The updated federal income tax brackets for the 2026 tax year

Editorial staff, J.P. Morgan Wealth Management

- The IRS recently announced updates to the U.S. federal tax brackets for the 2026 tax year, affecting tax returns filed in spring 2027.

- Tax brackets refer to ranges of income that are each subject to separate, progressive federal tax rates.

- The brackets that apply to you depend on both your taxable income for the year and your tax-filing status.

- Understanding how tax brackets work not only may help you prepare to file your taxes but also can inform your long-term tax strategy.

Tax season always seems to arrive sooner than expected. And while you’re likely focused on submitting your 2025 return in spring 2026, the IRS has already announced its updates to the federal income tax brackets for the 2026 tax year. These updates will affect your 2026 take-home pay as well as the tax return you’ll file in spring 2027.

Why does the IRS adjust the federal tax brackets every year, you might be wondering? The federal agency does this to account for inflation. Without these annual adjustments, inflation could push taxpayers into a higher income bracket when their nominal income increases without a corresponding increase in real purchasing power. This phenomenon is known as “bracket creep.”

You should always speak to a tax professional about your personal tax situation. You can get started by reading on to find the 2026 tax tables for every filing status, plus important information about U.S. tax brackets – including what they are, how they work and why they matter.

First things first: What are U.S. tax brackets?

A U.S. tax bracket is a defined range of income taxable at a defined federal tax rate. Each year, the IRS publishes a tax rate table for each filing status that includes a set of progressive tax “layers,” or brackets. Currently, each table has seven tax brackets with tax rates ranging from 10% to 37%.

As a U.S. taxpayer, you start in the lowest bracket of your applicable tax table, where the first portion of your income is taxed at the lowest rate. Once you hit the limit for the lowest income bracket, you jump to the next-higher bracket, where the following portion of your income is taxed at that rate. The process continues until all your income has been accounted for. The rate on your last dollar earned is known as your marginal tax rate.

A common misconception among taxpayers is that the rate of your highest tax bracket – again, your marginal tax rate – applies to all your income. This isn’t true. U.S. income tax brackets are tiered, so taxpayers pay different rates for different “levels” of their income. The only taxpayers who pay the same rate on all their income are those whose income does not exceed the top of the lowest tax bracket.

Here’s an example. Let’s say you’re a single filer with $60,000 in taxable income for 2026. The applicable federal tax rates for single filers for tax year 2026 are as follows:

- 10% for $0 to $12,400 of income

- 12% for $12,401 to $50,400 of income

- 22% for $50,401 to $105,700 of income

As a result, you’d be taxed as follows:

- 10% on the first $12,400, totaling $1,240

- 12% on the next $38,000, totaling $4,560

- 22% on the remaining $9,600, totaling $2,112

So, your total federal tax due would be $7,912.

Interested in working with an advisor?

Work 1:1 with our advisors to help build a personalized financial strategy that’s built around you.

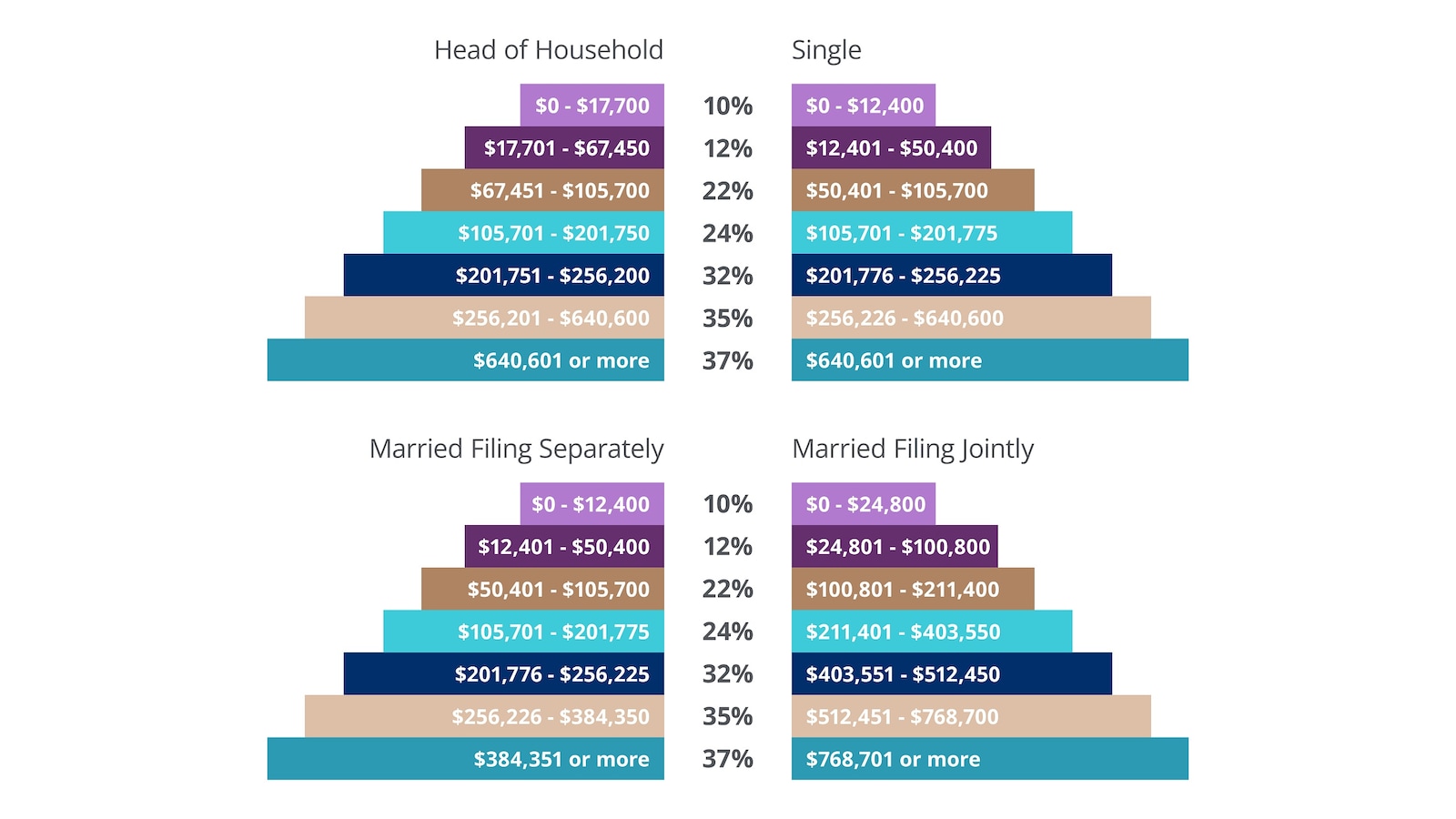

2026 U.S. federal income tax brackets

As we covered, federal income tax brackets for tax year 2026 have undergone changes to account for inflation. Below we outline the updated brackets.

U.S. federal income tax brackets for 2026

Step-by-step guide to finding your 2026 tax brackets

Determining which tax brackets apply to you is a process, but it’s relatively straightforward if you have all the relevant information. Follow the steps below to arrive at your applicable brackets for the 2026 tax year. (Note, however, that you’ll likely be estimating your income until you have all the official documentation, which may not be until early 2027.)

Gather your income documents

Start by gathering all the documents that show how much income you’ve earned during the year. Having all your records organized and ready to reference will make the following steps much easier.

Calculate your total (gross) income

While your tax brackets are based on your taxable income and not your total (gross) income, you’ll need to calculate your total income first. (Taxable income is what’s left over after you subtract eligible deductions and adjustments from your total income.)

Once you’ve determined all your sources of income for the year, add everything together. IRS Form 1040 walks you through how to calculate your total income on lines 1a through 9. Tax software programs can also guide you through the process by prompting you to answer a series of questions.

Subtract deductions to find your taxable income

Once you know your total income, you can subtract your deductions:

- Above-the-line deductions are determined in Part II of Schedule 1 (Form 1040). Go line by line to identify any adjustments you’re eligible for, such as those for alimony payments, business use of your car or money invested in a traditional individual retirement account (IRA).

- Next, calculate your itemized (below-the-line) deductions for the year to see if they amount to more than your standard deduction. Claim whichever number is higher.

- Certain business owners are allowed to deduct up to 20% of their qualified business income, along with 20% of dividends from qualified real estate investment trusts and income from qualified publicly traded partnerships.

After subtracting all your applicable deductions, you’ll be left with your taxable income.

Identify your filing status

In addition to your income, your tax brackets are determined by your filing status. You’ll need to choose from the following statuses:

- Single: Single filers are individuals who are unmarried or legally separated from their spouse on the last day of the year and don’t qualify for another filing status.

- Head of household: These are filers who are unmarried on the last day of the year and have paid more than half the cost of keeping up a home for the year, while having a qualifying person live with them for more than half the year.

- Married filing jointly: These are filers who are married and agree to file a joint return.

- Married filing separately: These are filers who are married and agree to file separate returns.

- Qualifying surviving spouse: These are filers whose spouses have passed away within the past two years. Qualifying surviving spouses are taxed at married filing jointly rates, so they should reference that tax rate table.

Once you know your status, you can identify your appropriate tax table. Refer to the figure above for the 2026 U.S. federal income tax brackets by filing status. Again, you’ll use these when filing your taxes in spring 2027 for income earned in 2026.

If you’re not sure which is right for your situation, use the IRS “What is my filing status?” toolOpens overlay.

The bottom line

Tax brackets matter because they directly determine how much you’ll owe in federal income taxes each year. The brackets are adjusted annually for inflation, so you’ll need to check them each year when preparing to file your taxes.

The brackets can also be helpful for tax planning. By understanding the brackets’ income thresholds, you can make choices throughout the year to help manage your tax bill. For example, you may want to time certain deductions, retirement contributions or income payments in such a way that they help keep your marginal tax rate lower. In short, understanding your tax brackets is important for both calculating your annual tax bill and planning strategically.

Invest your way

Not working with us yet? Find a J.P. Morgan Advisor or explore ways to invest online.

Editorial staff, J.P. Morgan Wealth Management