How policy, politics and profits are shaping market momentum

In what may be the year’s busiest 72 hours in markets, the market’s three “P’s” lined up.

- Policy is transitioning toward normalization, with central banks signaling a more data-dependent and flexible stance rather than a continued commitment to rate cuts.

- Politics delivered a few clean wins, but headline risk remains into year-end.

- And profits – still led by U.S. tech and the artificial intelligence (AI) buildout – continue to do the heavy lifting.

Here's what we focused on:

Policy: Normalization, not stimulus – global cuts are fading, balance sheets are quietly shrinking and central banks are keeping their options open

In the U.S., the Federal Reserve (Fed) delivered a small, well-telegraphed cut with “no preset course” language – setting the federal funds rate at a 3.75%–4% range. Balance-sheet runoff is winding down, guidance stayed intentionally vague and markets read Fed Chair Jerome Powell’s language as opting to manage risk rather than starting a big easing wave. Yields backed up, the U.S. dollar firmed and equities took it in stride at first. Our take: Slow and shallow – we still expect about two more cuts over the next year, not a sprint.

The European Central Bank held steady in Europe. Inflation is moving sideways while growth stabilizes, which argues for patience; the bar for additional cuts remains high, and everything is data dependent. Balance-sheet normalization continues in the background – the message: Steady hands.

Japan remained on hold as well. Wage gains are improving but not yet decisive, while fluctuations in energy prices and changes in fuel tax policy are creating uncertainty around near-term inflation. The Bank of Japan offered no forward guidance beyond “more data.” Dissenters again pushed for a hike, underscoring how balanced – rather than easy – the policy debate has become against the election backdrop.

Our take: The global rate-normalization story is either continuing or entering its final innings. Paths differ by region, but they play the same tune – shallow cuts, cautious communication and policy makers determined not to reignite inflation.

Politics: Two headlines, limited macro bite (so far)

This week it was all about the U.S. government shutdown clock and a U.S.–China timeout – one only matters if it breaks the data, while the other cools tempers without changing the rules.

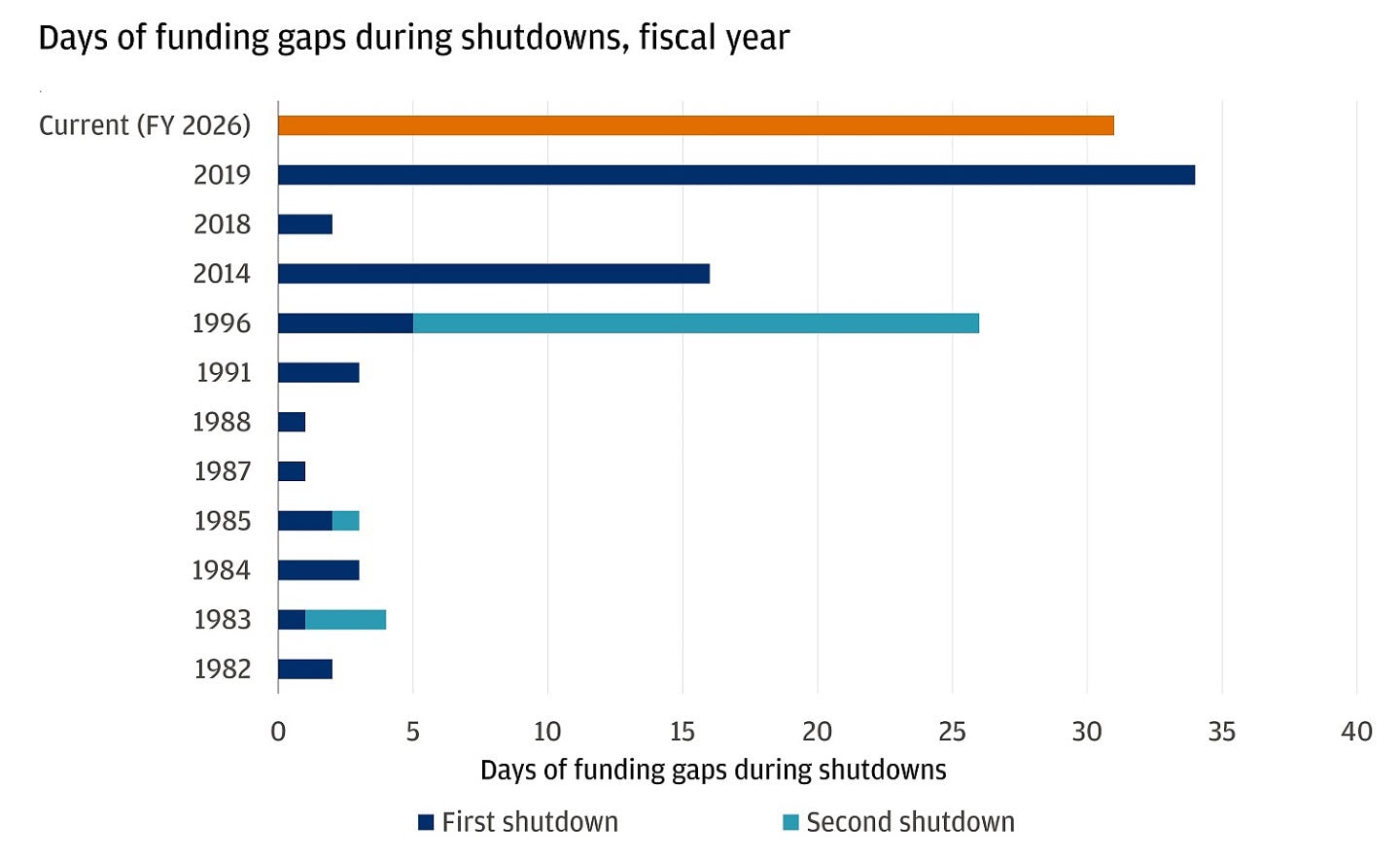

At day 31 – inching toward the longest on record – the U.S. government shutdown has been a headline more than a hit, and the main risk to investors is a prolonged period of missing official economic data. With Labor Department staff furloughed, the October Consumer Price Index (CPI) could be delayed or skipped, and it’s likely that October’s employment report will also be delayed, pushing investors to lean once again on various proxies (ADP, card-spend, regional Fed nowcasts) to get a pulse check on the economy.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

Beyond the data, the shutdown matters for how we think about near-term economic growth: Each week reduces quarterly annualized gross domestic product (GDP) growth by approximately 0.1–0.2 percentage points, and a month results in a decline of about 0.4–0.8 percentage points. Most of this lost growth typically rebounds once the government reopens, although hours lost to furloughs do not recover. The near-term pinch is expected to start on November 1 as funding for the Supplemental Nutrition Assistance Program (SNAP) is scheduled to run out, which could impact about 40 million people. Each pay period adds more pressure on Washington to end the shutdown, as more people go on without pay for longer.

The shutdown is the second longest in history

Meanwhile, the meeting between President Donald Trump and China’s President Xi Jinping in South Korea delivered a pause, not a pivot – a one-year truce with selective tariff relief and a restart of some flows (soybeans, rare minerals). The deal stabilizes relations but doesn’t resolve deeper issues or deliver major structural changes to the U.S.–China trade imbalance; in other words, U.S. export controls on semiconductors and AI – including Nvidia’s status – remain in place. Both sides keep derisking. Markets read it as a timeout, not a turn.

Our take: Politics isn’t driving markets right now. The shutdown only bites (in markets) if it blocks the official data (like CPI) for a prolonged period where proxies don’t cut it. The U.S.–China truce cools the temperature but doesn’t change export controls or earnings. So the focus stays on profits – especially AI-led capital expenditures (capex) – unless one of these turns into a real policy shock.

Profits: Earnings are doing the heavy lifting – AI is the engine, breadth is the story

This week’s strength came from companies beating expectations and nudging guidance higher. Mega-cap tech set the tone, but the support is broader: Results and management commentary point to a steady consumer, solid credit and execution through policy noise.

So far, about 61% of the S&P 500 has reported. 82% have beaten earnings per share (EPS) estimates – well above five- and 10-year averages – and about 79% have topped on revenue. The Street now tracks 10.5% year-over-year earnings growth for Q3, up from about 7% heading in.

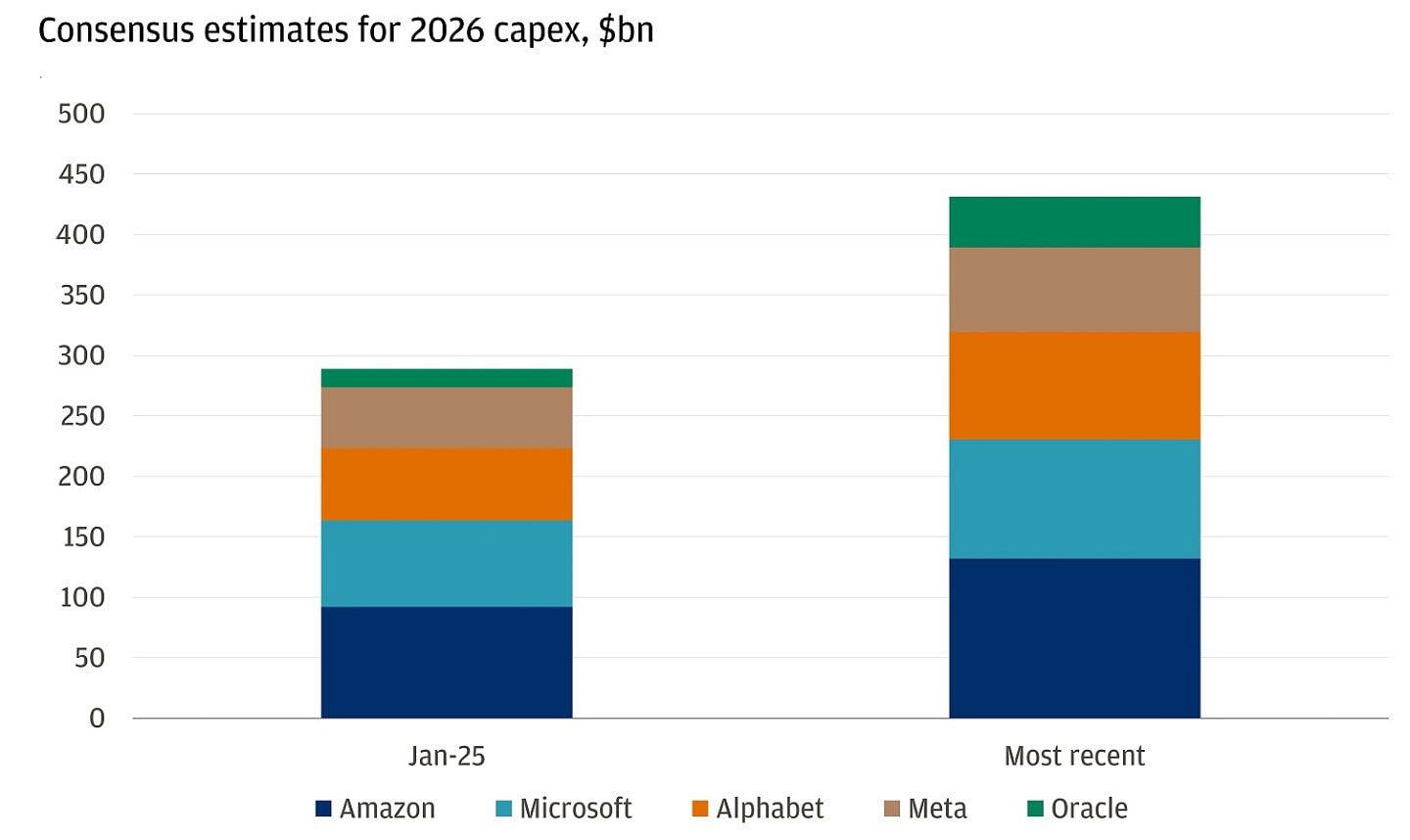

The hyperscalers reinforced the theme. Alphabet, Microsoft and Amazon generally beat; when stocks lagged, it was mainly due to earnings beats that were smaller than investors have come to expect, or concerns about higher capex. AI spend stepped up again – cloud units were a bright spot – and management tone stayed confident (Microsoft expects to “roughly double [its] data-center footprint over the next two years” to meet demand). The five hyperscalers (Alphabet, Microsoft, Meta, Amazon and Oracle) initially guided to $285 billion of capex in fiscal year (FY) 2026, and today that expectation stands at $431 billion.

Hyperscaler capex expectations have surged this year

Outside the megacaps, messages were consistent: Resilient consumer spend, stable deposits/credit and no broad-based weakness. As Wells Fargo’s CEO Charlie Scharf put it, “You see really strong credit results. You see strong consumer spend and stable deposits … [that] paint a picture of a consistently strong consumer.” Tariff effects have been less severe than feared, with teams highlighting pricing power, operating efficiencies and a friendlier rates/regulatory backdrop into 2026.

The bottom line

Profits – not headlines – are driving momentum. Broad beats plus rising AI capex keep the path of least resistance higher, so long as the macro doesn’t deliver a true policy shock.

All market and economic data as of 10/31/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.