How to better position portfolios before the hard data changes

J.P. Morgan Wealth Management

Market update

Markets are heading lower to close the week, despite a jolt from positive trade news out of Washington yesterday.

Heading into Friday, the S&P 500 (-0.4%) and Nasdaq 100 (-0.2%) are both underperforming European (+0.1%) and Japanese (+0.4%) equities.

However, the S&P 500 has essentially recovered all of its losses since Liberation Day, while the Nasdaq 100 has gained +2.5%. Since it’s April 8 trough, the S&P 500 has managed to gain +14% and the Nasdaq is up +17%, both outperforming European (+11%) and Japanese (+11%) stocks.

Outside of the price action though, the sentiment heading into Friday is positive in the U.S. after President Donald Trump announced a trade deal with the U.K. Thursday morning, before trade talks with China commence this week. The deal encompasses the U.K. lowering auto tariffs to 10% and eliminating metals duties, while the U.S. will reduce duties on British steel, aluminum and autos. The agreement, still pending final details, also includes a tariff-free quota for British beef and plans for a digital trade deal.

This was announced before U.S. and Chinese leaders are to meet this weekend in Switzerland to discuss trade. The delegation will be led by U.S. Treasury Secretary Scott Bessent and Trade Representative Jamieson Greer, with Vice Premier He Lifeng representing China. The talks aim to de-escalate the tariff standoff, with U.S. tariffs at 145% and Chinese retaliatory tariffs at 125%. Both nations are incentivized to reduce tariffs to prevent severing trade links. While the discussions have sparked market optimism, expectations are tempered by negotiation complexities and strategic uncertainty. We do not expect easy tariff relief.

In macro news this week, the Federal Reserve (Fed) left their target interest rate policy range unchanged at 4.25% to 4.5%. Chair Jerome Powell and the Federal Open Market Committee (FOMC) feel that their policy rate, which is modestly restrictive as it stands, is in a good position for them to take a “wait-and-see” approach to monetary policy (more on that below).

In fixed income, yields are heading higher into the week close. The 2-year (3.87%) is higher by four basis points, while the 10-year (4.38%) climbed seven basis points.

In commodities, oil (+2.5%) looks to snap a two-week losing streak amid the improved trade war narrative, while gold (+2.6%) continues its climb.

Below, we dig into the hesitation markets have faced amid uncertainty and the actions you can take in portfolios right now.

Work with an advisor

Our advisors can provide ongoing financial advice on how your portfolio can adapt to the changes in the market, your life and your goals.

Spotlight

A wait and see market. While having cooled from recent peaks, economic uncertainty remains elevated. As a result, much of the impacts of uncertainty haven’t hit the hard data (e.g., gross domestic product [GDP], employment rates, etc.) yet. The economic data that is reported today does not include the potential tariff impacts of tomorrow. This has resulted in a slew of “wait-and-see” pockets:

In economic data: Real GDP declined -0.3% in Q1 2025. A major caveat to the headline print was the distortion of the underlying data due to net exports detracting 4.8% from the headline figure, which is the largest-ever drag on growth from net exports. We identified that a better indicator of growth in the economy was domestic demand (consumer spending plus private fixed investment). Domestic demand added 2.5 percentage points to GDP growth, exactly in line with Q4 2024’s GDP. Using this measure, the economy seems to be growing in line with Q4 of last year, though we expect this growth to moderate as tariffs flow through the economy. As a result, we are more likely to see the effects of demand destruction leading to weaker growth from tariffs in the data prints for Q2 2025 through the end of the year.

From the Federal Reserve: Chair Powell noted this week that risks to the growth and inflation picture have increased because of tariff uncertainty and deterioration in the soft data (subjective indicators e.g. surveys, sentiment). However, the Chairman noted that this deterioration is not seen in the hard data quite yet. The economy is still expanding at a solid pace, the labor market is not showing any immediate signs of distress and inflation is only modestly above the Fed’s target. Powell and the FOMC feel that the best action for their policy rate, which is modestly restrictive as it stands, is to leave policy where it is and make a policy change when the data is giving clearer signs to do so.

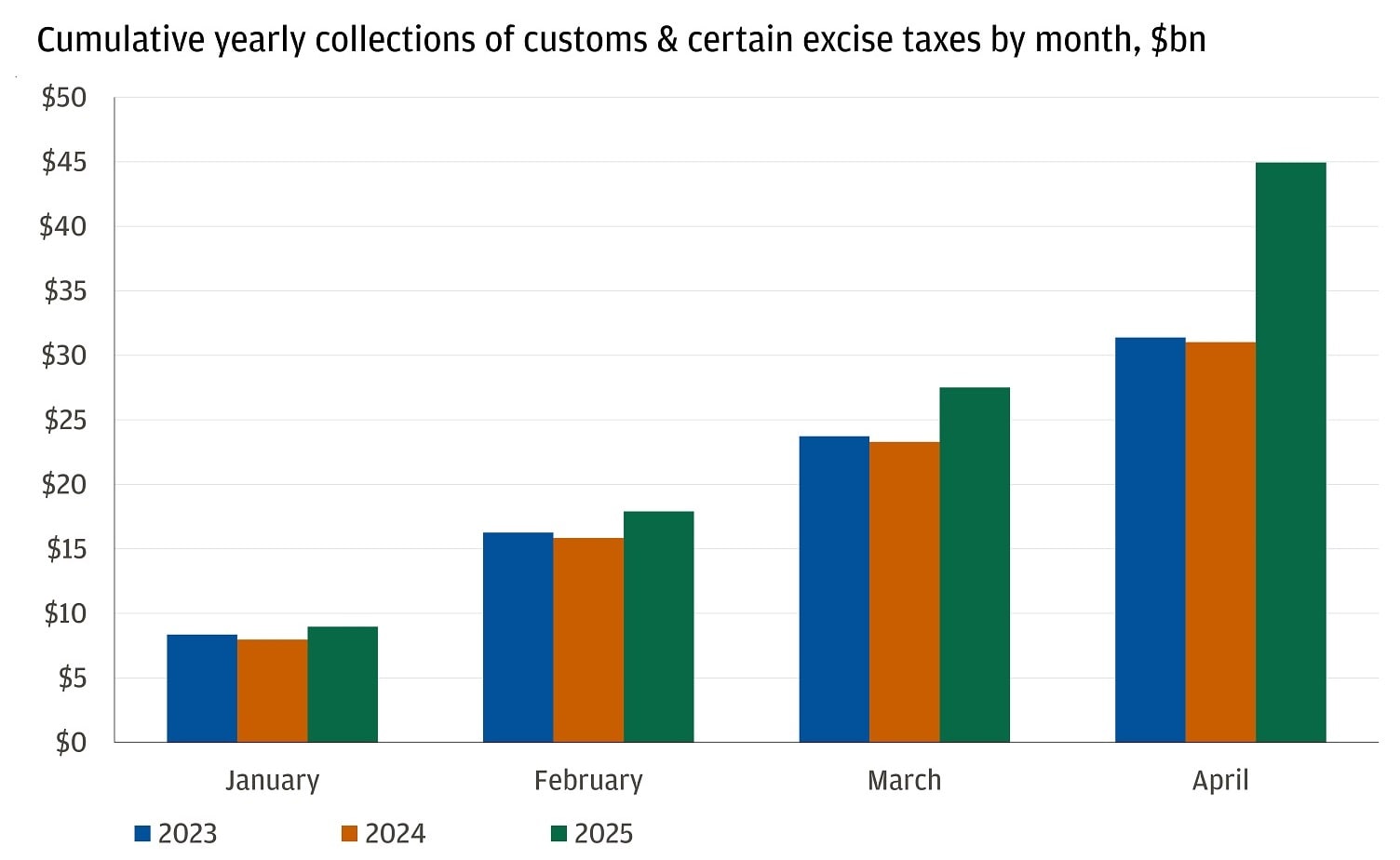

In the trade data: Trade uncertainty has dominated market dynamics this year as the estimated effective tariff rate in the U.S. has risen to the highest level in 100 years. This has led businesses to take preemptive measures by increasing their imports of inputs in the first quarter of this year to get ahead of tariffs. U.S. ship imports climbed throughout Q1 2025 and as a result, Treasury collections of customs and certain excise taxes in April increased over 60% relative to March this year.

Customs duty collections jumped in April

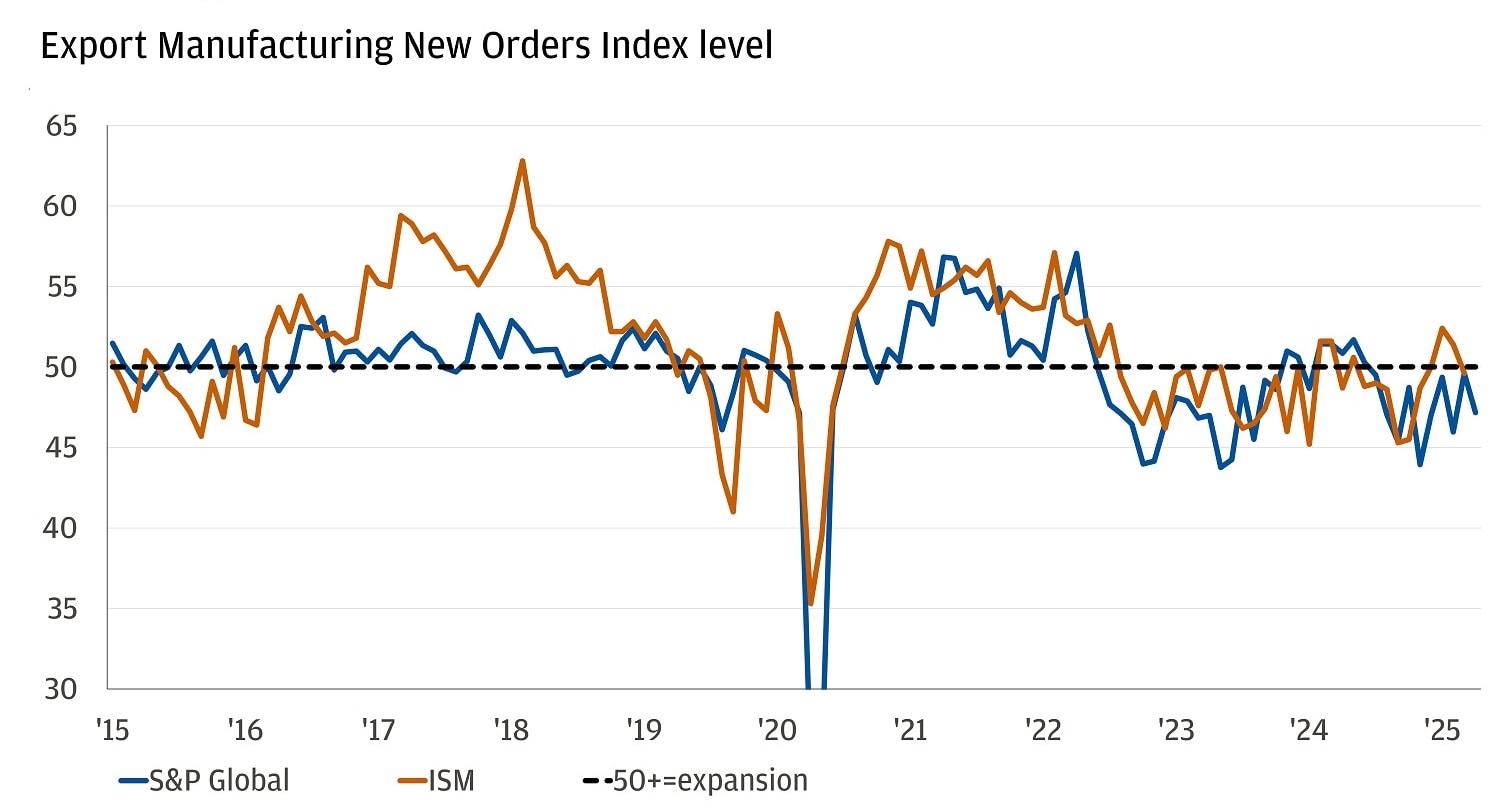

The fear for markets now is that global trade and demand for goods will fall amid heightened tariffs. But that’s not what we are seeing in the hard data, yet. Global export orders still remain around their 10-year average but are expected to decline if tariff rates remain high.

Global demand for exports remains relatively steady

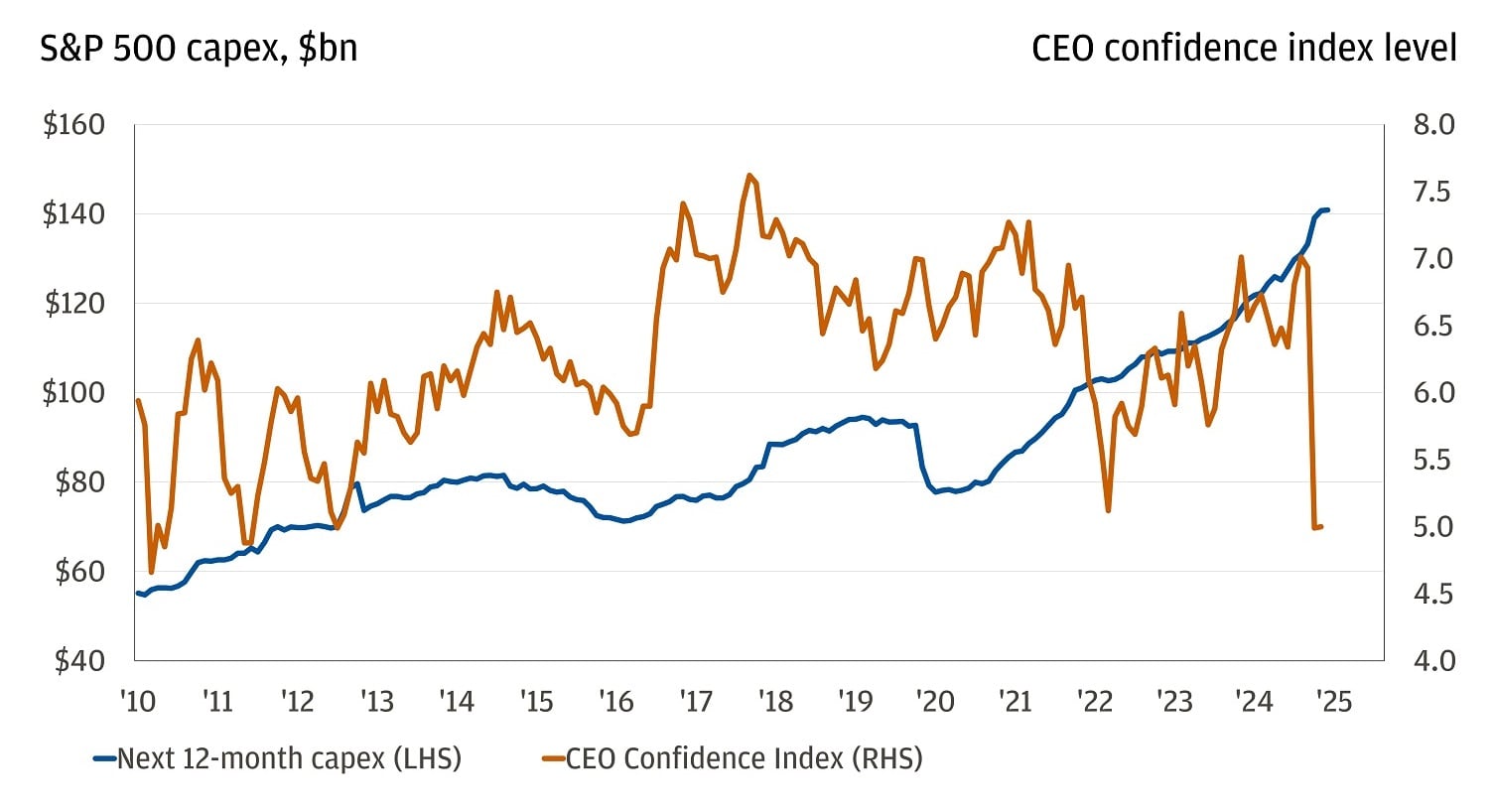

From corporate CEOs: Sentiment isn’t just downtrodden amongst Main Street, but also CEOs. A survey which measures CEO expectations for the overall business conditions one year from now has dropped to its lowest level since 2011. You might expect a collapse in CEO confidence to impact corporate spending plans (for hiring, investment or expansion). However, that’s not what we’re seeing in the data. Instead, capital expenditure expectations for the S&P 500 have increased every month since September.

Capex continues to increase despite muddied confidence

Several market areas are still awaiting confirmation of whether weak soft data will lead to declines in hard data. But portfolios don’t need to be in a state of limbo. We believe there are several timely actions you can take now to position ahead of changes in the hard data, namely, rightsizing positions to align with strategic asset allocations.

As U.S. equities have outperformed the rest of the world by an order of magnitude of 2x since 2010, investor portfolios have become massively overweight to U.S. assets. Whether that was due to a lack of rebalancing or intentionally to capture superior growth of U.S. tech corporations, it was the right call to make. But we see the tides changing and believe that now is a good time to add international diversification to those portfolios that have been underweight. This year’s U.S. underperformance versus the rest of the developed world serves as a reminder to hold diversified risk exposures.

Moreover, we view the U.S. dollar as structurally overvalued due to substantial historical foreign investment inflows and a shift in investor confidence amid diminishing U.S. economic advantages and increased political risks.

To mitigate risks from a potentially overvalued dollar, consider diversifying investments into international markets such as Europe and Japan leaving dollars unhedged. Diversification, by definition, means that you won’t have the highest return in a given year but it creates a smoother ride for investor portfolios. Using MSCI World as a benchmark, we believe about 30% of your equity allocation should be in non-U.S., with two-thirds of that in Europe. This can help reduce currency risk and further diversify sources of return in your portfolio.

For more on how you can best position your portfolio, your J.P. Morgan advisor is here to help.

All market and economic data as of 05/09/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

Explore ways to invest

Take control of your finances with $0 commission online trades, intuitive investing tools and a range of advisor services.

J.P. Morgan Wealth Management