A look at the present-day U.S. racial wealth gap

Editorial staff, J.P. Morgan Wealth Management

- There’s a notable difference in wealth between different groups of people in the United States, which can be examined through lenses including gender, age and race.

- Hispanic and Black households earned lower yearly incomes than Asian and White households in 2020, exacerbating discrepancies in gross wealth rates between these groups.

- Improving economic opportunities across all communities and races is an important step toward improving the financial health of the nation as a whole.

What’s the wealth gap?

In the United States, there’s a notable difference in wealth between different groups of people, which can be examined through a number of lenses including gender, age and race. On an individual level, a person’s wealth comprises many factors such as debt, liquid assets, inheritances and yearly income. The wealth gap is calculated by considering the financial circumstances of all individuals in a given group and then comparing that group to other groups of individuals who’ve been similarly categorized.

Understanding the wealth gap in the U.S.

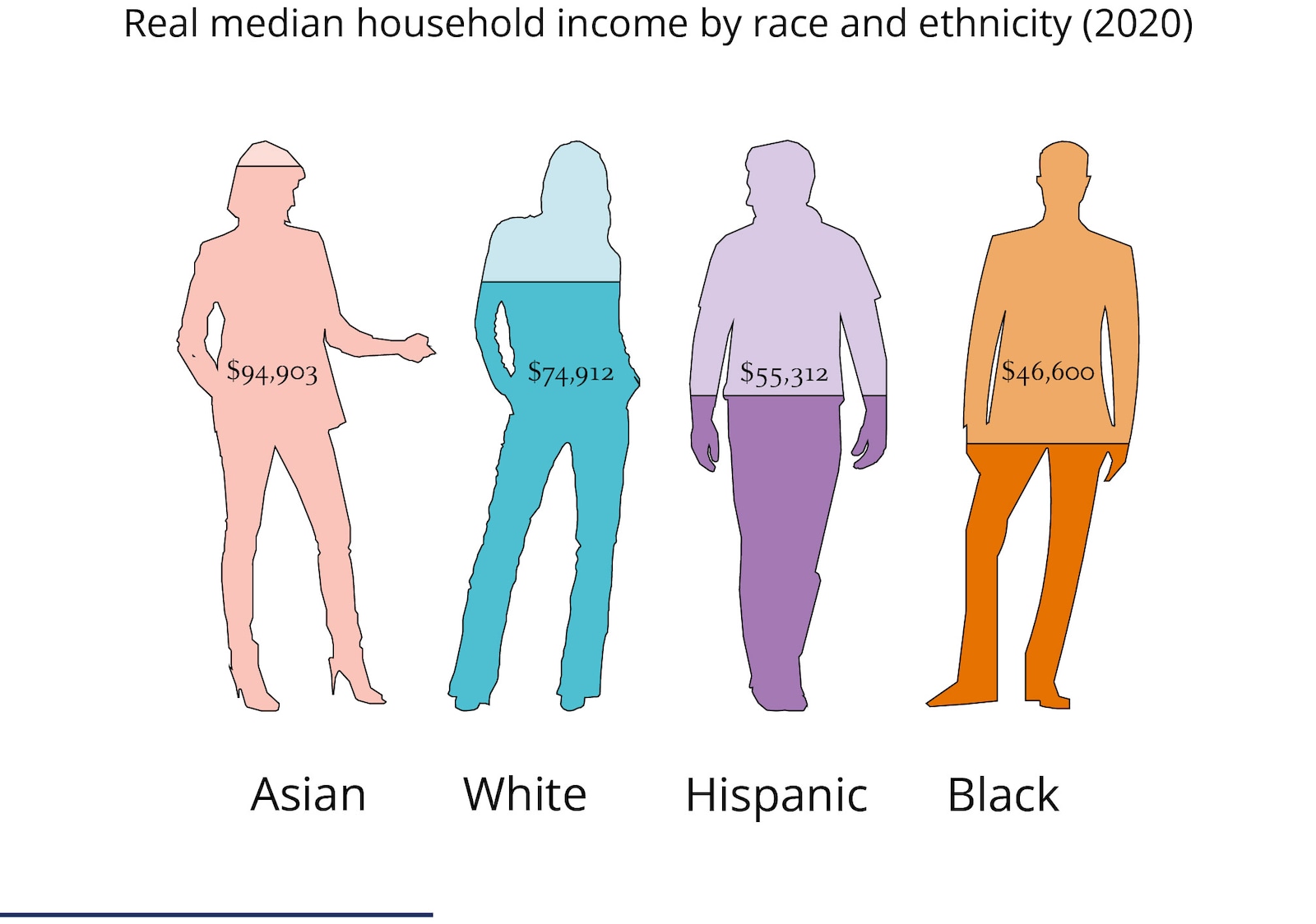

What did income disparity look like in 2020?

The above figure highlights an important aspect of the wealth gap – yearly income. In 2020, Asian households had the highest income compared to White, Hispanic and Black households, bringing home a median yearly pay of $94,903. The second highest earner of the four groups was White households, with a 2020 median yearly income of $74,912. The two groups with the lowest yearly median incomes were Hispanic and Black households, earning $55,312 and $46,600, respectively.

In 2020, the average wealth per White household was $1.2 million, while for Black households it was $279,100, and for Hispanic households it was $234,300. Considering that Black and Hispanic households have lower gross wealth rates on average to begin with, for them to rank the lowest among median yearly incomes for 2020 is especially harmful to their overall financial health.

On top of earning less in 2020, Hispanic and Black households also depleted their savings more rapidly during the peak of COVID-19 quarantine restrictions and associated lower-income job loss. In 2020, the U.S. labor market saw a decline of roughly 13.7 million full-time workers, with the largest amount of losses among lower-earning jobs, which are predominantly held by men and women of color.

The hardest hit demographics for full-time job loss in 2020 were Black and Hispanic women, whose percent declines were 13.1% and 17.4%, respectively. Comparatively, fewer White and non-Hispanic full-time workers lost their jobs in 2020, due largely to the fact that more employees with higher-earning full-time roles were able to continue working throughout the worst of the 2020 pandemic in a safe and remote fashion. For further reference, the percent change of overall unemployment rates from 2019 to 2020 was lowest for Whites at 4% and highest for Hispanics at 6.1%.

Why does this matter?

Aside from the fact that it’s socially demoralizing that we still haven’t achieved a more equal economic footing across races in America, the wealth gap is also bad for the economy. The racial wealth gap is predicted to lower national gross domestic product (GDP) by 4% to 6% by 2028 as a result of over $1 trillion in lost investments from 2019 to 2028. To be a truly healthy nation, the U.S. must improve economic opportunities across all communities and races.

JPMorgan Chase has made a $30 billion commitment toward tackling present-day U.S. race-related financial disparities. This commitment will support housing and homeownership, minority-owned businesses, financial health and workforce diversity. Read more about it here.

Invest your way

Not working with us yet? Find a J.P. Morgan Advisor or explore ways to invest online.

Editorial staff, J.P. Morgan Wealth Management