The bull side, the bear side and the reality

J.P. Morgan Wealth Management

Market Update

U.S. equity markets are heading towards their first weekly gain in four weeks.

The Federal Reserve (Fed) left rates unchanged, decreased growth forecasts and increased near-term inflation expectations, but signaled that their base case for tariff inflation is that it will be – gasp – transitory. Futures markets are now pricing two interest rate cuts this year and about a 50% chance of a third. That sparked a bid in Treasury markets. The 2-year (3.95%) dropped 7 basis points (bps), and the 10-year (4.23%) is lower by 9bps.

In Europe, stocks continued their outperformance. This week, Germany approved legislation allowing defense spending in excess of 1% of GDP to be exempt from borrowing restrictions. That will unlock hundreds of billions in fiscal spend for the country, which could permeate throughout the Eurozone. The Stoxx 50 is up +0.2% this week and +11% this year.

In commodities, investors continued to flock to safe-haven gold (+1.6%). The precious metal is heading towards its 11th week of positive returns in the last 12, its best streak in over a decade.

With markets looking for clues as to which way the next leg of the trade will go, below we assess the bull and bear cases.

Assessing the bull and bear case

This week marks the five-year anniversary of the approximately 35% drawdown of the S&P 500 during the COVID-19 pandemic. As the world was going into lockdown, investors believed that the risks to the outlook were clearly skewed to the downside. Today, the S&P 500 is hovering near correction territory (-10% from highs), and risks to the bull and bear cases seem more evenly distributed.

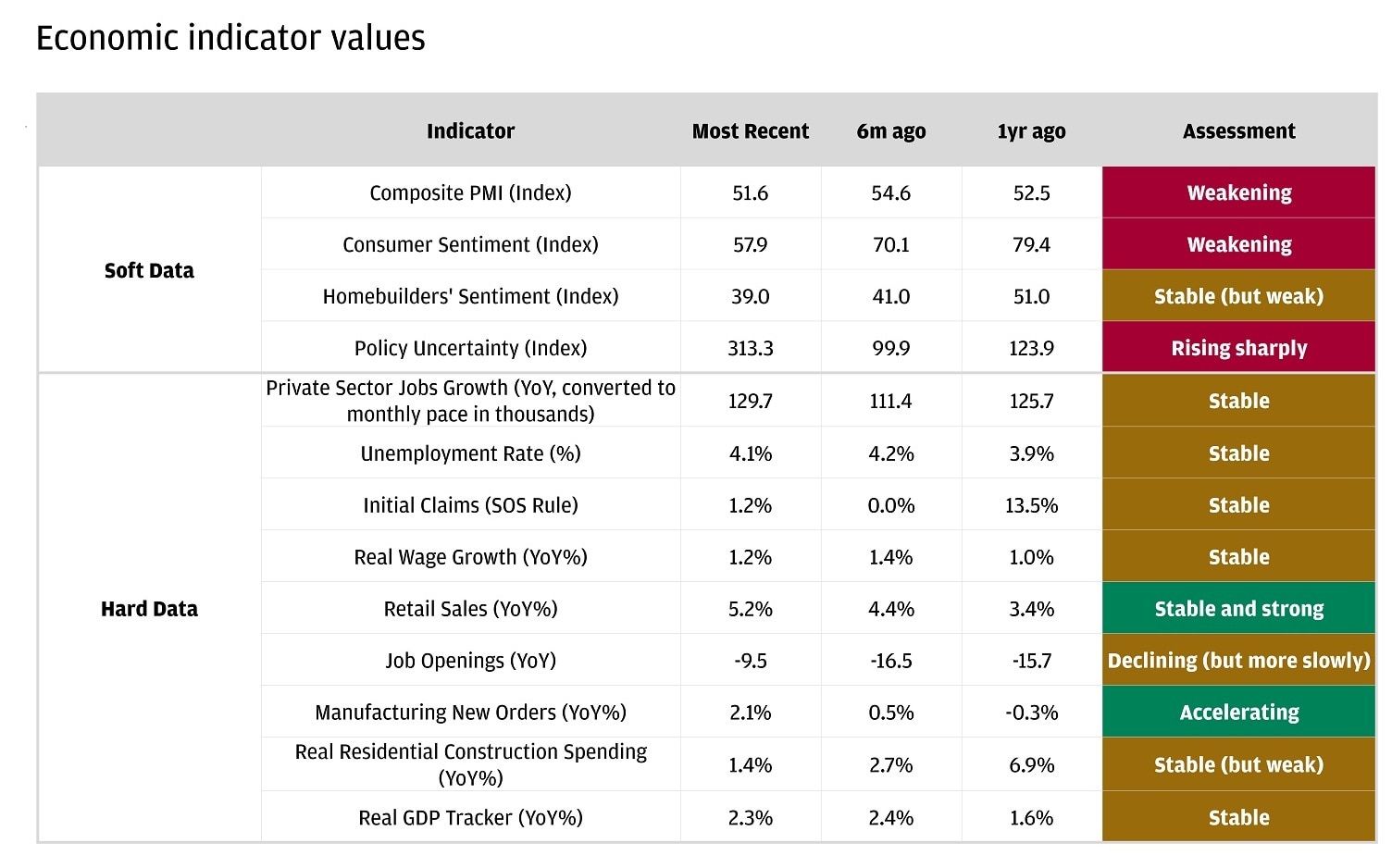

The bears have been taking a victory lap to start the year. The S&P 500 is off to its third-worst start to a year in the last 15. Softer economic data (purchasing manager surveys, consumer sentiment and homebuilders’ sentiment) has emerged, and consumer inflation expectations have risen. The bears would argue that tariff escalation on April 2 will exacerbate both. The tax on goods will be stagflationary, further driving up inflation while continuing to weigh on growth. That could leave the Fed in a difficult situation to manage their dual mandate of stable prices and maximum employment.

The bulls would argue that it’s not about how you start the year, it's how you finish. They would concede that the economic data referred to above has been weak. But those figures represent “soft” data (perceptions, opinions and expectations for economic conditions), not the “hard” data (realized economic activity, like employment figures and retail sales). The bulls would point to the fact that the actual realized economic activity has held up quite well.

“Hard data” is still holding up

Work with an advisor

Our advisors can provide ongoing financial advice on how your portfolio can adapt to the changes in the market, your life and your goals.

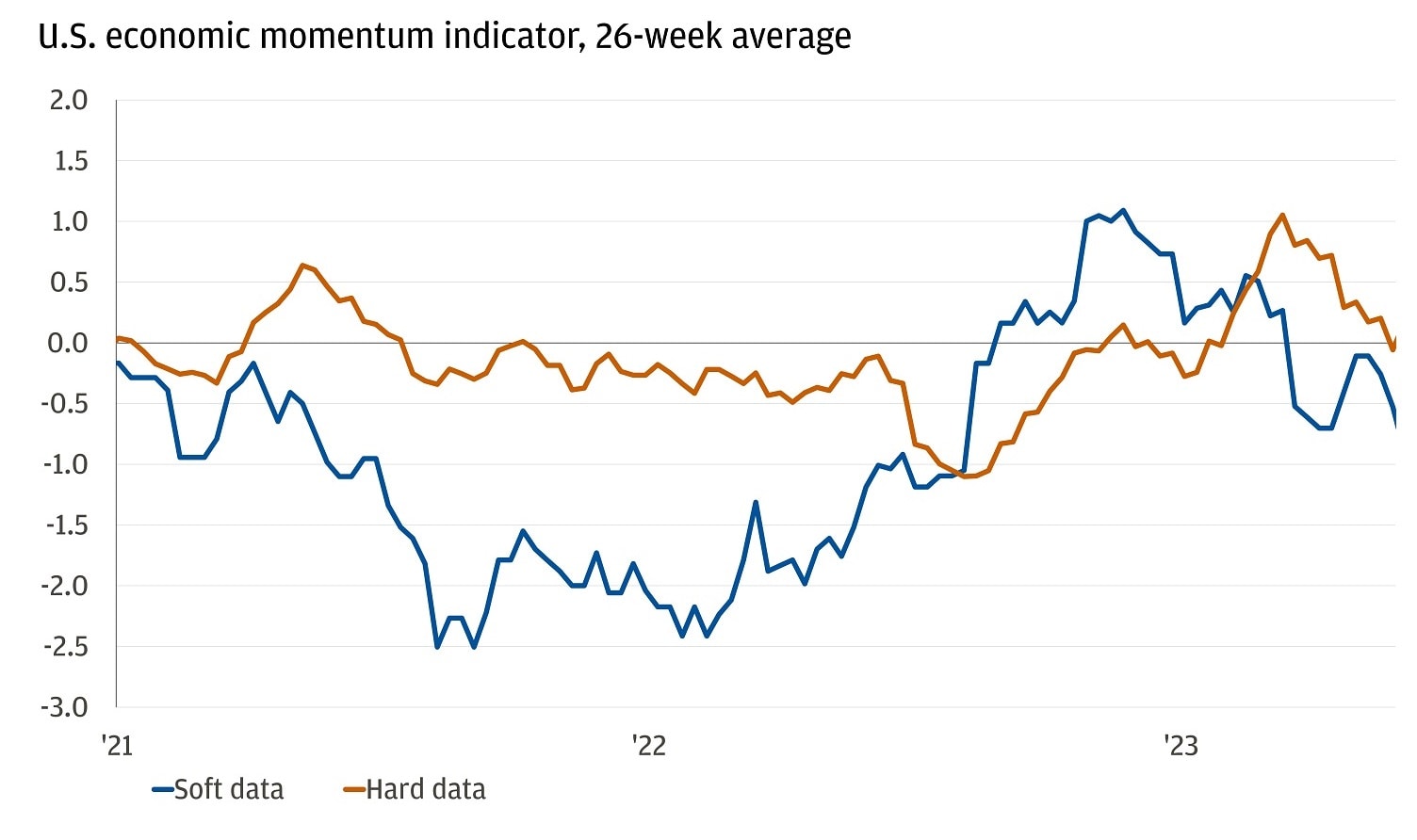

What’s more, the bulls would say that recent history suggests soft data has not been a good predictor of hard data, as Fed Chairman Jerome Powell mentioned this week. From 2021 to 2023, an index of soft data showed a decline and reversal of five orders of magnitude while hard data stayed about flat over the period.

Soft data isn’t always an indicator for hard data

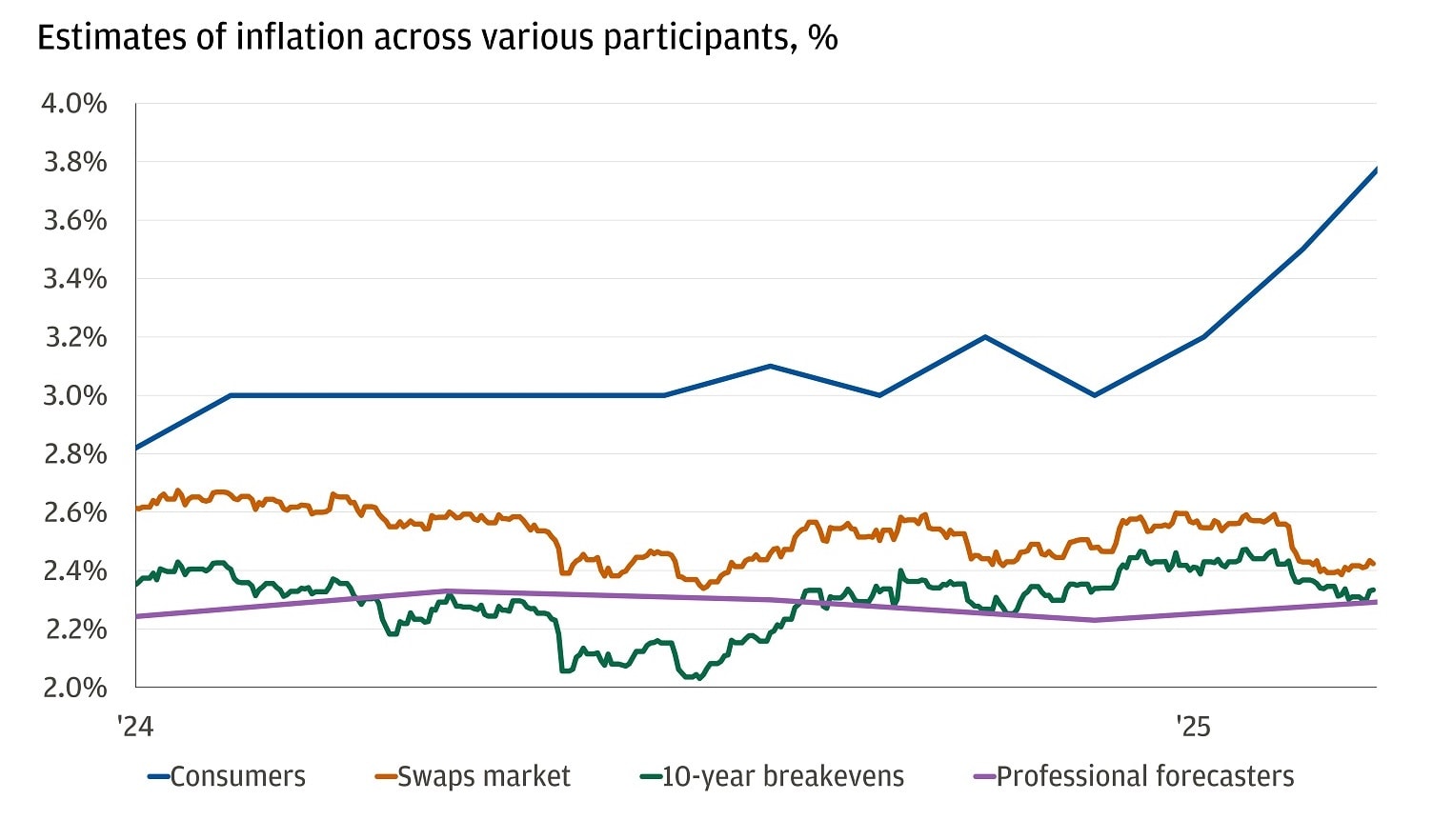

On inflation, the bulls would argue that the University of Michigan consumer expectations of an inflation increase is one data point. Other measures of inflation expectations haven’t seen an increase of the same magnitude, and in some instances, have actually shown a decline. Most importantly for the Fed and markets is that long-run inflation expectations remain anchored near the Fed’s 2% target to mitigate chances of a wage spiral.

Consumers have higher expectations for inflation

Every story has three sides: the bull case, the bear case and reality. We believe reality lies somewhere in the middle.

At the start of the year, market consensus was pricing in minimal risk. Over the last three months, risks have increased, and prices have adjusted to reflect them. In our opinion, that represents a healthy correction and acknowledgment of the distribution of outcomes.

We sympathize with the bears: Risks still exist to our outlook. The tariff overhang could cause a wait-and-see approach towards capital allocation and slower growth. Increased goods inflation could persist if supply chains are in fact reshored. To manage those risks, we think it’s prudent for investors to add resilience to portfolios through assets like gold (which can provide a hedge against uncertainty) and infrastructure assets (which can provide income and diversification from both stocks and bonds).

We think the bulls are right about inflation. Inflation expectations still remain anchored, and hard data has held up despite a shift in sentiment. In fact, poor sentiment may even present an opportunity. Going back to 1971, investing in the S&P 500 during the nine consumer sentiment troughs led to an average +24% return in the next 12 months. We think that investing in U.S. equities from here can still provide attractive returns into year-end.

We would not let the bulls nor the bears derail our investment plans. Remember everything that markets have experienced since the COVID-19 drawdown five years ago: inflation reaching the highest level since the 1980s, global central bank rate hikes, the Russian invasion of Ukraine, bank failures and two changes in the U.S. Presidential administration. The S&P 500 increased more than +150%.

Our advice when risks exist on either side of the outlook is to stick to a strategic asset allocation, use equities for long-term capital appreciation, fixed income to hedge during growth slowdowns and make tactical adjustments at the margins to take advantage of opportunities that arise.

For help finding your strategic asset allocation, reach out to your J.P. Morgan advisor.

All market and economic data as of 03/21/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

Explore ways to invest

Take control of your finances with $0 commission online trades, intuitive investing tools and a range of advisor services.

J.P. Morgan Wealth Management