Navigating Washington's risks: Mar-a-Lago accord, tariffs and municipal tax exemption

Head of Global FX Strategy,

J.P. Morgan Private Bank

Market update

U.S. consumers are not convinced about the prudence of the White House’s strategy. Consumer confidence fell to the lowest level in four years in March, largely due to concerns about higher prices and the economic outlook amid escalating trade policy uncertainty. Their expectations for the future also darkened. The expectations component of the index fell to the lowest level in 12 years. Equity investors looking for a silver lining should know that spikes in policy uncertainty and troughs in consumer sentiment counterintuitively augur stronger forward returns ahead. Sometimes, it really is the darkest before the dawn.

Economic data this week also signaled some reprieve. The Citi U.S. Economic Surprise Index (which measures how economic data is coming in relative to economist expectations) has increased from -16.5 in February to -4.6 now. Indeed, it seems like “hard” measures of economic data are holding up much better than the “soft” data derived from people’s perceptions.

Until we hit first-quarter earnings season (J.P. Morgan announces in just two weeks), Washington will likely continue to dominate the debate. We are focused on three risks: tariffs, municipal bond tax status and the Mar-a-Lago accord.

Three risks emanating from Washington

Trade uncertainty has reached the highest level on record, advisors to the administration have reignited a 15-year-old debate on municipal bond tax exemption and the White House could be looking for ways to weaken the dollar.

Here is our take on those three risks, listed in order of our assessment of most to least likely and impactful.

1. What’s at stake with tariffs? April 2, ”Liberation Day,” is now less than one week away.

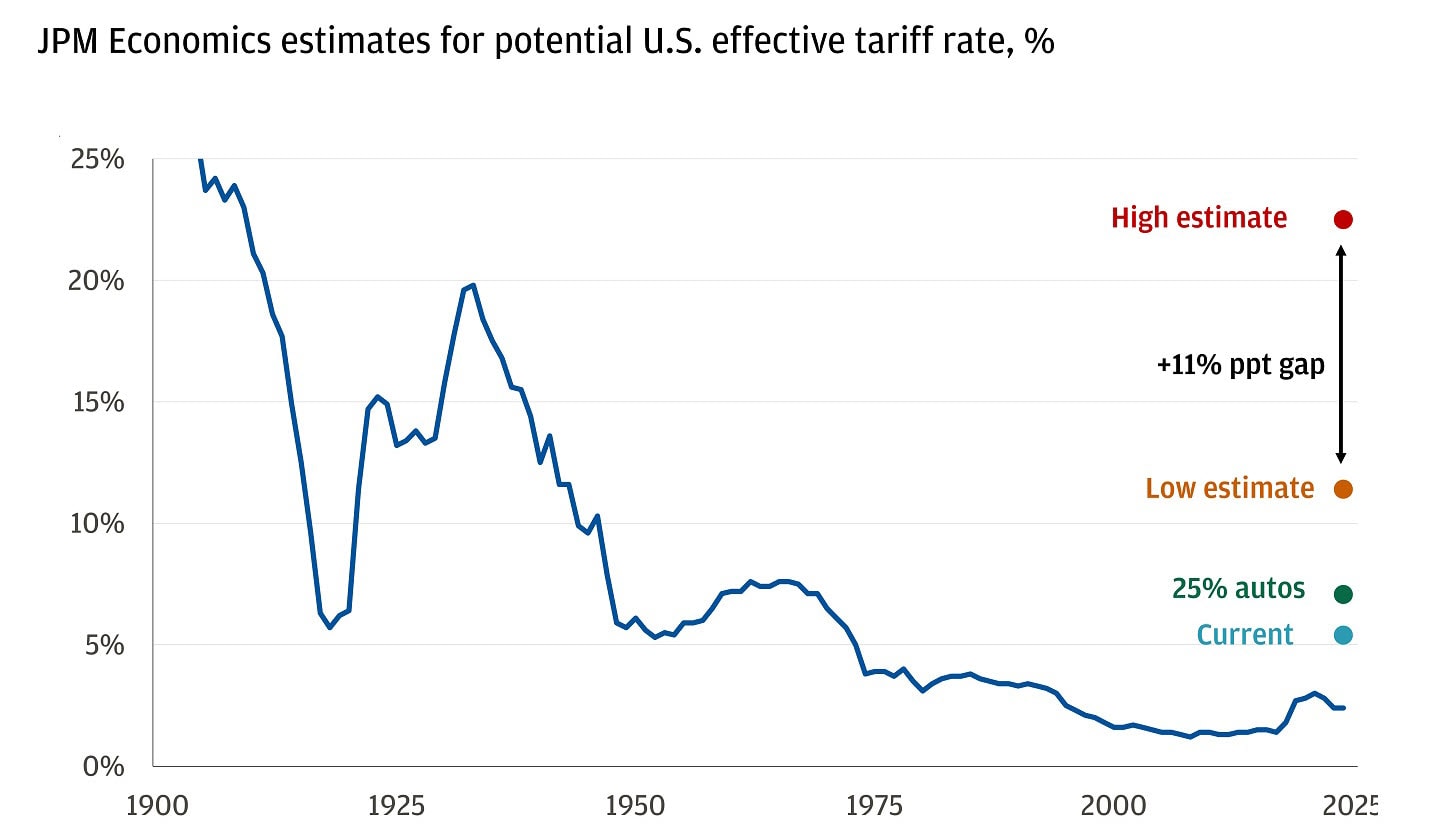

What’s at stake? The market agrees that tariff rates are heading higher, but there is tremendous uncertainty over just how high they will go. At over 10 percentage points, the range of estimates on where the U.S. effective tariff rate will land is wider than the overall tariff rate itself has ever been in post-war America.

Wide range of tariff estimates

There is a wide range of goals the administration appears to be trying to solve with tougher trade policies: remedying trade deficits, raising government revenue, ensuring reciprocity/fairness for U.S. business interests abroad, safeguarding national security-related supply chains and securing the border from immigrants and drugs. Crafting a single tariff strategy that encompasses all of these goals in such a short time will be challenging. During the 2018 trade war, it took officials 326 days to investigate and enact tariffs on Chinese imports.

Work with an advisor

Our advisors can provide ongoing financial advice on how your portfolio can adapt to the changes in the market, your life and your goals.

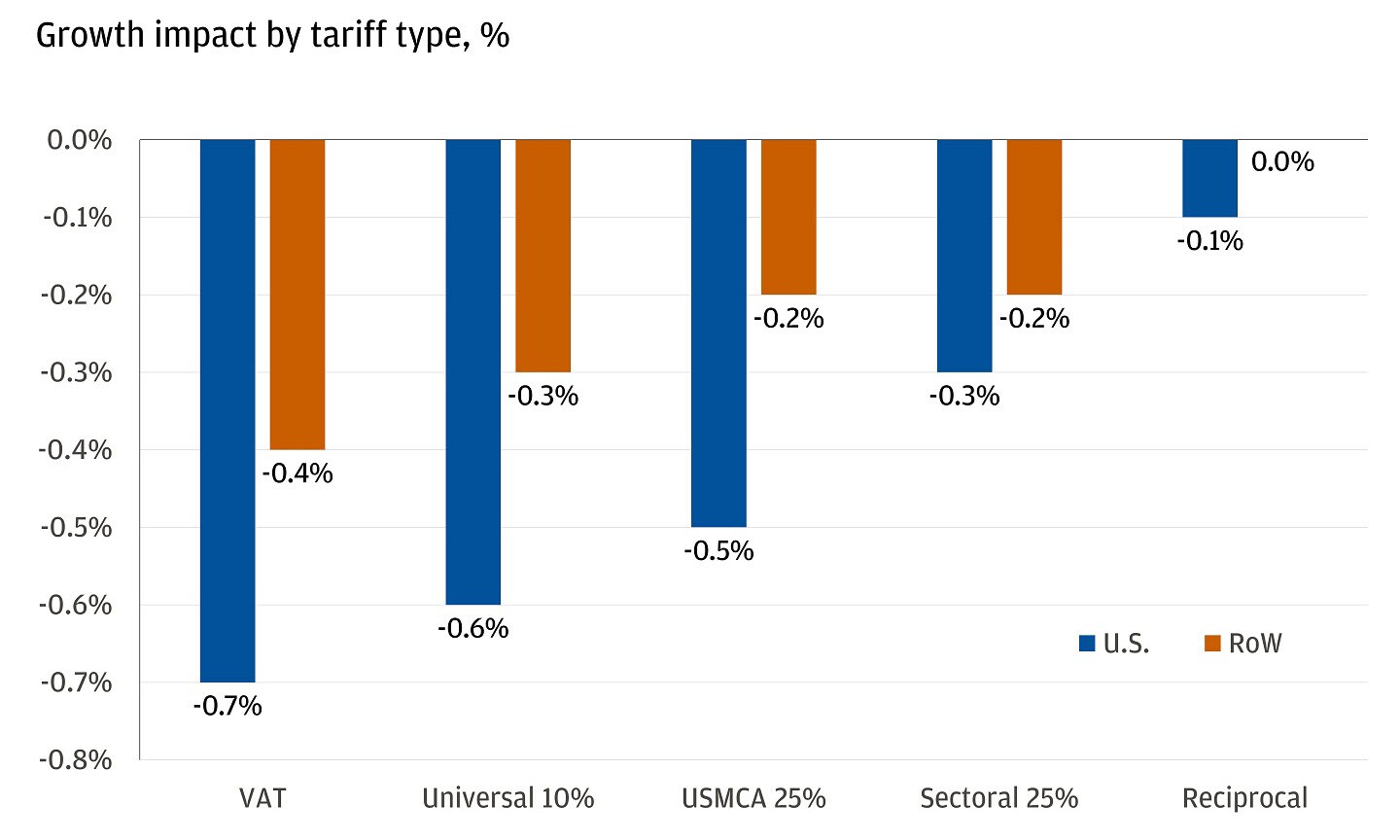

What is the effect on the U.S. economy? The higher tariff rates go, the larger the hit to growth is likely to be. The estimated impact on economic growth from the range of tariffs under consideration is between 0% to -0.7%. Notably, however, the potential hit to U.S. gross domestic product (GDP) could be larger than for the rest of the world, which is a stark contrast to the estimated impact of tighter trade policy coming into the year. After that, most forecasts were for higher tariff rates but primarily on China and a narrow set of national-security-related sectors. As the U.S. instigates trade wars with the rest of the world, they lose the advantage of size.

Negative growth impact varies by tariff type

This week President Trump offered a teaser to April 2 by signing a proclamation to implement a 25% tariff on all auto imports, set to come into effect on April 3 and expand to auto parts by May 3. The 25% tariff rate on vehicles covered by the US-Mexico-Canada trade agreement will only apply to the value of non-U.S. components.

There is little consensus over what the U.S. tariff regime may look like, raising the likelihood of market volatility and downside risks to U.S. and global growth. However, any sort of clarity on tariff policy may allow the market to move on to other risks.

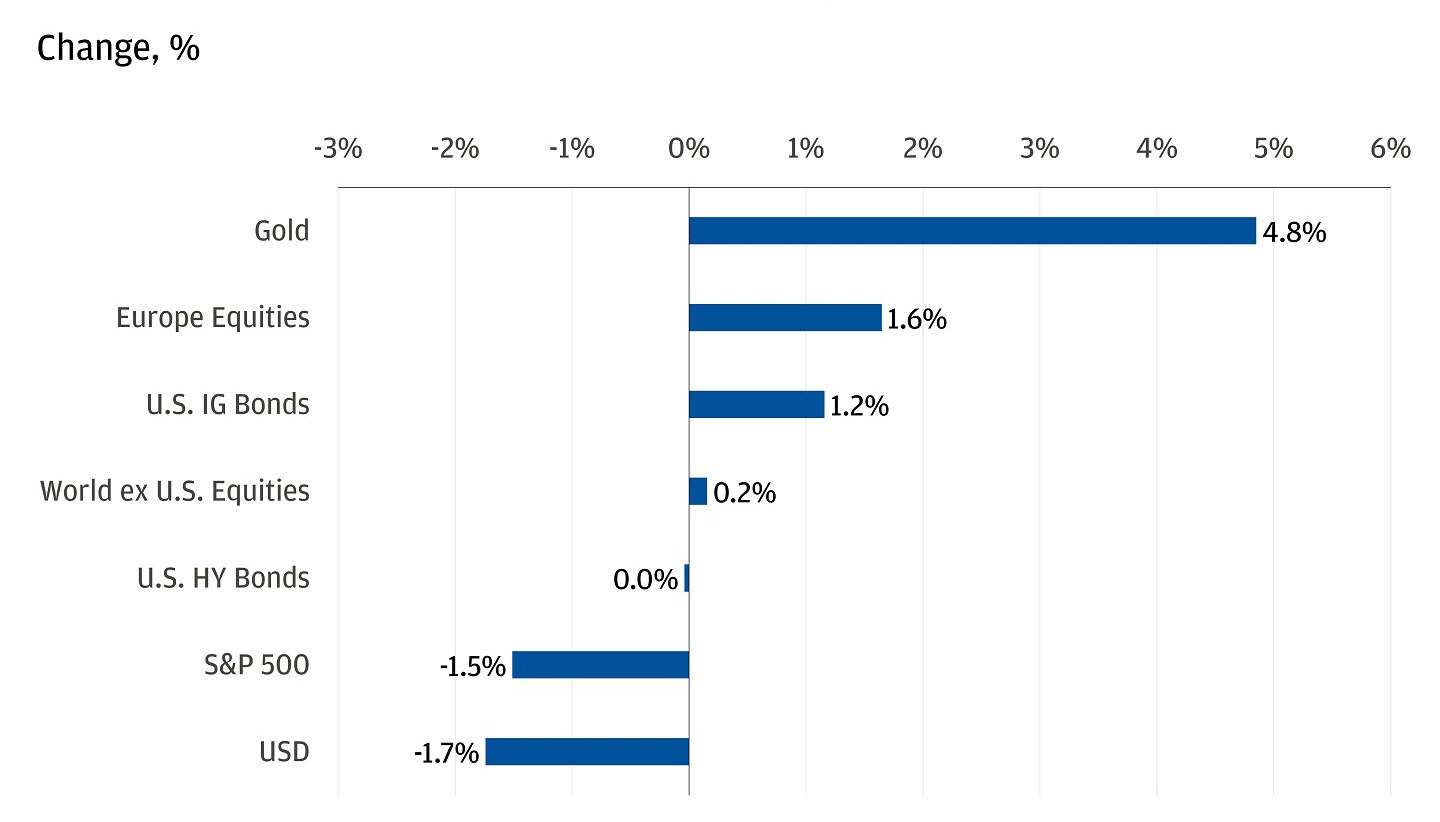

A key observation for investors is that gold has outperformed the USD and S&P 500 by >6% across the 11 days dominated by tariff announcements this year. We continue to think gold has a valuable role to play in portfolios, alongside diversification across asset classes and geographies.

Cumulative cross-asset pricing on tariff event days

2. Will municipal bond interest lose its tax-exempt status? Outside of trade, taxes are garnering market attention this week. The federal government forgoes approximately $30 billion annually by not taxing municipal bond interest. Stephen Moore, an informal Trump economic adviser, suggested modifying the tax exemption of municipal bond interest income to raise revenues.

We continue to think an elimination of the municipal bond tax exemption is unlikely, but some kind of modification to the tax exemption is possible.

The decision to tax municipal bond interest has been debated by Congress many times over the last 15 years. So far, the tweaks have been marginal. In 2017, the Tax Cut & Jobs Act (TCJA) eliminated the ability for municipalities to issue tax-exempt advance refunding bonds on a tax-free basis. Prior to the TCJA, municipalities could issue bonds to refinance existing debt at lower interest rates before the call date of the original bonds, allowing them to take advantage of favorable market conditions. The interest on these advance refunding bonds was exempt from federal income tax, which made them an attractive option for municipalities looking to reduce their borrowing costs. This provision was estimated to save $17 billion over ten years or $1.7 billion per year – a small amount.

We see four potential scenarios regarding taxation of the municipal market:

- Municipal market remains tax-exempt: Probability - High

- Municipal sector modification (e.g., higher education, health care or private activity bonds become taxable): Probability - Moderate

- Municipal Bond Tax-Exemption Cap initiated: Probability - Moderate

- Municipal market becomes taxable: Probability - Low

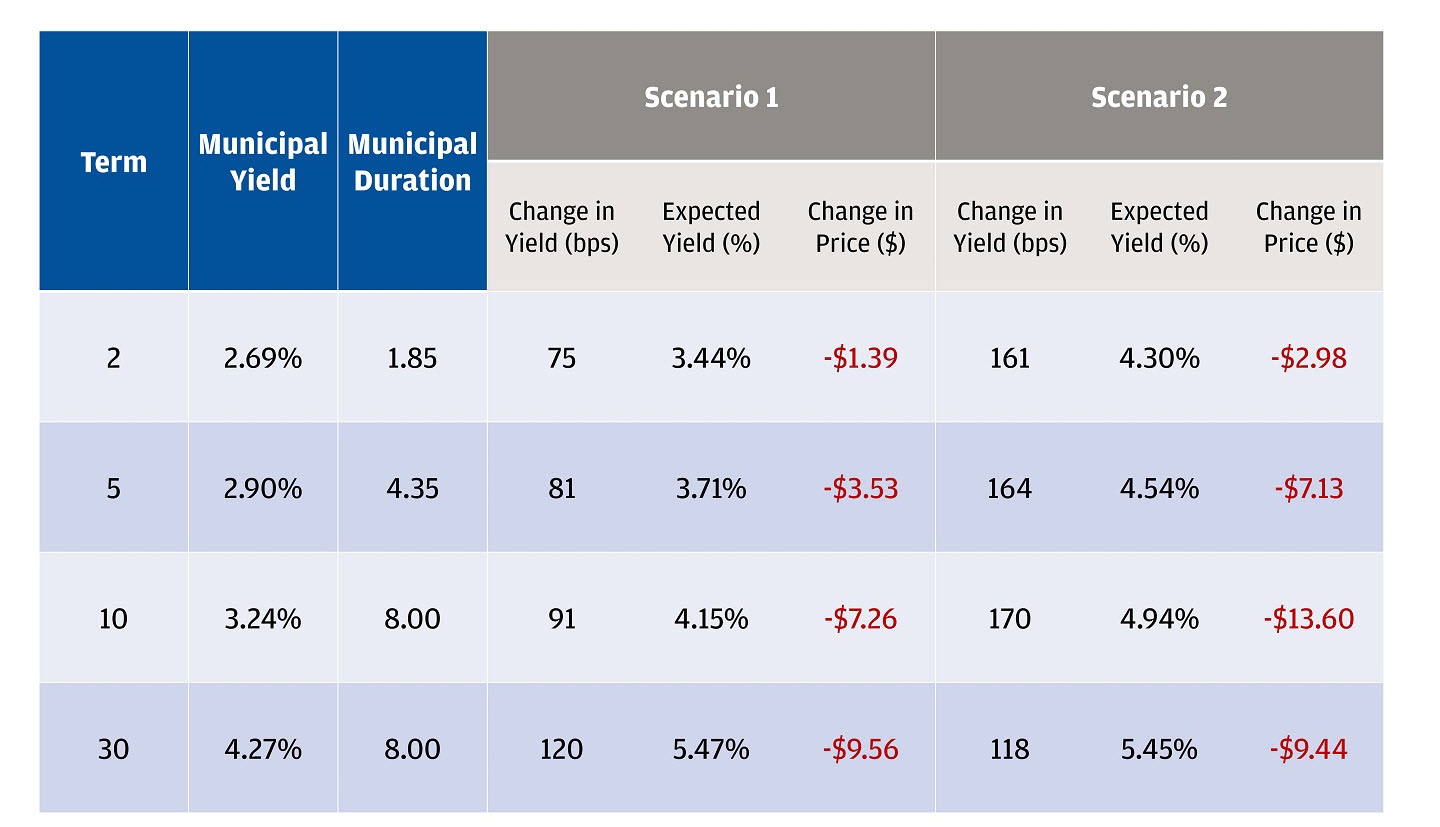

What if municipal bonds become taxable? Below we outline two potential scenarios that cover if municipal bonds are taxed. Keep in mind these cover the worst-case scenarios, are not our base case and result in just an approximate 10% maximum decline in price if not held to maturity.

Scenario 1: The first scenario illustrates taxing municipal bond interest at 28%, the rate that Stephen Moore and the 2011 American Jobs Act proposed. We estimate that a 28% tax on municipal bond income would cause an upward adjustment in interest rates by approximately 75–120 basis points (bps). This would cause a bond price erosion of approximately $1.40–$9.60.

Scenario 2: The second scenario depicts tax-exempt rates rising to levels consistent with the AA/Aa rated corporate bond market. In this case, tax-exempt rates could widen by 118–170bps. If this were to occur, once the market normalizes, bondholders would generically see price erosion of approximately $3.00–$13.60.

Municipal bond taxation scenarios

Both of these scenarios represent tail risks, and the bottom line for us is that the municipal market is likely to remain tax-exempt. Even if there were changes, it is more likely that they would happen on the periphery of the market, and that existing positions would be grandfathered into tax-exempt status. We are watching Washington closely for any signs that Congress is seriously considering changes.

3. What is the Mar-a-Lago accord and could it happen? A paper by Stephen Miran, Chair of the White House Council of Economic Advisers, has raised some radical ideas as to how the administration could weaken the dollar.

The U.S. dollar is 6% above its 10-year average and 16% above its 20-year average valuation when measured against a basket of other major world currencies. A stronger dollar tends to lead to more imports (international goods are relatively cheaper for U.S. consumers) and fewer exports (U.S. goods are relatively more expensive for international buyers), which directly opposes the administrations goals of balancing trade and revitalizing domestic manufacturing. The administration has a stated goal to increase manufacturing domestically.

Miran’s paper focuses on two ideas:

- A “Mar-a-Lago Accord” where countries/central bank reserve managers agree to swap their holdings of short-term U.S. Treasury securities for century (i.e., 100 year) bonds. If countries don’t agree to this, they would be subject to tariffs and have U.S. security guarantees removed.

- The U.S. could charge a “user fee” on reserve assets held by other countries – for example, a fee of 1% of coupons, which might increase to 2% if USD devaluation is insufficient. The paper also suggests differentiating between friends and foes: “Presumably, the Administration would want to withhold remittances to geopolitical adversaries like China more severely than to allies or to countries that engage in currency manipulation more severely than to those that do not.”

The persistent overvaluation of the USD poses a challenge, but the “Mar-a-Lago Accord” and user fees on reserve assets carry substantial risks. Most notably, these measures could undermine the dollar’s reserve status and lead to much higher long-term interest rates, which are also contrary to the administration’s goals. Further, it seems unlikely that other economic policymakers would agree readily to a scheme to weaken the dollar like they did in the 1980s. Our view is that the accord is very unlikely.

We’ve highlighted several risks which are growing out of Washington. Investors should think about how they can position portfolios to help protect from those risks. We believe investors should stick to their strategic asset allocations, using equity exposure for long-term capital appreciation and fixed income to hedge from growth scares. Additionally, we think tactically adding resilience (defined as income, diversification and inflation protection) to portfolios through gold and real assets like infrastructure can help insulate portfolios from existing risks. Limiting the severity of drawdowns is critical to long-term investment success.

For questions as to how to best position your portfolio, reach out to your J.P. Morgan advisor.

All market and economic data as of 03/28/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

Explore ways to invest

Take control of your finances with $0 commission online trades, intuitive investing tools and a range of advisor services.

Head of Global FX Strategy,

J.P. Morgan Private Bank