All eyes on DC: 3 things investors should watch

J.P. Morgan Wealth Management

By: Alan Wynne and Rebecca Boeve

Market update

U.S. equities climbed higher this week as positive political news came in the form of U.S. President Donald Trump and Chinese President Xi Jinping’s first phone conversation of Trump’s presidency.

A lot of moving macro pieces this week as global economic concerns were highlighted by the Organization for Economic Co-operation and Development’s reduced growth forecasts, citing aggressive trade policies. Despite an unexpected rise in U.S. job openings boosting market sentiment, May’s ADP private payrolls and the Institute for Supply Management’s services fell short of expectations, indicating potential economic contraction. Furthermore, President Trump plans to increase steel and aluminum tariffs, while expressing optimism about a U.S.-India trade deal. Inflationary pressures persist, with the Federal Reserve’s (Fed) Beige Book noting slowed hiring and tariff-related price concerns, prompting markets to increase their call for rate cuts.

In all, the moves netted out as a positive. The S&P 500 (+0.5%), Nasdaq 100 (+1%) and European equities (+0.8%) are all heading towards their second week in a row of gains.

In fixed income, the Treasury curve flattened. At the short end, 2-year yields increased two basis points while the 30-year declined six basis points.

This week’s news gives us three things to monitor closely coming out of Washington. We cover them in detail below.

Work with an advisor

Our advisors can provide ongoing financial advice on how your portfolio can adapt to the changes in the market, your life and your goals.

Spotlight

1. The deficit. The Congressional Budget Office (CBO) analyzed the budgetary and economic effects of the “One Big Beautiful Bill” passed by the House.

The bottom line: The CBO estimates that over the next 10 years, the cost of the bill is estimated to be $2.4 trillion. While a large number, the estimate is less than a preliminary CBO estimate of $3.8 trillion. What’s more, a separate CBO analysis found that tariffs would cut the deficit by $2.8 trillion. In total, the two policies are estimated to shrink the primary deficit by roughly $400 billion over 10 years.

Important: This analysis is on the primary deficit and does not include interest cost. So even with the offsetting tariff revenue on the proposed budget costs, deficits after interest costs would continue to increase in all likelihood.

First, this analysis remains in flux given the executive orders imposing the tariffs (which provide a large part of the $2.8 trillion offset) remain in place pending consideration by the Federal Circuit Court of Appeals. Second, the bill still needs to be passed through the Senate and is subject to changes which would modify these estimates.

With those disclaimers out of the way, this is an improvement of the deficit estimate relative to the previous CBO estimate. But we don’t think this changes the trajectory of the U.S. fiscal position and would expect the budget deficit to continue increasing over time when considering interest costs. That means term premium and volatility are expected to persist, especially at the longer end of the curve. In fixed income, we prefer the belly of the curve and in, which is more highly correlated with moves from the Fed relative to the long end. For U.S. taxable investors, our preferred fixed income instrument remains municipal bonds. 10-year municipal bonds spread, or compensation above inflation expectations, is at one of the highest levels in a decade and a half. Additionally, the income is tax-advantaged.

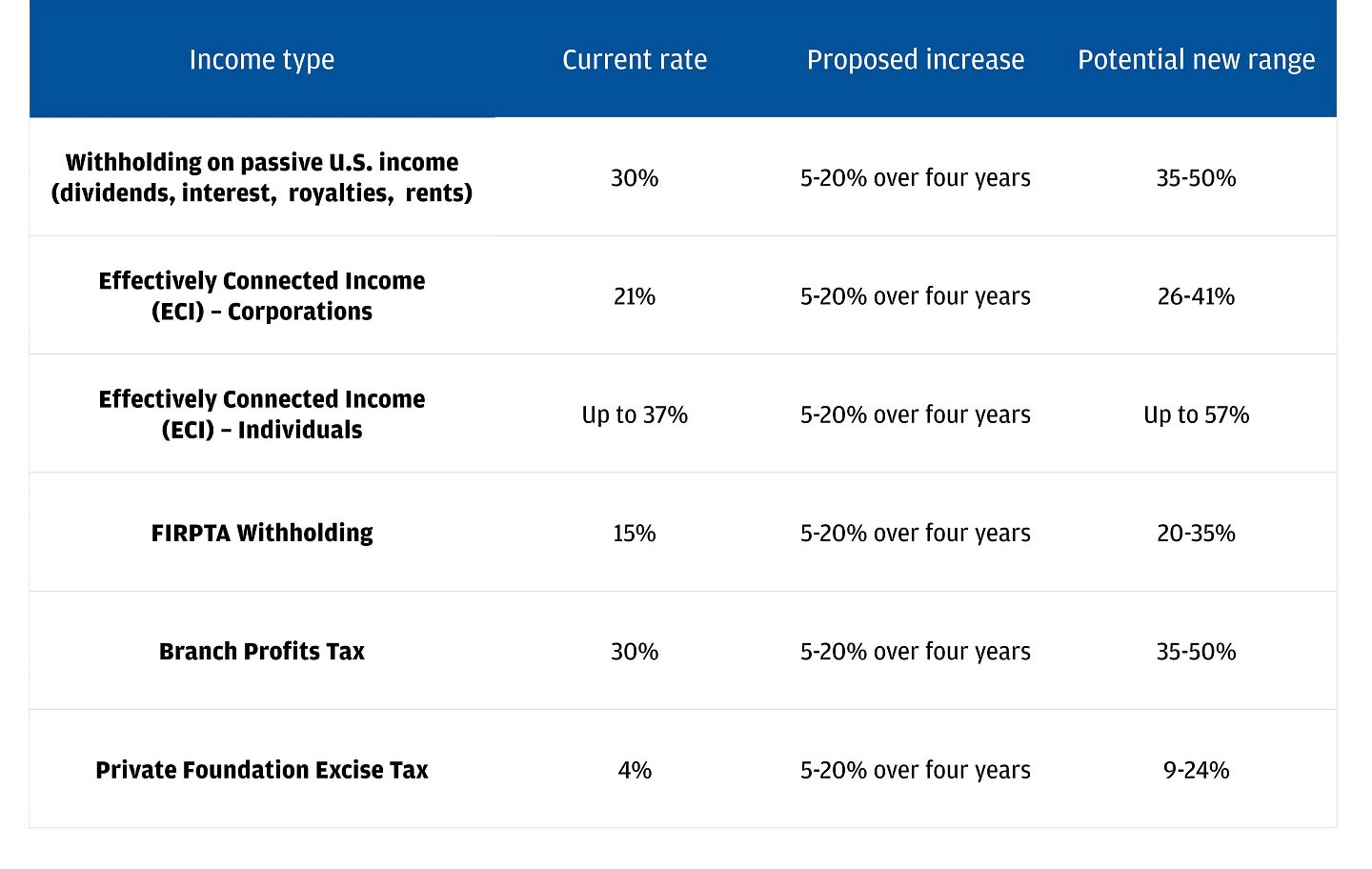

2. Section 899. Up until late last week, most of us probably hadn’t heard of Section 899, given it’s buried in the details of the bill. But now, it’s making headlines and raising questions, especially from those outside the U.S. Why? If passed, it could deter foreign investment in the U.S., reduce demand for U.S. assets and pressure the dollar. Here’s what you need to know about the provision, based on our read of the sparse details. But remember: It’s still just a proposal and could change, be clarified or even scrapped before becoming law.

What it is: It’s shorthand for a “retaliatory” U.S. tax measure on companies and investors from countries deemed to have “unfair foreign taxes.”

Who it targets: Individuals, corporations and governments linked to “discriminatory foreign countries” would be considered “applicable persons.” The main targets appear to be countries taxing U.S. corporations, particularly those with digital services taxes (DSTs) and undertaxed profits rules (UTPRs), such as France, Germany and the UK. Countries on the “naughty list,” which impose such taxes and thus subject to Section 899, would be reported quarterly.

What’s in scope: The most significant item for investors and markets is likely around withholding tax on passive U.S.-sourced income, such as dividends, interest and royalties earned from U.S. investments by foreign investors.

As it currently appears, interest on U.S. government and corporate bonds and deposits is expected to remain exempt under the U.S. portfolio interest exemption, which permits non-U.S. investors to receive interest from specific U.S. debt instruments without withholding tax. Non-real estate-related capital gains should also continue to be considered foreign-sourced and thus not taxable. U.S. dividend and preferred income are the most likely items to fall within the tax scope.

Tax rates for affected parties would increase gradually based on a country’s classification as discriminatory, starting at a 5% increase and adding another 5% each year the country maintains an unfair tax policy, capped at a maximum of 20% above the statutory tax rate for the relevant income item.

However, there’s a lot of uncertainty and we’re closely monitoring the Senate’s stance on this matter. The Trump administration’s gradual and targeted tax approach hints at a strategic move to lower levies on American corporations abroad, implying another example of “America First” policy. Notably, that political stance appears less prominent in the Senate, indicating potential changes as the bill progresses.

Such a tax might prompt foreign investors to demand a “premium” for U.S. assets due to heightened uncertainty and perceived risk, raising concerns about built-up overweights to U.S. asset positions and leading to fund repatriation, intensifying downward pressure on the dollar. To mitigate such risks, we advocate for diversifying investments into international markets not denominated in U.S. dollars, such as European and Japanese equities. Using the MSCI World Index as a benchmark, we recommend allocating about 30% of equity investments to non-U.S. markets, with two-thirds of that in Europe.

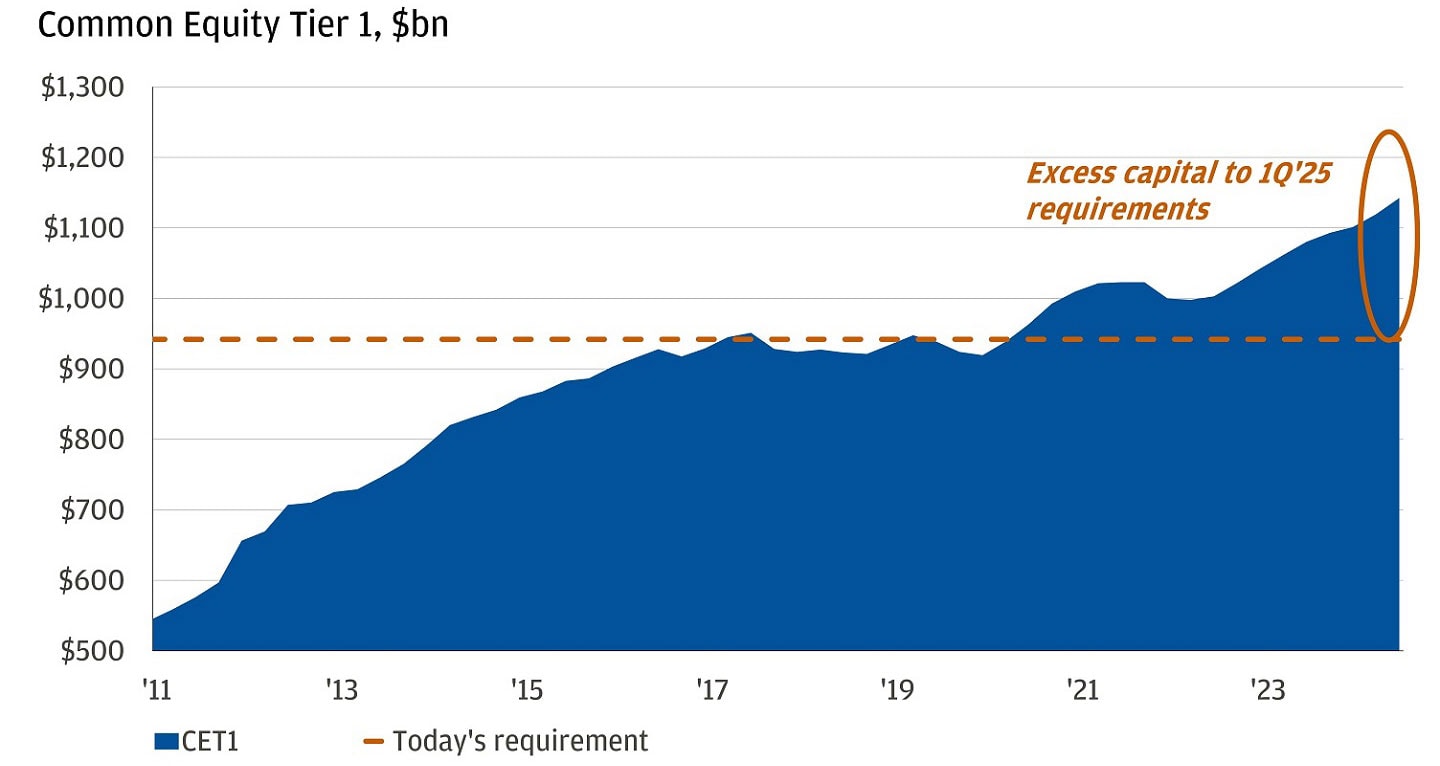

3. Deregulation. Regulation rightfully increased after the 2008 financial crisis in an effort to strengthen bank balance sheets and prevent another financial collapse. Over time, those regulations became increasingly strict each year. In the wake of the March 2023 banking crisis and the proposed Basel III Endgame rules (the final set of reforms and regulations aimed at strengthening the global banking system’s resilience), U.S. banks built capital amid regulatory uncertainty. The view, especially following the 2024 election, has shifted towards banks being overregulated and a policy push for deregulation in the industry.

Banks have ~$200bn of excess capital relative to requirements

Treasury Secretary Scott Bessent has been a prominent advocate for deregulation, emphasizing its importance to unlock non-government lending and stimulate private sector growth. This shift presents investment opportunities in U.S. financial equities and preferreds, given potential changes in bank balance sheets and profitability.

We see deregulation’s effect across four aspects in the banking sector:

Buybacks:

- Excess capital is used for stock buybacks, which can benefit equities.

- Notably, equity buybacks may pose risks for preferreds if funded by increased preferred issuance.

Loan Growth:

- Loan growth drives net interest income and earnings, significantly influencing stock prices.

- Deregulation may lower loan costs, potentially boosting private sector growth.

Supplementary Leverage Ratio (SLR) Reform:

- SLR reforms aim to improve liquidity in the treasury market.

- Excluding treasuries from assets in the SLR calculation could increase tier one capital surpluses, allowing banks to hold fewer preferreds.

- This adjustment could enhance banks’ ability to buy treasuries and facilitate market-making trades, improving overall market liquidity.

Profitability:

- Profitability may rise through reduced expenses and increased capital markets activity.

- Regulatory consolidation could lower operating costs and boost deal activity, enhancing fee revenue and earnings per share (EPS).

Overall, bank deregulation offers opportunities for enhanced shareholder returns, loan growth and merger and acquisitions activity, with improved profitability through increased capital markets activity and reduced regulatory expenses. Both preferreds and equities are likely to benefit from these changes.

Curious about these developments could affect your portfolio? Reach out to your J.P. Morgan advisor.

All market and economic data as of 06/06/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

Explore ways to invest

Take control of your finances with $0 commission online trades, intuitive investing tools and a range of advisor services.

J.P. Morgan Wealth Management