Beyond bonds: How to protect against inflation-led shocks

Executive Director, Head of U.S. Wealth Management Portfolio Advisory Group

Labor market cools; price increases trickle through

This week was all about the anticipation of Federal Reserve (Fed) Chair Jerome Powell’s Jackson Hole remarks, and markets entered wait-and-see mode. The S&P 500 rally took a breather, while U.S. rates barely budged. In the macro backdrop:

- The labor market showed more signs of a slowdown. There were more first-time filers for jobless claims than there were last week, and the number of people filing continuing claims also rose more than expected. This points to cooler employment conditions and easing labor demand.

- Price increases are trickling through to consumers. Earnings reports from major U.S. consumer retailers suggested as much: Walmart said that its costs have been rising every week due to tariffs, although the company still managed to expand its gross margins by +26 basis points as sales rose more than expected – perhaps as consumers seek discounted goods amid economic uncertainty. Meanwhile, Target saw margin compression – evidence that not every company can offset rising input prices with either better sales or pass-through of higher costs.

All in all, an economic slowdown is already happening. In the first half of the year, gross domestic product (GDP) growth ran at 1.2%, less than half the pace of 2024 (not new news, but useful context). Looking ahead, our economists see the balance of risks tilted more toward an acceleration of inflation than toward rising unemployment or recession.

This raises the question, what works in an inflation-skewed environment? When inflation – not growth dynamics – drives the tape, bonds are less effective in hedging against stock market volatility. That reality should prompt investors to consider what actually works for diversification.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

Bonds may be a less effective hedge against stock market pressure during inflation shocks

For most of the last 30 years, bonds were the go-to shock absorber when stocks cracked. In that regime, core bonds reliably protected against equity drawdowns. From 1997 to 2020, the S&P 500 saw 10 pullbacks of more than -10%; in nine of them, U.S. Treasuries rose, delivering an average total return of about +7%.

This pattern had a simple engine: Most sell-offs were triggered by growth scares, not price shocks. When growth deteriorated – or markets feared it would – the Federal Reserve was expected to cut benchmark interest rates, so yields would fall and bonds would rally, cushioning equity losses. That’s the key: What drives the slowdown shapes correlation: Bonds can be a good hedge in growth shocks; during inflation shocks, bonds and stocks can fall together.

Then the regime flipped. Post-pandemic, the dominant shock was inflation, not growth. As the pace of price increases ran to highs not seen since the late 1980s, the Fed tightened aggressively. Higher policy rates pushed yields up (sending bond prices down) while compressing equity valuations – so stocks and bonds weakened together. That’s why stock-bond correlation moved higher, and the old “bond-as-insurance” playbook stopped working as well.

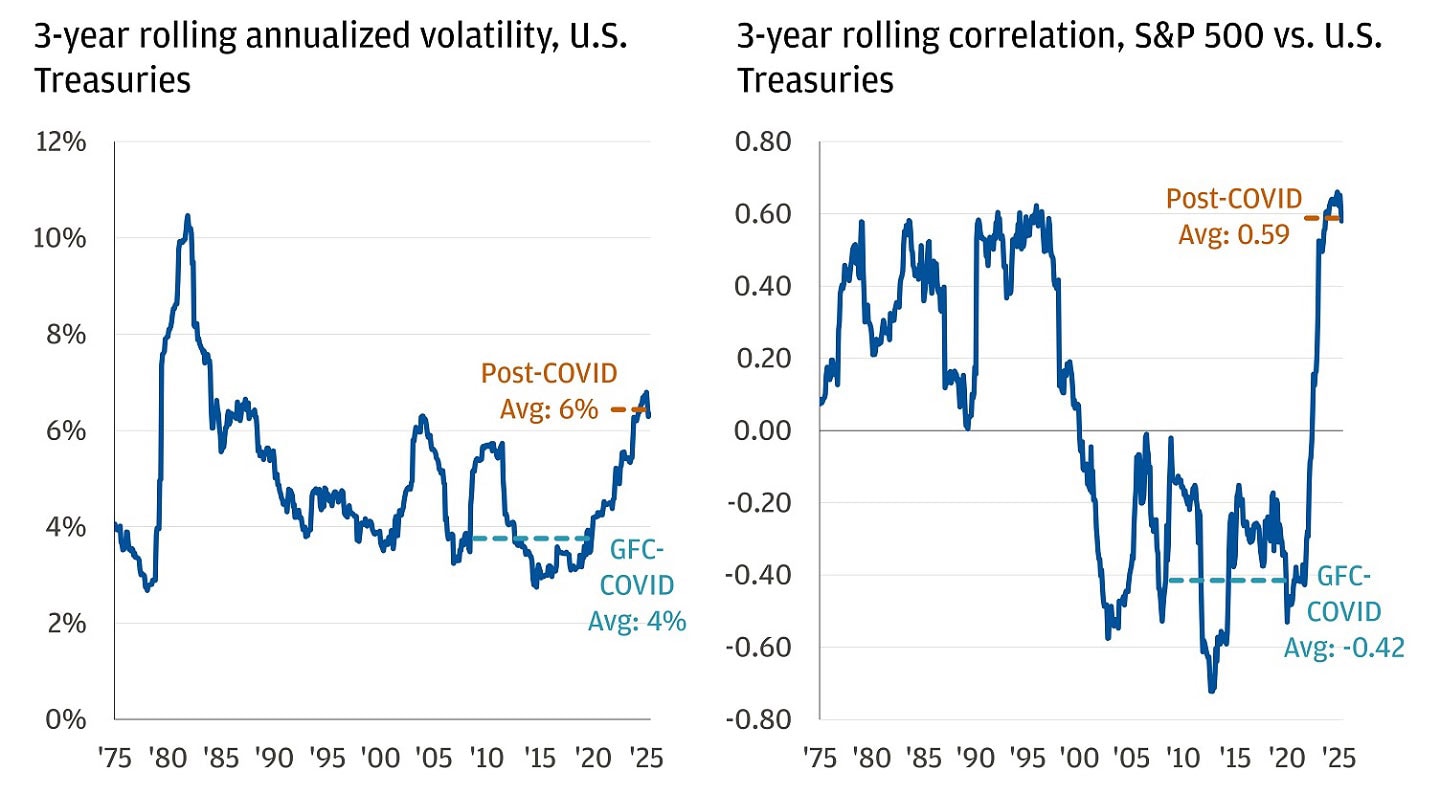

Since the height of the COVID-19 pandemic, the S&P 500 has had three drawdowns of at least -10%. In two of them, U.S. Treasuries finished negative – most notably in 2022, when the U.S. Treasury index fell -13% while the S&P 500 dropped -24%. In other words, the usual hedge didn’t show up. Since 2020, bonds have been more volatile and have displayed a stronger relationship to stocks (higher correlation) than in the prior two decades – both symptoms of higher, more volatile inflation.

Since COVID, bond volatility has increased …& stock/bond correlation has turned positive

It is not possible to invest directly in an index.

Now bond yields have reset higher to reflect inflation risk. At the 2020 trough, the Bloomberg U.S. Aggregate bond market yielded about 1%; today it’s about 4.5% – an approximate 350 basis points step-up.

Meanwhile, inflation has cooled sharply – from an approximate 9% year-over-year peak in 2022 to around 3% today. With growth slower, markets are pricing in about 100 basis points of Fed cuts over the next 12 months, and we agree. The expectation is for the Fed to prioritize the employment side of its dual mandate by easing policy.

Bonds have benefited from the reset in inflation and policy expectations. The Bloomberg U.S. Aggregate is up over 4% year-to-date and has outpaced cash. To the extent economic growth slows even more than expected, yields should fall further and bonds should continue to rally. Look no further than the disappointing payrolls report on August 1: The S&P 500 fell over -1.5%, while the U.S. Treasury index gained nearly +1%. That’s why we still view core bonds as the second-best protection asset against equities.

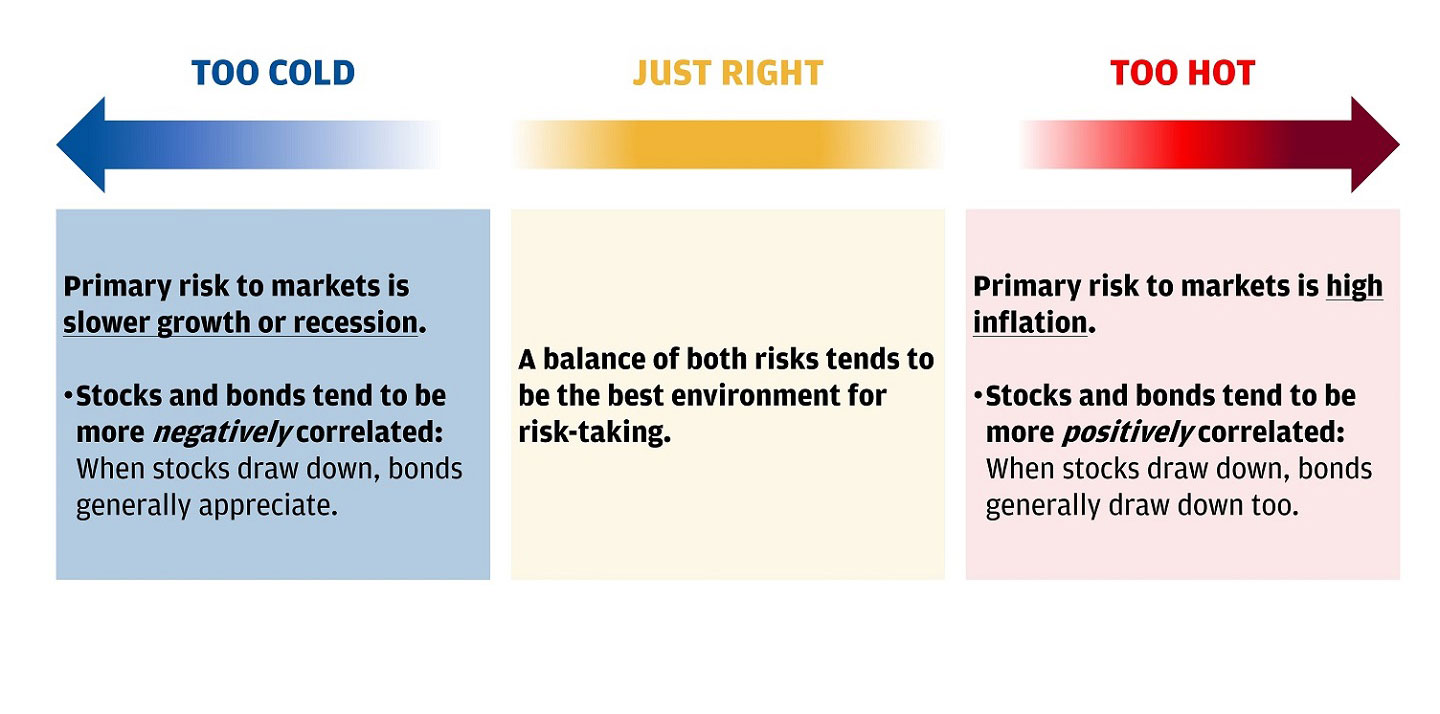

But what if the next equity drawdown is inflation-led, not growth-led? For most of the last 30 years, inflation sat below the Fed’s 2% target, so growth scares (“too cold”) dominated and bonds usually rallied when stocks sold off. Today, factors like deglobalization, U.S. fiscal deficits and labor supply raise the odds that inflation spends more time above target (“too hot”) – even if it still averages about 2% over time. This would mean bonds – while still being a key hedge against recession risk – could experience more episodes of negative returns at the same time as equities. In our view, that’s why positioning for a regime where inflation is something we have to look out for – and where stock-bond correlation goes through stretches of being positive – matters now.

The stock/bond correlation framework: “Too hot vs. too cold” spectrum for the U.S. economy

So, how can investors protect against the risk that bonds won’t always cushion equity drawdowns? One potential solution is to add exposures that, like bonds, diversify equities but tend to do better when inflation is firm. Based on our Long-Term Capital Market Assumptions, the opportunities worth exploring fall into two buckets:

- Commodities, including gold

- Select liquid alternative strategies: Macro and relative value managers

These strategies carry their own risks – including higher volatility – so they should be sized to fit broader objectives and risk tolerance. In general, no more than 25% of a traditional core fixed income allocation should be shifted into these diversifiers. We still think bonds remain the cornerstone, and if you’re using them to get income and don’t plan to buy or sell them, then they should still play their part in your portfolio in the long run. But adding complementary assets can help portfolios weather both growth- and inflation-led shocks.

All market and economic data as of 08/22/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Executive Director, Head of U.S. Wealth Management Portfolio Advisory Group