What are required minimum distributions, and why do they matter?

Vice President, Product Manager, J.P. Morgan Wealth Management

- Required minimum distributions (RMDs) are required annual withdrawals from certain tax-deferred accounts, with each year’s amount being determined per IRS rules.

- However, not all tax-advantaged retirement accounts have RMDs – Roth Individual Retirement Accounts (IRAs) do not require their original owners to withdraw during their lifetime.

- Effective January 1, 2024, Roth qualified retirement plan accounts (i.e., Roth 401(k), Roth 403(b), etc.) no longer have pre-death RMDs, aligning with the rule for Roth IRAs.

- Recipients should consider the tax implications of RMDs.

- Talk to your financial advisor about your RMDs.

- Please note this article will discuss RMDs for the original account owner; inherited retirement assets follow rules set by the IRS that won’t be covered in this article.

Many tax-advantaged retirement savings accounts and plans require you to start taking money out of the account or plan when you meet criteria determined by the Internal Revenue Service (IRS). These withdrawals are called required minimum distributions (RMDs). Knowing what RMDs are and how they will affect your wealth in retirement is important in building your overall retirement strategy.

Understanding the tax implications of RMDs can influence your overall tax liability in retirement. Consulting with your legal and tax advisors might help you navigate these complexities.

Thinking about retirement?

No matter what life stage you’re at, it's always the right time to plan for retirement.

Which accounts do RMDs apply to?

RMDs apply to certain Individual Retirement Accounts (IRAs) and retirement plans, excluding Roth IRAs of original owners. Roth IRAs are funded with post-tax income, and the IRS does not require you to withdraw and pay income tax on your earnings the same way it does with traditional IRAs and retirement plans. Traditional IRAs, 401(k)s and other plans allow for “pre-tax” contributions, meaning you may be able to take a deduction for your contributions and pay taxes on those amounts, and earnings, when they are withdrawn.

RMDs apply to:

- Traditional IRAs

- SEP (Simplified Employee Pension) IRAs

- 401(k) and 403(b) retirement plan accounts

- SARSEP (Salary Reduction Simplified Employee Pension) plans

- SIMPLE (Savings Incentive Match Plan for Employees) IRAs

Currently, original owners of these plans must begin taking RMD payments at age 73. The first year’s RMD can be delayed until April 1 of the following year; however, RMDs for all subsequent years must be taken by December 31. The minimum amount that must be withdrawn annually is determined by a formula provided by the IRS based on the year-end account balance, your current age and your life expectancy.

Retirement accounts that are subject to the RMD rules include profit-sharing plans, 401(k) plans, 403(b) plans and 457(b) plans. Annual RMDs for employer-sponsored retirement plans like 401(k)s generally follow similar RMD age rules or, if later and permitted by the plan, RMDs can begin for the year in which the account owner retires.

Not all tax-advantaged retirement accounts have RMDs, with Roth IRAs for original account owners representing a key exception. This type of retirement account does not have an RMD requirement, and effective January 1, 2024, Roth-qualified retirement plan accounts (i.e., Roth 401(k)s, Roth 403(b)s, etc.) no longer have pre-death RMDs, aligning with the rule for Roth IRAs.

All tax-advantaged retirement accounts that are treated as inherited are subject to RMD rules; however, as noted above, these rules are beyond the scope of this article.

How are IRA RMDs calculated?

The formula for calculating IRA RMDs is to divide the balance of your retirement account on December 31 of the previous year by a “life expectancy factor” published by the IRS in three different tables.

- Single Life Expectancy Table I. This table may be used for an inherited IRA.

- Joint Life and Last Survivor Expectancy Table II. This table is used if the sole beneficiary of the account is your spouse and your spouse is more than 10 years younger than you.

- Uniform Lifetime Table III. This table is used for unmarried account owners, married owners whose spouses aren't more than 10 years younger than the owner and married owners whose spouses aren’t the sole beneficiaries of their IRAs.

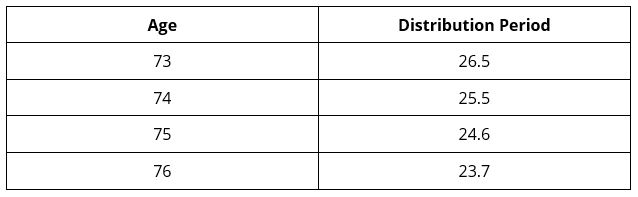

This is an example of a Uniform Lifetime Table III RMD calculation.

If you had an account balance of $100,000 in your traditional IRA on December 31 of the prior year, and you are 73 years old, you divide the $100,000 balance by 26.5, which gives you an RMD of $3,773.58. If you were 74, the RMD would be $3,921.57; if you were 75, it would be $4,065.04; and so on. The more money you have, and the older you are, the larger your RMD will be.

What is the impact of an RMD on your retirement planning?

In the example above, the annual RMD of $3,773.58 doesn’t seem like a lot of money, but RMDs on top of other kinds of income in retirement can tip the scales on your tax burden. When retirees are in a lower tax bracket or when the markets decline, they may sometimes choose to convert their traditional retirement accounts into Roth accounts, and then, when and if eligible, take tax-free “qualified distributions” (as defined by the IRS). This can help manage the tax burden when withdrawing from your retirement assets. Without careful tax planning, RMD requirements could end up costing you more money in taxes than you may have anticipated. It is crucial to understand how RMDs fit into your overall retirement strategy.

Invest your way

Not working with us yet? Find a J.P. Morgan Advisor or explore ways to invest online.

Vice President, Product Manager, J.P. Morgan Wealth Management