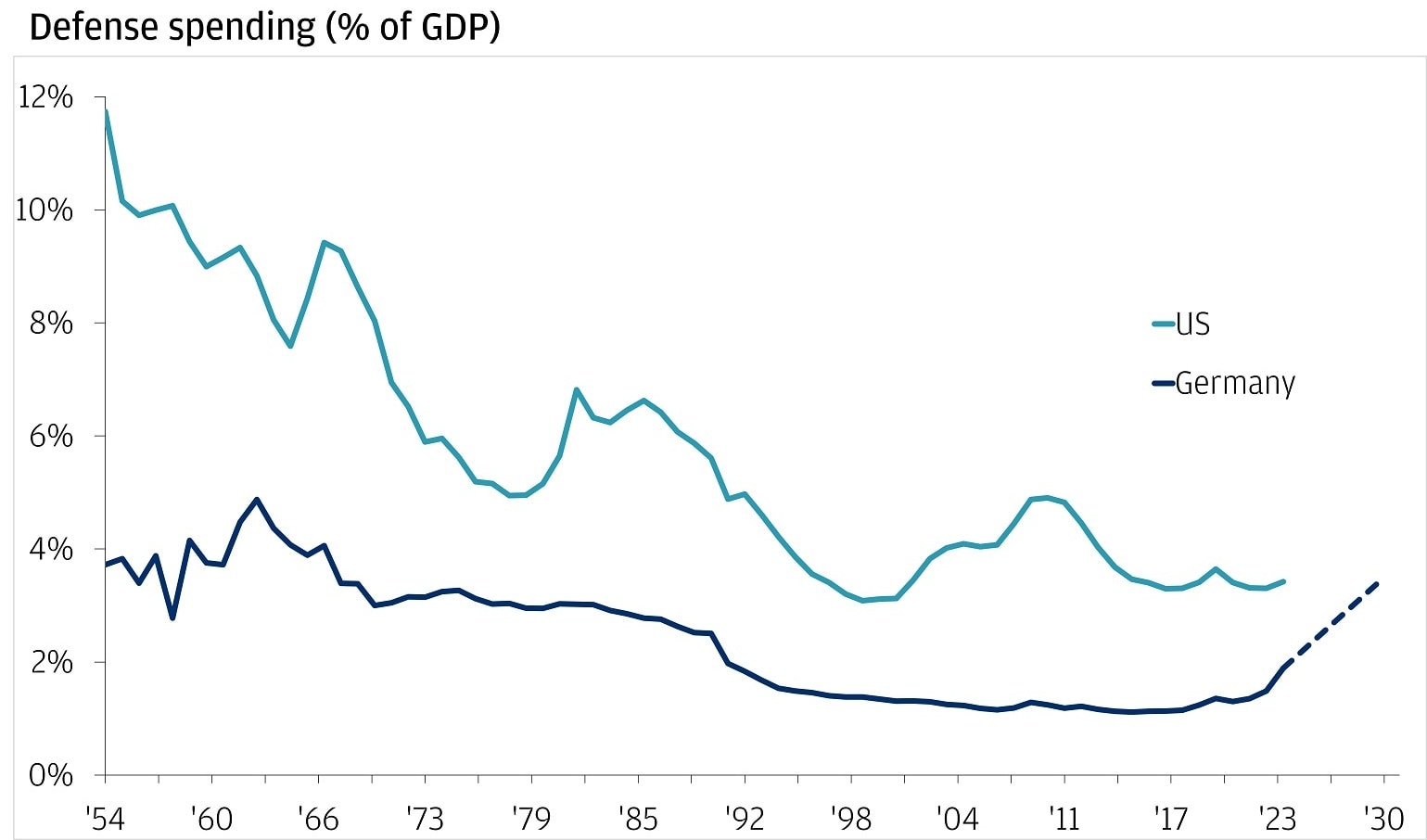

We completely understand the skepticism around investing in Europe. It’s been a market that has continually overpromised and underdelivered. With European equities (Stoxx 50) returning 34% (total returns) in U.S. dollar terms through October 24, 2025, it’s a fair question to ask whether the investment thesis has already played out. We don’t think so, because of some important changes that Europe has made over the past year when it comes to expansionary fiscal policy, and Germany stands out as a helpful example. Earlier this year, the German government passed a bill to invest roughly 650 billion euros ($756 billion) over the next five years on defense, with a similar amount being set aside for infrastructure investments.

It’s interesting because additional spending on defense and infrastructure could unlock faster productivity growth, which is something that Europe has been lacking for the past few decades. We also see that government research and development tends to lay the foundation for private sector investment to come through in the following years. Already there’s a “Made for Germany” campaign where around 60 private sector companies have committed to investing 600 billion euros over the next three years in the same type of sectors. And historically, we’ve seen a lot of innovation that comes out of these public/private partnerships surrounding defense – think nuclear, semiconductors, global positioning systems (GPS), the internet – so this could be a significant tailwind that potentially boosts trend growth in Europe and might extend the investment thesis.

German defense spending could match U.S. as a percent of GDP in coming years

All market and economic data as of 10/28/2025 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Global Investment Strategist