What’s on the horizon for the proposed House reconciliation bill?

J.P. Morgan Wealth Management

Market update

Equities are heading to close the week higher as trade deal momentum continues and investors shift some focus to pro-growth policies.

The S&P 500 (+4.5%) and Nasdaq 100 (+6.4%) both made significant gains, with both recovering past their pre-“Liberation Day” levels. The large cap indexes largest constituents (Magnificent 7 +8.8%) and largest sector (information technology +8.0%) outperformed amid the risk-on sentiment.

In macro news, measures of consumer inflation came in muted relative to expectations, as did retail spending. Nonetheless, as investors shift their focus from the negative effects of tariffs towards the pro-growth deregulation and tax policies, yields climbed across the curve. The 2-year (3.96%) climbed seven basis points (bps) and the 10-year (4.43%) rose five basis points.

The risk on sentiment permeated into commodities markets. Oil prices rose for the second week in a row, amid lower recession odds across the sell-side, while gold declined.

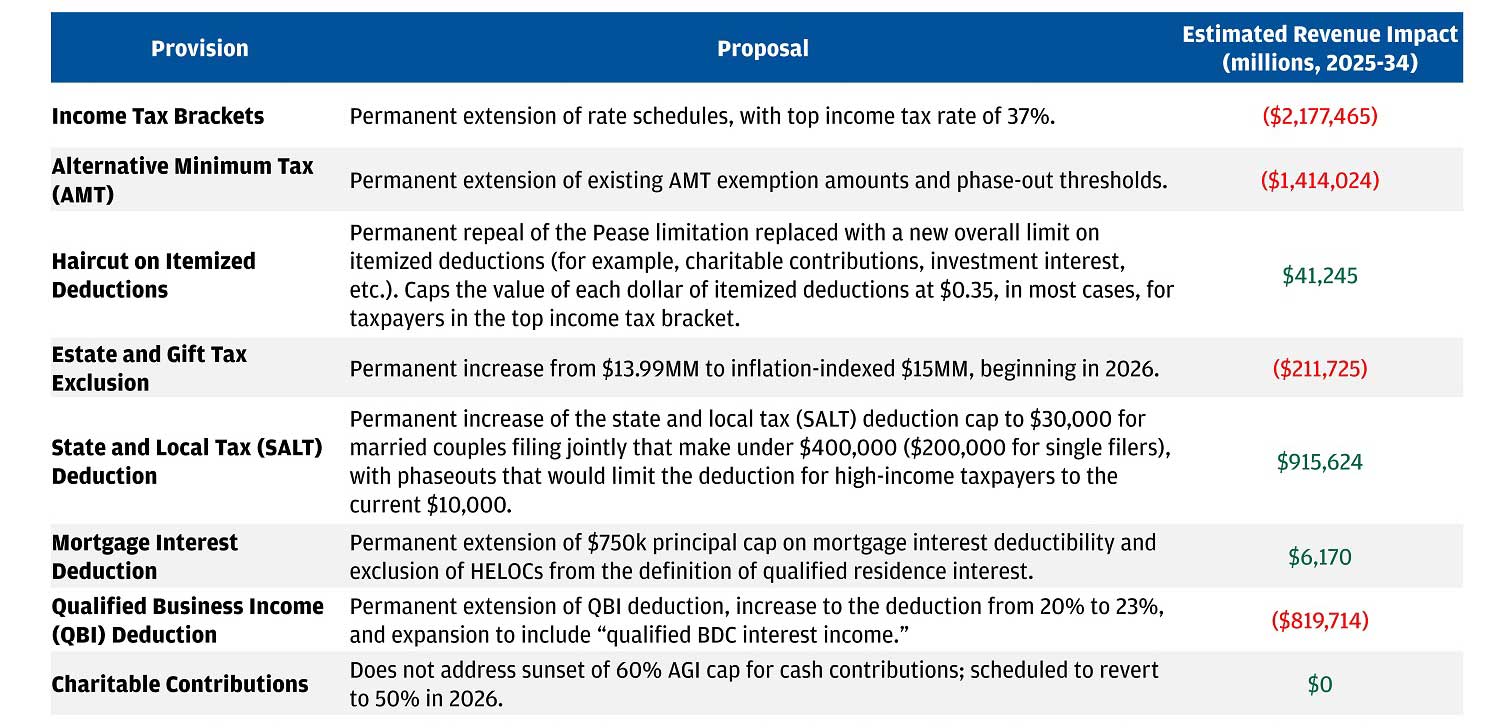

The language for the reconciliation bill – which aims to extend the Tax Cuts and Jobs Act (TCJA) – was released this week and passed by key committees on health and tax. But it was subsequently voted down in the House Budget Committee. House leaders are working to broker a compromise and re-group to address the divisions, with the Budget Committee reconvening on Sunday. Nevertheless, we dive into the language of the current working bill and what it could mean below.

Work with an advisor

Our advisors can provide ongoing financial advice on how your portfolio can adapt to the changes in the market, your life and your goals.

Spotlight

The House made significant progress with its reconciliation bill this week, and even though progress was delayed Friday, nonetheless the language allows us to assess its possible impact. In U.S. legislation, a reconciliation bill allows budget-related measures to pass in the Senate with a simple majority, bypassing the typical 60-vote threshold needed to overcome a filibuster. This process is crucial for advancing significant fiscal policies – such as tax cuts or adjustments to mandatory spending – when bipartisan support is limited. Reconciliation was the route used for the Tax Cuts and Jobs Act of 2017 during Donald Trump’s first presidency. This week, most House committees have approved their portions of the reconciliation legislation, which include an extension of that bill.

Below, we recap the TCJA’s impact on the economy and markets and what a new bill could potentially mean.

The Tax Cuts and Jobs Act of 2017 was a significant overhaul of the U.S. tax code, enacted under President Donald Trump. It aimed to stimulate economic growth by reducing tax burdens on individuals and businesses. Before the TCJA, the U.S. tax system was characterized by relatively high corporate tax rates and a complex individual tax code. The corporate tax rate stood at 35% – one of the highest among developed countries – which many argued made the U.S. less competitive globally. The individual tax system had seven tax brackets, with a top rate of 39.6%. There were numerous deductions and credits but the system was often criticized for its complexity and inefficiency.

The TCJA was a key component of President Trump’s economic agenda, aimed at boosting economic growth, job creation and investment in the U.S. The Republican-controlled Congress prioritized tax reform, seeing it as a way to deliver on campaign promises and stimulate the economy. The bill was introduced in November 2017 and passed through a budget reconciliation process. The TCJA was a landmark piece of legislation that significantly altered the U.S. tax landscape.

The draft budget resolution by the House and Senate now unlocks the process to extend that bill, with a target date of July 4. Here’s what that could mean:

Reconciliation can make expiring provisions permanent

However, extending these tax breaks is not a free lunch. When we think of the U.S. as a business – which has revenues and expenses – lowering tax rates reduces the country’s “revenue,” and if expenses (Medicare, Social Security, defense spending, etc.) are not reduced, the deficit increases.

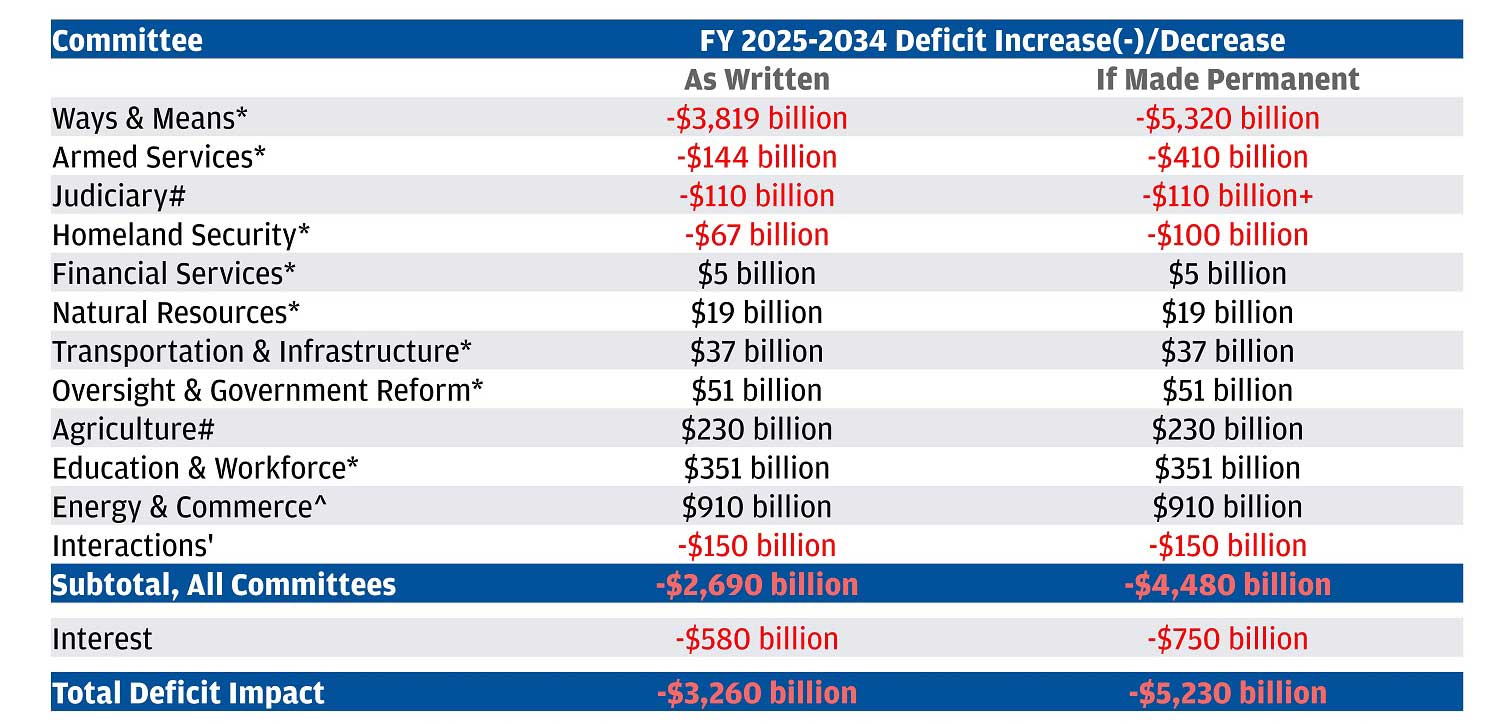

According to the Committee for a Responsible Federal Budget (CRFB), the developing House reconciliation bill is shaping up to add roughly $3.3 trillion to the debt through Fiscal Year (FY) 2034 and is setting the stage for more than $5.2 trillion of additional debt if policymakers ultimately extend temporary provisions. The CRFB estimates that by 2034 the drafted House reconciliation bill would:

- Increase debt by $3.3 trillion or $5.2 trillion if made permanent.

- Increase annual deficits to $2.9 trillion (6.9% of gross domestic product[GDP]), or $3.3 trillion (7.8% of GDP) if made permanent.

- Increase yearly interest costs to $1.8 trillion (4.2% of GDP), or $1.9 trillion (4.4% of GDP) if made permanent.

- Increase debt to 125% of GDP, or 129% of GDP if made permanent.

Deficit Impact of the House Reconciliation Package

To be clear, the bill as drafted is not final, and will likely change between now and the July 4 target date to accommodate lawmaker pushbacks, but we believe this bill could pose some risks (and opportunities) for the economy and markets. We explore those below:

For the economy: The fiscal stimulus the proposed bill provides could help partially offset some of the negative growth impacts from tariffs. We estimate a roughly -1% hit to GDP due to tariff announcements year-to-date (post-May 11 U.S.-China reductions). However, we believe that the stimulative portion of the proposed bill (extension of tax cuts, new tax cuts and spending increases) could offset two-thirds of the negative tariff impact.

On financial markets: It is likely this proposed bill increases fiscal deficits and as a result, puts upward pressure on Treasury yields in the U.S. We believe that concerns about the deficit are likely to alter the risk-reward profile of investing in longer-dated U.S. Treasury securities or securities with a comparable duration. This creates uncertainty and higher yields (term premium) at the longer end of the Treasury curve.

With that backdrop in mind, we think the latest draft of the bill may create investment opportunities.

Within fixed income: We prefer the risk-reward offered at the belly (roughly five years) of the curve and in. This part of the curve is relatively less affected by the trajectory of U.S. debt and macroeconomic uncertainty and more affected by the Fed. We have confidence that the next move the Federal Reserve makes is a cut rather than a hike and as a result, we have more conviction in the short end of the curve.

Moreover, for taxable investors in the U.S., the draft does not modify the municipal tax exemption. The seasonal supply/demand dynamics have led to a substantial cheapening in municipal bonds from a valuation perspective. From a fundamental perspective, the municipal bonds market is of very high quality. Since 1970, the 10-year cumulative default rate for investment-grade (IG) municipal bonds has been just 0.1% (versus 2.2% for IG corporates). If heightened deficit fears put upward pressure on yields, we think that is an opportunity for investors to leg into municipal bonds.

As for equities: Increasing the fiscal stimulus in the U.S. could be a tailwind for stocks. Financials remain one of our preferred sectoral implementations in the U.S. Net interest margins and net interest income are set to inflect higher while capital markets activity is also poised to meaningfully accelerate. Credit conditions remain benign while the regulatory environment likely eases. This backdrop is favorable for banks and capital markets companies and becomes more attractive in a steeper yield curve environment.

Infrastructure investment: For investors looking to avoid rate volatility that can arise amid higher fiscal deficits, we think infrastructure can add resilience to portfolios. Infrastructure investments can offer diversification and consistency, providing essential services with high barriers to entry and long-term contracts that include inflation escalators.

For questions on how the proposed reconciliation bill could affect your portfolio, reach out to your J.P. Morgan advisor.

All market and economic data as of 05/16/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

Explore ways to invest

Take control of your finances with $0 commission online trades, intuitive investing tools and a range of advisor services.

J.P. Morgan Wealth Management