Why the S&P 500 had its best month in over 5 years despite Middle East uncertainty

Global Investment Strategist

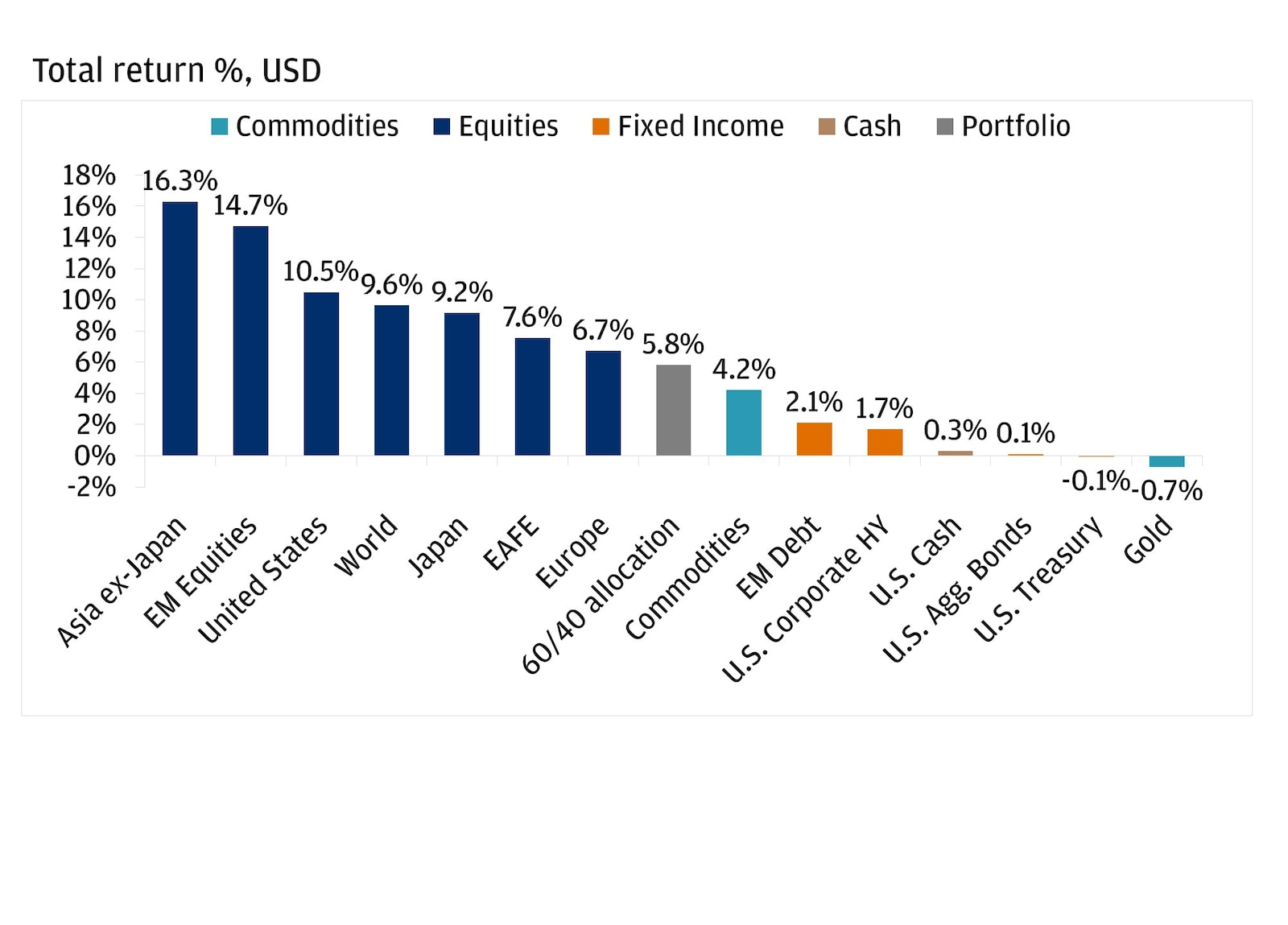

Global equities staged a broad-based recovery in April, with Asia ex-Japan up 16.3%, emerging markets rising 14.7% and U.S. stocks gaining 10.5%. This rebound followed a fragile ceasefire agreement between the U.S. and Iran early in the month, which helped ease fears of a sustained disruption to global energy supplies. Investors spent much of April balancing shifting geopolitical tensions, central bank expectations and resilient corporate earnings.

Below, we highlight how these developments helped most major asset classes and regions deliver positive total returns in April and what they could mean for portfolios heading into May.

Global equities stage massive rebound in April

Past performance is no guarantee of future results. It is not possible to invest directly in an index.

Middle East conflict: Fading escalation fears, despite risks remaining

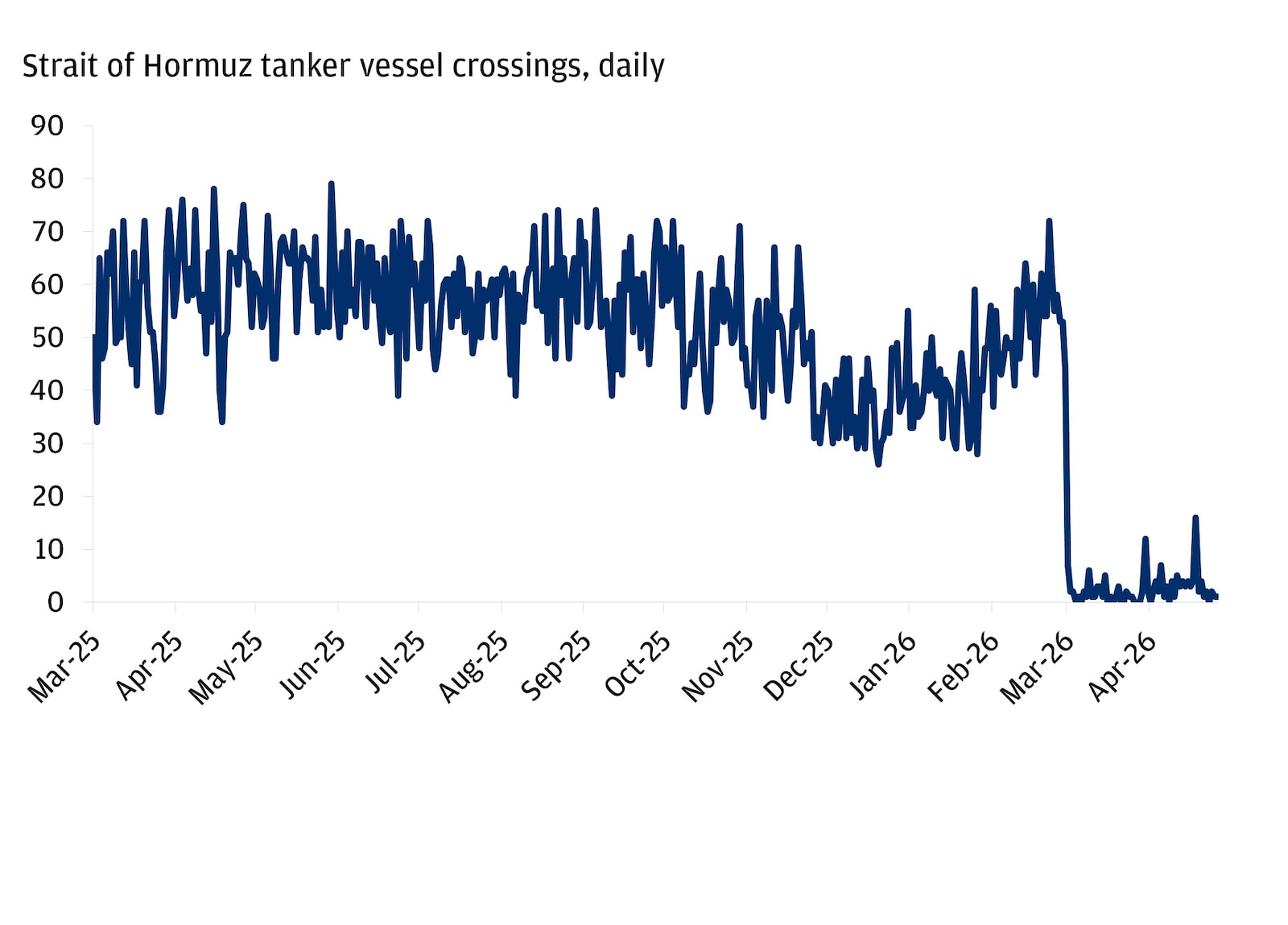

April began with markets still heavily focused on the U.S.-Iran conflict, which had resulted in the closure of the Strait of Hormuz, a vital shipping route for about 20% of the world’s oil supply, and rattled most major asset classes in March. Both sides agreeing to a ceasefire in early April provided a much-needed boost to sentiment and helped spark a global risk asset recovery (MSCI World +9.6% for the month).

Even still, oil prices remained elevated throughout April, with the strait remaining effectively closed as geopolitical risks have persisted and both sides have repeatedly tested the ceasefire.

The longer the Strait of Hormuz remains closed and oil supply constrained, the more severe the economic impact could become as higher energy costs filter through to businesses and consumers. A key concern is that these price increases may become long-lasting in the event of a drawn-out supply shock that compresses profit margins and impacts consumer spending, as households are forced to allocate more of their income to essentials like gasoline.

Despite ceasefire agreement, Strait of Hormuz remained effectively closed

While geopolitical risk has not disappeared, markets were able to look past the most severe tail risks in April. Looking forward, our base case anticipates a bumpy de-escalation with Iran and, over time, a normalization of energy prices rather than a prolonged shock.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

A divided Federal Reserve holds interest rates steady

Even if the conflict were to end fully today and the Strait of Hormuz were to reopen immediately, the elevated oil prices investors have seen over the past several weeks will likely continue to be felt throughout the global economy for some time. In April, monetary policymakers and investors got their first look at how the elevated oil prices were feeding through to economic data, with both core and headline March Consumer Price Index readings accelerating year-over-year.

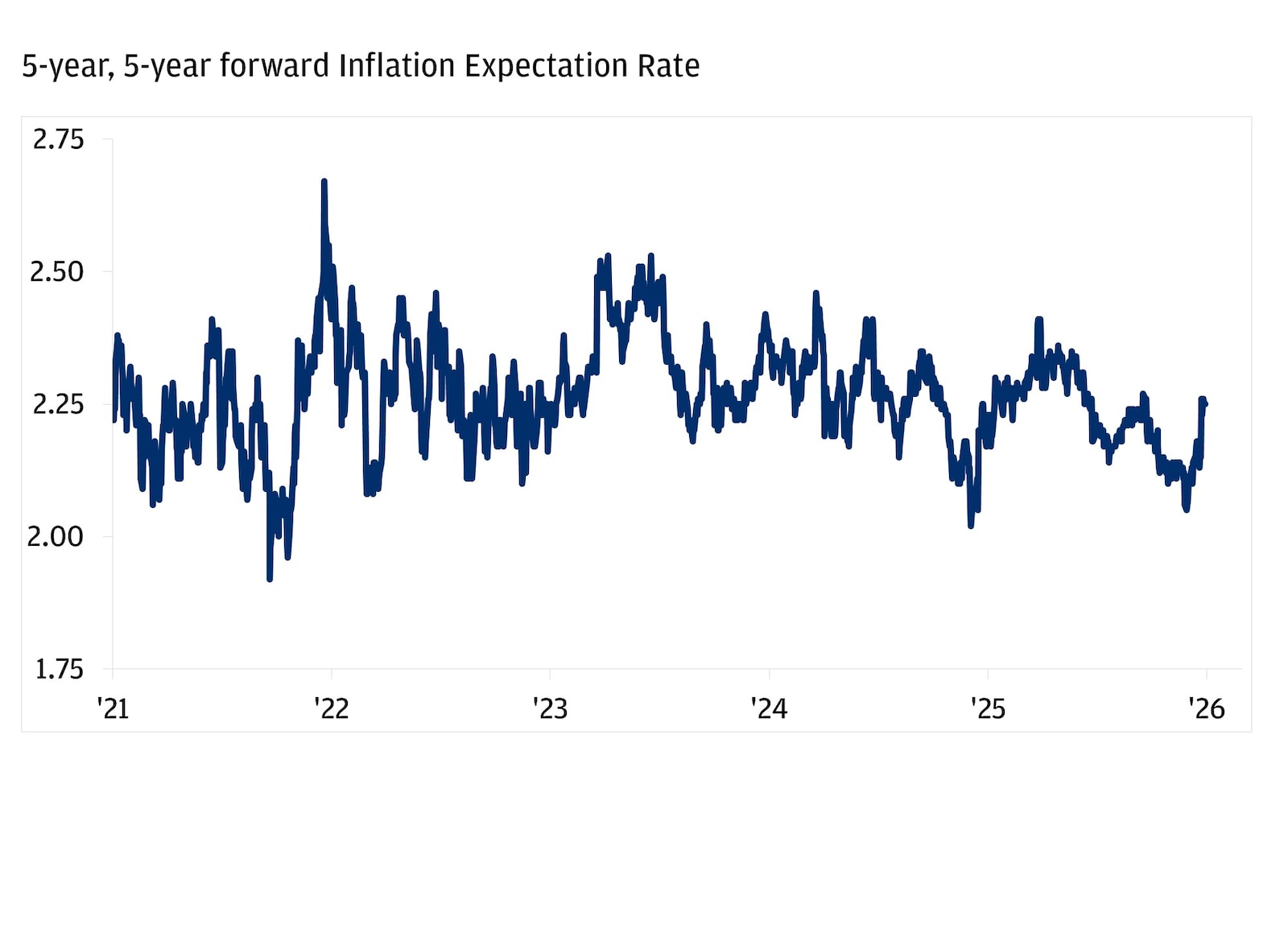

While it’s expected that inflation would pick up in the face of an oil price shock, a key metric to watch is long-term inflation expectations, as they can play a critical role in shaping the Federal Reserve’s (Fed) policy decisions.

If long-term inflation expectations sharply increase, it can influence consumer and business behavior. However, if expectations remain anchored like we’ve seen so far, temporary price shocks are less likely to become embedded in the broader economy.

Long-term inflation expectations remain anchored

The backdrop of elevated inflation combined with a labor market that has showed signs of potential stabilization as layoffs remain contained and job gains remain low, on average, helped position the Fed to maintain a “wait and see” approach.

At its April meeting, the Federal Open Market Committee left the federal funds rate unchanged, but the decision wasn’t unanimous. The meeting saw the most dissents in over 30 years, with Governor Stephen Miran voting for a 25-basis-point cut and three other voting members dissenting over language used in the Fed statement that could imply the Fed maintains its easing bias. The dissents away from maintaining the easing bias helped spark a nearly 5-basis-point rally for both two- and 10-year Treasury yields.

Yields moving higher could provide a renewed opportunity for investors to be compensated for stepping out of cash, which can help protect purchasing power in an elevated inflation environment. We expect the Fed to leave rates unchanged in 2026 as uncertainty about the outcome of the conflict persists and inflation remains elevated.

Strong corporate earnings validate the U.S. equity rally

Amid the backdrop of continued geopolitical and monetary policy uncertainty, corporate earnings provided a solid foundation for an impressive U.S. equity rally in April. By the end of the month, nearly two-thirds of S&P 500 companies had released their first-quarter results, with 84% posting earnings per share (EPS) above estimates, which is well above both the five- and 10-year averages. If this trend sticks, it would be the highest percentage of S&P 500 companies posting positive EPS surprises since early 2021.

The robust U.S. earnings backdrop helped support the S&P 500’s double-digit April rally and reinforced investor confidence in the durability of the U.S. equity market.

The U.S. was not the only region that posted equity market gains in April. In some emerging markets, energy-exporting countries benefited from higher oil prices, supporting stronger equity performance. Meanwhile, Asian markets such as Korea and Taiwan saw outsized gains, driven in part by booming demand for semiconductors and technology exports related to artificial intelligence.

Looking forward: The outlook remains uncertain

While strong earnings and a perceived reduction in the risk of a prolonged energy disruption helped fuel April’s equity rally, the path ahead is likely to remain volatile as markets continue to grapple with elevated oil prices and their impact on the global economy.

As we turn the page to May, we continue to believe investors who focus on maintaining portfolios that are diversified across regions and asset classes could be better positioned to navigate periods of volatility and change.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Global Investment Strategist