Is deal activity on the rise? 2 signs we see now

Global Investment Strategist

Market update

Markets maintained a tenuous holding pattern this week as investors monitor the escalating conflict between Iran and Israel. Oil (+3.6%) prices topped $78 per barrel for the first time since January amid fears of war escalation in the Middle East, with ongoing concerns about flows from Iran and threats to vessel traffic in the Strait of Hormuz. While markets are on edge, it seems like crude prices have some more room to rise before they start to cause real friction for the U.S. economy.

The June Federal Open Market Committee meeting met expectations. The Federal Reserve left rates unchanged and kept messaging consistent: Tariff-driven economic uncertainty and inflation risks complicate its efforts to ease monetary policy. They still expect that all else equal, they will lower interest rates by 50 basis points this year. Treasury yields are relatively unchanged, with no tenor moving more than 2 basis points.

U.S. equities are flat headed into Friday trading following yesterday’s holiday. The tech-heavy Nasdaq 100 (+0.4%) eked out a gain alongside small caps (Solactive 2000 +0.4%).

While most eyes are watching to see how far the conflict in the Middle East might escalate and whether the White House will decide to intervene directly, we have been seeing some signs that the recovery in dealmaking and capital market activity may be gaining speed.

Work with an advisor

Our advisors can provide ongoing financial advice on how your portfolio can adapt to the changes in the market, your life and your goals.

Spotlight

Coming into this year, we were expecting a meaningful resurgence in dealmaking activity fueled by the Trump administration’s pro-business, deregulatory agenda. And there were green shoots to start the year: global mergers and acquisitions (M&A) activity was up 17% year-over-year in Q1 2025. But tariff-induced uncertainty curtailed any momentum. However, we are now starting to see three distinct drivers that could accelerate the recovery:

1. Artificial intelligence

Artificial intelligence (AI) is rapidly becoming a catalyst for transformative change in the M&A and initial public offering (IPO) landscapes. Generative AI is reshaping the M&A process, with about one in five companies currently utilizing AI and expectations that more than half will integrate it by 2027, according to Bain. AI’s ability to improve various stages of dealmaking – from sourcing and screening to diligence and integration – is raising the standard for competitors. Those leveraging AI are gaining a competitive edge, making it essential for others to adopt these technologies or risk falling behind in the fast-paced environment.

The broader tech ecosystem is also focused on AI acquisitions to gain and maintain a strategic advantage. Meta’s $14.8 billion Scale AI deal is just the latest testament to the rise of AI tie-ups. Meta finalized a multibillion-dollar investment in Scale AI and recruited the startup’s CEO to join its AI efforts.

OpenAI is acquiring io, a startup co-founded by Apple veteran Jony Ive, in a nearly $6.5 billion all-stock deal to develop AI-powered devices. This move highlights the transformative potential of AI in M&A, as tech companies increasingly acquire AI startups to enhance their offerings and leverage their experience.

CoreWeave, an AI cloud-computing startup, has experienced a remarkable post-IPO rally and is now up over 280% as a public company. It has gained significant traction due to its multi-billion-dollar contracts with Nvidia, OpenAI, Microsoft and other major companies propelling AI. CoreWeave expects capital expenditures of $20 billion to $23 billion this year to expand its AI infrastructure and data center capacity.

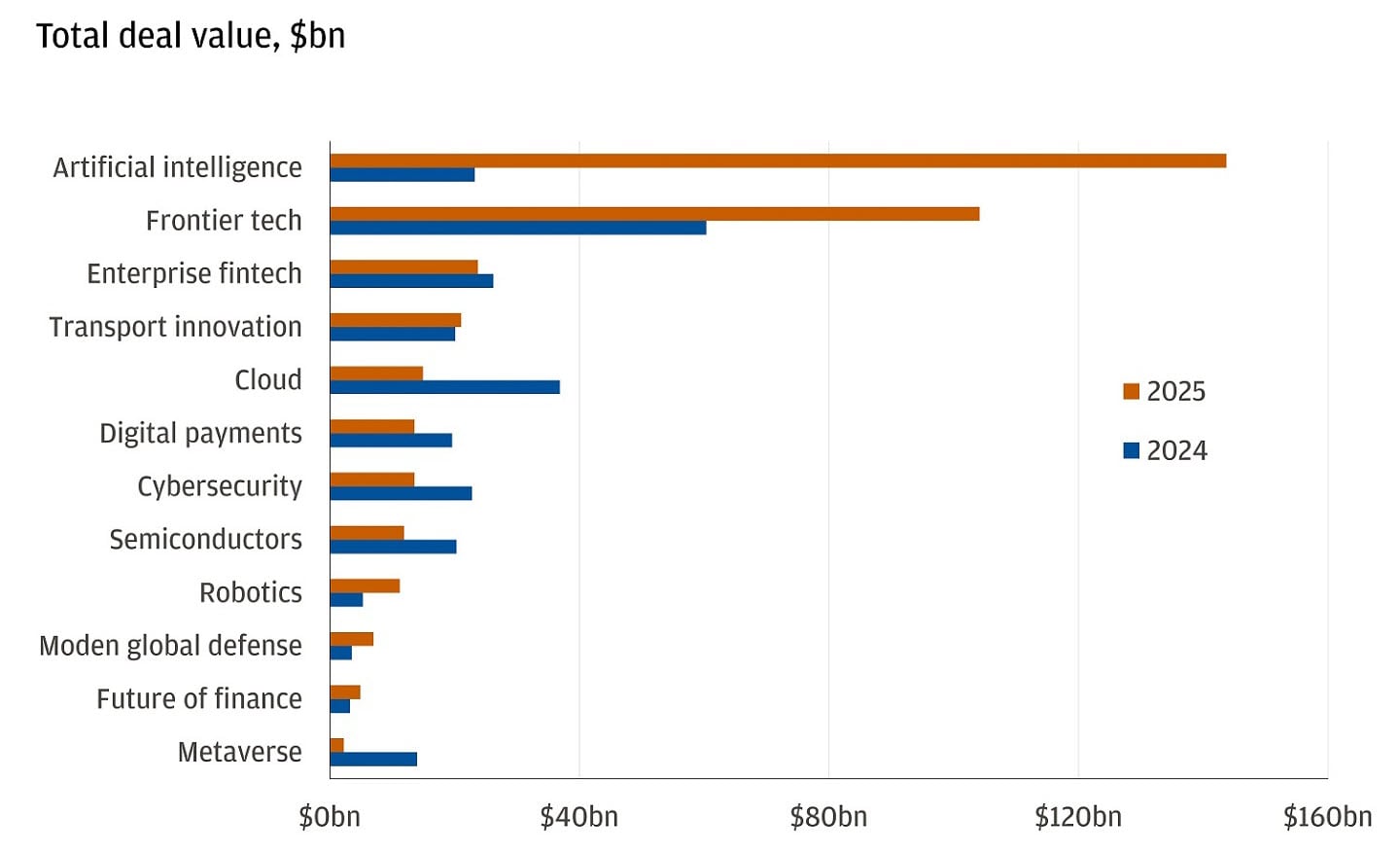

AI deal value so far this year exceeds $140 billion, crushing last year’s total of roughly $25 billion.

AI dealmaking has accelerated in 2025

We are confident that AI will continue to drive significant productivity gains for businesses, consumers and the economy. The integration of generative AI into M&A processes and the strategic urgency to stay at the leading edge of AI should propel dealmaking activity.

2. Financial sector deregulation

While tariffs have dominated headlines, a significant conversation around bank deregulation is unfolding, poised to spur M&A activity through increased lending. Following the Global Financial Crisis, regulations were tightened to strengthen bank balance sheets and prevent another collapse. However, these regulations have become increasingly stringent over time. In the wake of the March 2023 banking crisis and the proposed Basel III Endgame rules, U.S. banks have built up capital amid regulatory uncertainty. Now, with the new administration signaling a potential easing of these regulations, banks are expected to release some of this built-up capital.

Treasury Secretary Scott Bessent has emphasized the importance of bank deregulation to unlock non-government lending and stimulate private sector growth. Deregulation is seen as the next phase of the administration’s agenda. The latest move plans to reduce the enhanced supplementary leverage ratio (eSLR) by up to 1.5 percentage points. The rule requires large lenders to hold a certain amount of capital against their investments in Treasuries. With an easing of this rule, banks may have more flexibility to lend as they are required to hold less capital against their leverage exposure. As banks gain more balance sheet capacity, they are likely to use it for capital distributions to shareholders, M&A activity for themselves and lending growth for the broad economy.

The ongoing dialogue around bank deregulation presents a multifaceted opportunity for the U.S. banking sector. As regulatory requirements soften, banks are positioned to deploy significant excess capital, enhancing shareholder returns, loan growth and M&A activity. This deregulation could lead to improved profitability through increased capital markets activity and reduced regulatory expenses, with preferred stock and equities both likely to benefit.

The current dealmaking and capital market environment seems to be heating up. AI innovation and deregulation are promising catalysts for a continued revival. As AI continues to drive productivity gains and competitive advantages, deregulation unlocks lending potential and investors are well-positioned to capitalize on these potentially transformative trends.

Reach out to your J.P. Morgan advisor to discuss how these themes might impact your portfolio.

All market and economic data as of 06/20/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

Explore ways to invest

Take control of your finances with $0 commission online trades, intuitive investing tools and a range of advisor services.

Global Investment Strategist