Trump Accounts for kids are now available: A guide for parents on rules, considerations and steps to open one for your child

Editorial staff, J.P. Morgan Wealth Management

- Trump Accounts launched in July 2026.

- Any child under 18 with a Social Security number may be eligible for a Trump Account.

- Children born between January 1, 2025, and December 31, 2028, who are U.S. citizens can receive a $1,000 government deposit to their Trump Account.

- Up to 25 million children age 10 or younger who live in qualifying ZIP codes may receive a $250 charitable gift deposit to their Trump Account from the Michael & Susan Dell Foundation. These children must have been born before January 1, 2025, and are therefore ineligible for the $1,000 government deposit.

- Account funds are invested according to regulatory guidelines and are subject to distribution restrictions until December 31 of the year the child turns 17 (referred to as the “growth period”).

Saving for your child’s future can feel overwhelming, but a new federal program offers families an additional way to save and invest for their children. Under a provision of the One Big Beautiful Bill Act (OBBBA), children under age 18 with a Social Security number are eligible for a Trump Account – an investment account designed to help families build wealth for the next generation.

Depending on your child’s birth date, age and where they live, their Trump Account may start with a $1,000 government deposit (“seed” money); a “qualified general contribution” from a charitable organization, state or other approved entity; or no deposit. For children who are eligible for an account – regardless of initial deposit – family members, other individuals and even employers can contribute each year, up to annual limits, until the end of the growth period.

Trump Accounts launched in July 2026. Here’s what you need to know about how the accounts work, who’s eligible for them and how they compare to other ways to save and invest for your child.

What are Trump Accounts?

Trump Accounts are a new type of tax-advantaged investment account for children created under the OBBBA. Accounts are available to certain children under age 18 with a Social Security number. The U.S. government will fund $1,000 deposits for eligible children born between January 1, 2025, and December 31, 2028, while a $6.25 billion gift from the Michael & Susan Dell Foundation will fund $250 charitable deposits for qualifying children in certain ZIP codes. While not all children qualify for federal or charitable funding, families, as well as other individuals and employers, may contribute up to the annual limit. There is a limit of one Trump Account per child.

Trump Accounts are subject to an annual contribution limit of $5,000 per child per year during the growth period (indexed for tax years after 2027). This limit applies to contributions from parents, family, other individuals and employers, but it does not apply to the Treasury’s $1,000 seed money, qualified general contributions and qualified rollover contributions.

Learn how Trump Accounts can support your child’s future

Build lasting financial security for your child with a tax-advantaged Trump Account and help them save for retirement and other future goals.

Who is eligible for a Trump Account and the federal or charitable deposits?

Trump Accounts are available to children under age 18 with a Social Security number. However, the types of deposits your child may receive – if any – depend on their birth date, their age and where they live:

- A $1,000 federal seed deposit is available for eligible children born between January 1, 2025, and December 31, 2028.

- A $250 Dell charitable deposit is available for up to 25 million children age 10 or younger (but born before January 1, 2025) living in ZIP codes with median incomes below $150,000.

- Other eligibility-based charitable deposits may also be available with amounts, timing and criteria determined by each program. For example, Dalio Philanthropies pledged to provide $250 deposits for eligible children in Connecticut.It’s possible that more organizations may sign on for similar charitable gifts in the future.

How to open and fund a Trump Account

You can open a Trump Account by filing IRS Form 4547Opens overlay or through the online portal at TrumpAccounts.gov. According to the IRS, Form 4547 may be used at any time, including when filing your income tax return. The election to open an account must be made before January 1 of the year in which your child turns 18.

All Trump Accounts are first created and held with the U.S. Treasury Department’s designated financial agent. Later, you may be able to transfer the full balance to your preferred financial institution through a trustee-to-trustee transfer.

If your child is eligible and a Trump Account has been opened for them, the Treasury Department will deposit the $1,000 seed contribution after the Treasury confirms with the initial Trump Account trustee that the account is active. Qualified general contributions, such as the Dell Foundation gift, are expected to be made by the Treasury on a periodic basis, based on the members of the qualified class as of the beginning of the quarter.

How Trump Accounts work

Trump Accounts are meant to provide a head start for savings and are intended to grow over time through investments in low-cost index funds, like mutual funds or exchange-traded funds (ETFs). The idea is that the account can grow with the market over the course of your child’s life. Like all investments, the account’s value may go up or down depending on market performance. Any gain in the Trump Account will be tax-deferred.

During the growth period, distributions from a Trump Account are generally prohibited; funds cannot be distributed except in the event of the account holder’s death or a return of excess contributions. Once the growth period ends, the account becomes subject to most standard traditional IRA rules, including with respect to contributions, investments and distributions.

Parents, family or other individuals can add money to the account, up to a yearly contribution limit of $5,000 (indexed for tax years after 2027). Employers – of both young employees who have their own Trump Account and employees who have dependents with a Trump Account – can contribute up to $2,500 per year per employee to an account as well, though this counts toward the $5,000 yearly cap. Importantly, an employer’s contribution is not considered income to either the employee or the dependent.

Tax treatment

During the growth period, in addition to the possible seed money or other qualified general contributions, a Trump Account may be funded with after-tax dollars from parents, family members and other individuals. After the growth period, annual individual contributions must comply with the otherwise applicable traditional IRA contribution rules, including account owner earned income requirements.

Tax treatment of Trump Account contributions

Federal government contribution | Qualified general contributions | Employer contributions | Other contributions | Qualified rollover contributions |

|---|---|---|---|---|

Contribution type details | ||||

$1,000 deposit for eligible children | Gifts can be made to a group of people in any amount by a state or Washington, D.C., the U.S., a tribal government or a section 501(c)(3) tax-exempt organization, and will be distributed equally to all members of the group | Up to $2,500 annually per employee, not per account, subject to the $5,000 annual limit (both amounts are indexed for inflation beginning in 2028) | Anyone else, e.g., beneficiary, parents, family or other individuals (subject to the $5,000 annual limit, indexed for inflation beginning in 2028) | Trustee-to-trustee transfer from one Trump Account to another Trump Account for the same beneficiary; rollover must be for the entire account, partial rollovers not allowed; not subject to the $5,000 annual limit |

Basis | ||||

Contribution does not create basis in the account; contributions and growth are taxable at withdrawal | Contribution does not create basis in the account; contributions and growth are taxable at withdrawal | Contribution does not create basis in the account; contributions and growth are taxable at withdrawal | Contributions create basis in the account (not taxable at withdrawal); growth is taxable at withdrawal | Basis in the original account rolls over to the new account, but the rollover does not create any additional basis in the new account |

Investment restrictions

During the growth period, funds must be invested in broad U.S. equity index funds – such as mutual funds or ETFs that track market indexes like the S&P 500 – with no leverage and annual fees and expenses capped at 0.1%. Subject to limited exceptions for cash, no other investments are permitted, including sector-specific funds.

Rollover and transfer options

During the growth period, Trump Accounts may be “rolled over” (via trustee-to-trustee transfers) to another Trump Account for the same beneficiary. The entire account must be rolled over; no partial rollovers are permitted. After the growth period, Trump Accounts are subject to the standard traditional IRA rollover and transfer rules.

How Trump Accounts compare to other saving and investing options for your child

Adam Frank, Head of Wealth Planning and Advice at J.P. Morgan Wealth Management, suggested that parents and guardians start by deciding what their savings goals are as they consider the account type that’s best for their child’s needs.

“For those focused on college expenses, 529 plans may be advantageous due to their tax-free withdrawals and flexibility in covering various educational expenses,” Frank said.

Qualified 529 expenses have been further expanded under sections 70413-70414 of the OBBBA, and since a Trump Account is in your child’s name, it may count against your child for financial aid purposes, unlike a 529 plan.

“Conversely, [Trump Accounts] can satisfy broader financial goals, such as a down payment [on a home] or career training, and provide a $1,000 head start for eligible children born from January 1, 2025, to December 31, 2028,” Frank said.

However, echoing earlier points, Frank also emphasized the following limitations:

- Restricted investment choices (generally, must be broad U.S. equity index funds, no leverage, and fees and expenses capped at 0.1%).

- A $5,000 annual contribution cap (with inflation adjustments after 2027; the government seed, Dell charitable gift and certain other charitable and government contributions do not count toward this cap).,

- Contributions from parents, family, other individuals and employers can be made only until the end of the growth period.

- The money can’t be withdrawn before the child reaches the end of the growth period, except in case of death or return of excess contributions. (“Rollovers” – trustee-to-trustee transfers – are permitted during the growth period.)

Frank advises parents and guardians to weigh these factors against their family’s priorities and tax situation to make informed decisions.

Comparing Trump Accounts, 529 plans and custodial accounts

Trump Account | 529 plan | Custodial account |

|---|---|---|

Who can open | ||

Parent, guardian or other authorized individual | Parent, guardian or other adult | Parent, guardian or other adult |

Initial deposit | ||

$1,000 federal seed for babies born between 2025 and 2028 with a Social Security number; $250 Dell Foundation charitable gift for eligible children 10 or younger born prior to 2025; no minimum required for additional deposits | Varies by state; often $0 or parent-chosen amount; no minimum required | Varies; often $0 or parent-chosen amount; no minimum required |

Who can contribute | ||

During growth period, parents, family, other individuals, employers, charities, government | Anyone | Anyone |

Annual contribution limit | ||

During growth period, $5,000 (excludes government seed, Dell Foundation charitable gift and other “qualified general contributions”) | No annual limit; most states limit total contributions | No legal limit |

Tax benefits | ||

Grows tax-deferred; taxed as ordinary income on withdrawal; potentially subject to early withdrawal tax (expect complexities around tracking pre-tax/post-tax contributions and the implications); employer contributions not deemed income to employee | Grows tax-deferred; withdrawals tax-free if used for education, otherwise taxed as ordinary income plus a 10% tax | Generally taxed at parents’ rate until child turns 19 and at child’s rate after age 19 (or as late as age 24 if full-time student) |

Who controls | ||

Authorized individual (generally parent or guardian) until end of growth period at which time the beneficiary may be able to take control of the account | Account owner | Custodian until child reaches adulthood, generally age 18 or 21 but up to 25 |

When funds can be used | ||

During growth period, distributions are restricted; after growth period subject to traditional IRA withdrawal rules (generally, anytime, for any reason) | Anytime for qualified educational expenses | Anytime for any reason |

Early withdrawal tax | ||

Yes, subject to early withdrawal tax unless an exception applies | Yes, if used for nonqualified educational expenses | No |

Given these similarities and differences, it’s important to consider your family’s unique needs and next steps.

If you’re a parent, should you open a Trump Account for your child?

J.P. Morgan Wealth Management’s Frank recommends families carefully consider their financial goals, tax situation and the unique features of Trump Accounts when deciding whether and how to use these accounts for their children’s future.

“For eligible families, there doesn’t seem to be a financial downside to getting the $1,000 government funding, even if no other money is added to the account,” Frank said. “And if your child is eligible for a contribution from the Dell Foundation gift, the Dalio Philanthropies gift or other charitable gifts, there wouldn’t be a downside to opening the account to take advantage of those gifts.”

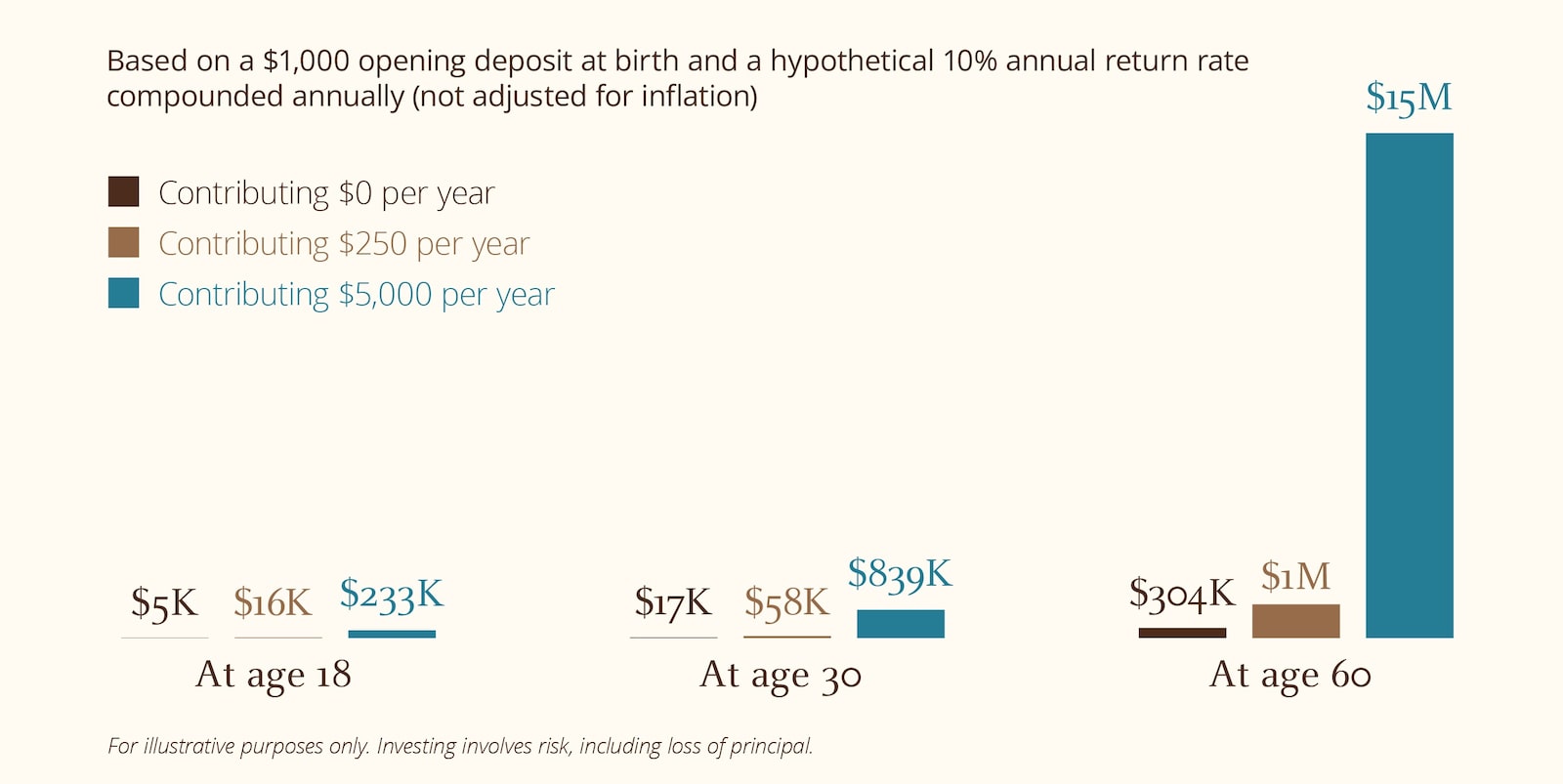

Projected Growth of a Trump Account (Hypothetical)

The above is a hypothetical example for illustrative purposes only and should not be relied upon in making an investment decision. These examples do not reflect actual or future performance results of any specific vehicle, and are based solely on the hypothetical illustration cited. Assumed starting amount is $1,000 at birth. Assumed hypothetical annual rate of return is 10%, not adjusted for inflation, and compounded annually. Investing involves risk, including loss of principal.

“These accounts allow an employer of the parent to make contributions of up to $2,500 of the $5,000 annual funding maximum without that money being considered compensation to the parent, so it might be worth parents and guardians making a $2,500 contribution if their employer will match [and that’s their requirement for contributing]. But the limit on investment options, combined with the child becoming the owner at age 18, could lead many parents and guardians to limit their contributions to these accounts.”

Frank also notes, “Qualified dividends and long-term capital gains in these accounts are taxable at ordinary income rates when withdrawn, versus UTMA accounts, where qualified dividends and long-term gains are taxed at favorable rates. By revisiting their strategy every few years, parents and guardians can adapt to any changes in congressional benefits or tax treatment to any of the account types available to them to save for their children.”

Because Trump Accounts are new, it’s not yet clear how they may affect state tax benefits, college financial aid eligibility or other government programs. Families should consult a tax or financial professional to understand how a Trump Account may impact their specific situation.

The bottom line

Trump Accounts are designed to help families begin investing for their children’s future early on. With a $1,000 head start from the federal government for eligible children or a possible $250 contribution from the Dell Foundation, the potential for contributions from other charitable organizations, and the chance to grow funds over time, these accounts may be an option worth considering for some families.

As J.P. Morgan Wealth Management’s Frank puts it: “Parents and guardians should assess their comfort level with the child gaining full control of the funds at age 18,” even though the accounts will be subject to IRA withdrawal rules. “This aspect requires careful consideration, as it involves predicting whether their newborn child will be ready to manage what could be a five- or six-figure sum of money in their teen years.”

It's for these reasons that it may be important to discuss your investment strategy for your children with financial advisors, including tax professionals, to make the most informed decision.

Frequently asked questions about Trump Accounts

Trump Accounts launched in July 2026. Parents or other authorized individuals may open a Trump Account using IRS Form 4547 or the online portal at TrumpAccounts.gov. There is a limit of one Trump Account per child.

Yes, the Trump Accounts: Official App launched on May 28, 2026, and is available in app stores. You can also download the app from TrumpAccounts.gov. You must complete Form 4547 before you can sign up for the app. Once the form is complete, you can sign up with the email address you used to sign up for a Trump Account. Once you sign up with your email, a password and your phone number, you can sign up for notifications to get updates on your child’s Trump Account once it’s active. The Treasury Department also indicated that parents who signed up for a Trump Account for their children will receive emails with steps for setting up the app. Keep an eye out for emails from this address: no-reply@TrumpAccounts.Treasury.gov.

Children born between January 1, 2025, and December 31, 2028, who are U.S. citizens with a SSN are eligible for the $1,000 government deposit into a Trump Account.

Up to 25 million children age 10 or younger (but born before January 1, 2025) living in ZIP codes with median incomes below $150,000 are eligible for the $250 Dell Foundation charitable deposit.

Children who do not qualify for the $1,000 government deposit (for example, those born before 2025) may still receive the $250 deposit if they meet the age and ZIP code requirements.

Some children may be eligible for other additional charitable deposits. For example, Dalio Philanthropies in December 2025 pledged to provide $250 deposits for eligible children in Connecticut. Other charitable contributions may also be announced.

Employers can contribute up to $2,500 per employee per year to a Trump Account, including through cafeteria plans for dependents. These contributions are not considered income to the employee or the dependent. The contributions are counted against the child’s $5,000 annual limit (indexed after 2027).

Money in a Trump Account must generally be invested in broad U.S. equity index funds – such as mutual funds or ETFs that track indexes like the S&P 500 – with no leverage and annual fees and expenses capped at 0.1%.

No withdrawals are allowed from a Trump Account before the end of the growth period, except for specific “rollovers” (trustee-to-trustee transfers), returns of excess contributions or upon death.

When a child reaches the end of the growth period, the child may be able to take control of the Trump Account, which is then generally treated like a traditional IRA, with standard rules for contributions and withdrawals. Note that children may not actually be able to take control of the Trump Account until they reach the applicable age of majority (generally age 18, but later in a few states).

After the end of the growth period, the account is generally treated like a traditional IRA, so it may be rolled over or converted to another eligible retirement account, such as a traditional IRA or Roth IRA.

No, there is no earned income requirement for contributions to Trump Accounts during the growth period.

No, during the growth period, the contribution limits for IRAs and Trump Accounts are applied separately.

Unlike 529 plans, Trump Accounts are not limited to education expenses. Once your child reaches the end of the growth period, the account is generally subject to the rules applicable to traditional IRAs, and money can be used for certain approved purposes without an additional tax, including paying for education or buying a first home. If your child doesn’t use the funds right away, they can leave the money in the account to continue growing tax-deferred. Note that at the end of the growth period, the account is subject to traditional IRA withdrawal rules, and so money can be withdrawn for any purpose subject to ordinary income taxes and an early withdrawal tax (unless an IRS exception applies).

Like any investment vehicle, there are potential drawbacks to consider. Families may have limited control over the investment options available to them compared to custodial accounts. And while the money grows tax-deferred, withdrawals are taxed as ordinary income when the money is withdrawn and may be subject to an early withdrawal tax unless an exception applies. There will also be pre-tax and post-tax contribution nuances to keep track of that may make these accounts challenging.

Giving an 18-year-old direct ownership of what could be a five- or six-figure account could be a deterrent to using Trump Accounts rather than other savings vehicles – and it’s nearly impossible for parents and guardians of a newborn or young child to know what that child will be like in their teenage years.

More broadly, some financial specialists have also raised concerns that wealthier families may benefit more from the program, since they’re more likely to contribute the full $5,000 each year. And because the program is new, there’s still uncertainty around how the accounts will operate and how they may affect college financial aid or other government benefits.

Invest your way

Not working with us yet? Find a J.P. Morgan Advisor or explore ways to invest online.

Editorial staff, J.P. Morgan Wealth Management