Private credit: Promising or problematic?

Market Update

Investors had every reason to quiver this week – from rumors about Federal Reserve (Fed) Chair Jerome Powell’s future to worries about rising inflation as tariffs make their way through the economy. Yet, stocks powered through and reached new highs once again.

The main driver? Fundamentals.

- Second quarter earnings season kicked off with promising signs. Banks had strong results and many even mentioned how robust the consumer was. Meanwhile, artificial intelligence (AI) investments and relaxed chip export restrictions fueled semiconductor stocks’ impressive streak.

- Inflation edged up but less than anticipated. The latest inflation report showed tariff impacts finally making their way through but the effect hasn’t been too significant and was offset by weakness in some discretionary services. We expect it to increase over the next couple of months but see it as a one-time bump – as long as inflation expectations remain well anchored, we continue to roll on.

- Consumer data delivered positive surprises too. Retail sales rebounded and jobless claims dropped for the fifth consecutive week, easing worries about consumer health. A slowdown is expected, but resilience continues to push through – nudging the U.S. dollar towards its best week since February.

Bottom line: Markets don’t need an “all clear” to move forward. They need solid fundamentals and a touch more clarity. Corporate America is stepping up. Risks are real, but so is resilience.

Cryptocurrencies were in the headlines with “Crypto Week” in Washington too. Congress passed the GENIUS Act, the first of three federal bills aimed at regulating stablecoins. Treasury Secretary Scott Bessent expressed confidence that the stablecoin economy could grow from $195 billion to over $2 trillion and bitcoin surpassed the $120,000 mark.

Our take: While not a true portfolio diversifier due to its volatility and positive correlation to risk assets, bitcoin has gained institutional acceptance. We think of it as an “out-of-the-money” call option: potential for big gains but high risk of loss. We wouldn’t be surprised if its popularity continues to grow as currency diversification worries persist, but it’s important to understand what bitcoin is and isn’t.

Below, we discuss our thoughts on JPMorganChase Chairman and CEO Jamie Dimon’s latest comments regarding private credit and the industry overall.

Work with an advisor

Our advisors can provide ongoing financial advice on how your portfolio can adapt to the changes in the market, your life and your goals.

Spotlight

Dimon has cautioned that private credit could become a “recipe for a financial crisis” if mismanaged. Though some see it as a doomsday call, it’s really a push for responsible practices amidst the risks.

He has flagged risks like opaque ratings, aggressive leverage, looser covenants and illiquid vehicles with five-to-10-year lockups over the past few months. Drawing parallels to the subprime mortgage crisis of 2008, he cautioned that mounting losses in the rapidly growing private credit market – which is now as large as the markets for leveraged loans or high-yield bonds – could amplify systemic stress. And he’s not alone: The Fed’s latest Financial Stability Report recently surveyed investment professionals about potential economic shocks and private credit made the list.

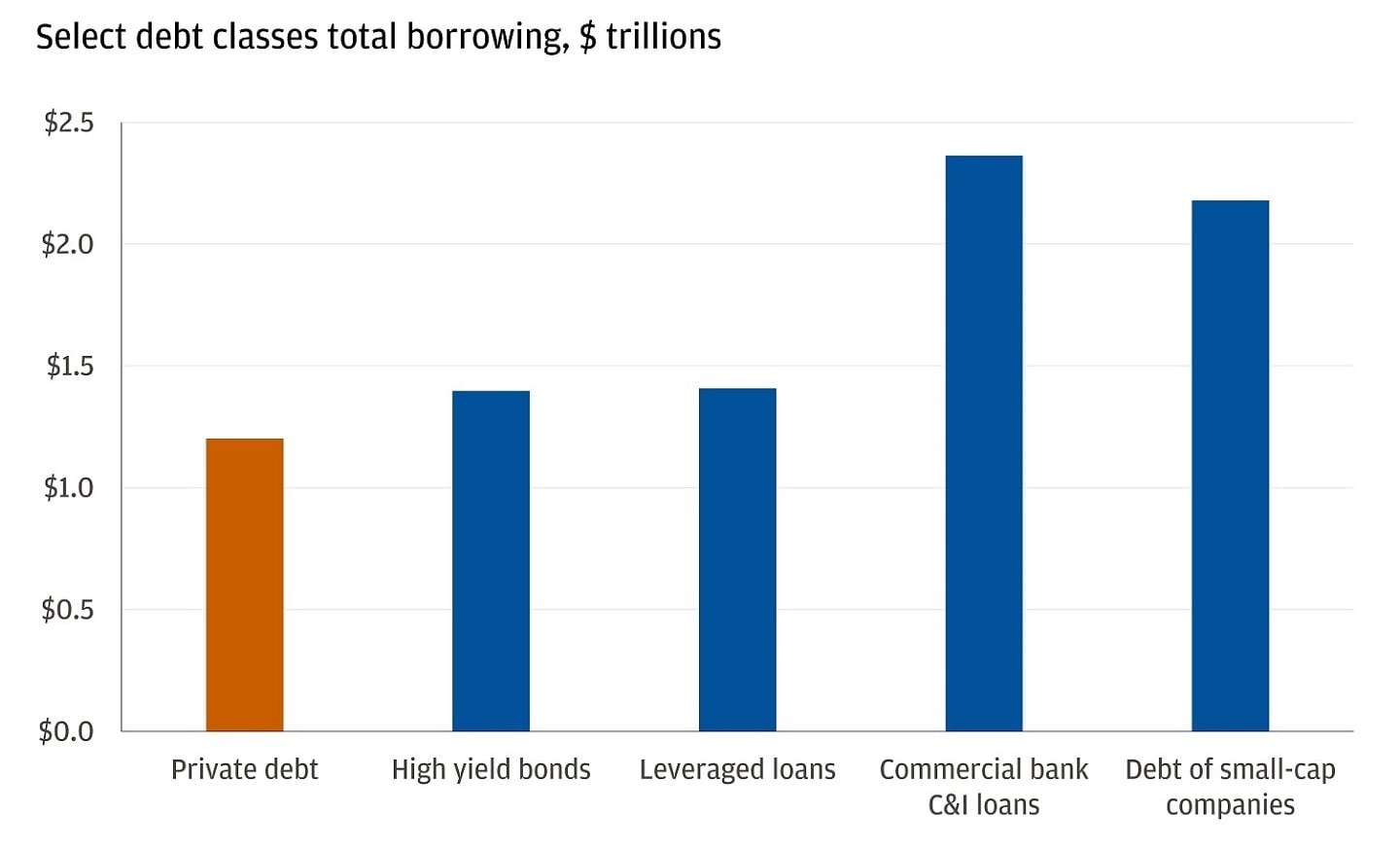

Private credit is now a major category of borrowing

While Dimon’s warnings highlight real risks, they shouldn’t be misconstrued as a negative stance on private credit. He’s advocating for responsible practices and sees potential, as shown by J.P. Morgan’s own $50 billion commitment to the space.

Dimon acknowledges that “parts of direct lending are good” and that the asset class can positively fill lending gaps left by banks under Basel III and higher rates, provided there’s greater transparency, disciplined underwriting and prudent regulation. After all, the risk lies with bad actors, not the asset class itself. Private credit isn’t inherently dangerous; it’s the execution that matters. With thoughtful structuring, it can deliver strong risk-adjusted returns without systemic issues.

In our view, there are three key points to keep in mind:

1) Fears of private credit leading to a systemic crisis are overstated. While the industry’s growth is significant, it’s still a smaller slice of corporate borrowing and not large enough to pose systemic risk. To level set: Over the past decade, corporate borrowing has grown at a 5.5% annualized pace, with commercial and industrial bank loans at 3% and private credit at 14.5%. Yet, private credit assets under management (AUM) is about $1.2 trillion, just 9% of all corporate borrowing. While meaningful, we believe it is not large enough to threaten the broader economy.

Even factoring in banks’ direct exposure to private debt managers, the risk remains limited and unlikely to trigger a ripple effect that would destabilize the banking system and create systemic risk. To boot, bank lending to private equity firms, Business Development Companies and private debt managers totaled about $320 billion last year – with over a third going to private debt managers. This is modest compared to the $2 trillion in total loan commitments to non-bank financial institutions.

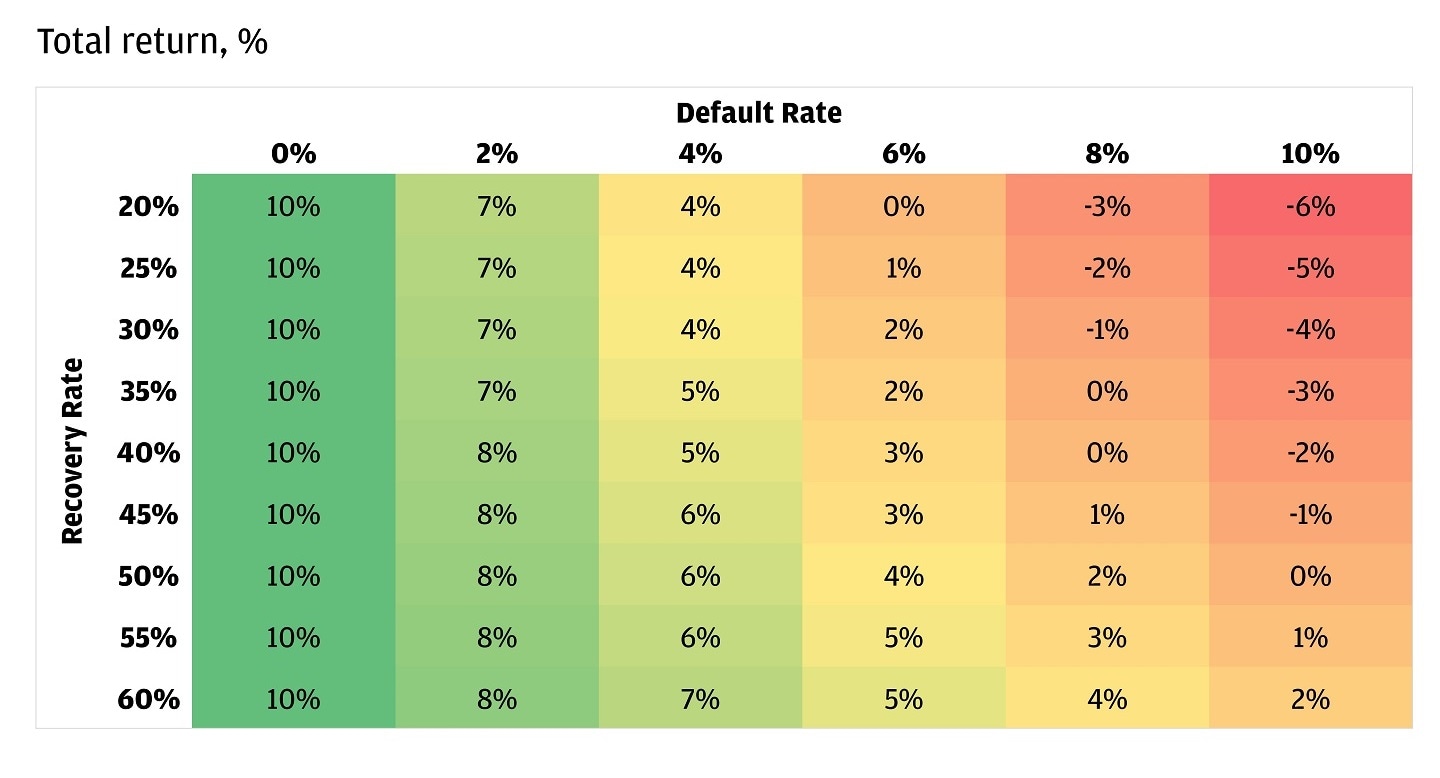

2) We’d need a major economic downturn to see negative total returns in this space. In senior direct lending, higher starting yields and seniority in the capital structure help the asset class stay resilient by providing a cushion against potential losses. As a simplified example, with a starting yield of 10% and assuming a 1x turn of leverage over a long-term holding period, default rates would need to rise above 6% and recovery rates fall below 40% to result in negative returns.

A significant economic downturn would be required to result in negative total returns

For context, private credit default rates were around 2.4% by the end of Q1 2025. Also, high yield bond defaults are currently at about 1.5%, below the 25-year average of roughly 3%. The last time high yield bond default rates exceeded 6% was during the COVID-19 pandemic and the Global Financial Crisis, while recovery rates haven’t dipped below 40% since the pandemic. It’s rare for high-quality managers to encounter such high defaults and low recoveries.

3) Weaker fundamentals than public markets demand higher selectivity. Yes, the private credit industry shows lower quality fundamentals compared to public markets, including high yield bonds and broadly syndicated loans. Overall, interest coverage is weaker (2.1x versus public at 3.9x), leverage is higher (5.6x versus public at 4.6x), and earnings before interest, taxes, depreciation and amortization (EBITDA) margins are slimmer (14.9% versus public at 16.4%).

The good news? Investors have historically been rewarded for the additional risk, as private credit has outperformed high yield bonds by around 150 basis points over the past decade. As the market expands, manager dispersion is expected to increase, emphasizing the need for careful selection. This underscores the vital role of our due diligence team, dedicated to identifying high-quality managers who possess scale, seasoned management teams and a proven track record of achieving target returns with minimal impairment.

In all, there are risks, and the industry won’t be immune to a potential economic slowdown. While we believe that high quality managers within senior direct lending will be able to navigate the impact of an economic downturn, we recommend diversification across the various segments of private credit outside of just senior direct lending (think asset-backed credit, opportunistic credit and secondaries). Double-clicking on opportunistic credit, while we don’t expect a macro distress cycle, pockets of dislocation may emerge as growth moderates, creating opportunities for specialized lenders.

Moving forward, we anticipate returns to normalize to historical ranges of 8% to 10% as base rates move lower, making diversification into other areas of private credit crucial.

Reach out to a J.P. Morgan advisor for more on how these insights could affect your investing portfolio.

All market and economic data as of 07/18/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

Explore ways to invest

Take control of your finances with $0 commission online trades, intuitive investing tools and a range of advisor services.

Head of Alternative Investment Strategy, J.P. Morgan Private Bank

Global Investment Strategist

Global Investment Strategist