How the S&P 500 finished May with nine consecutive weekly gains

Global Investment Strategist

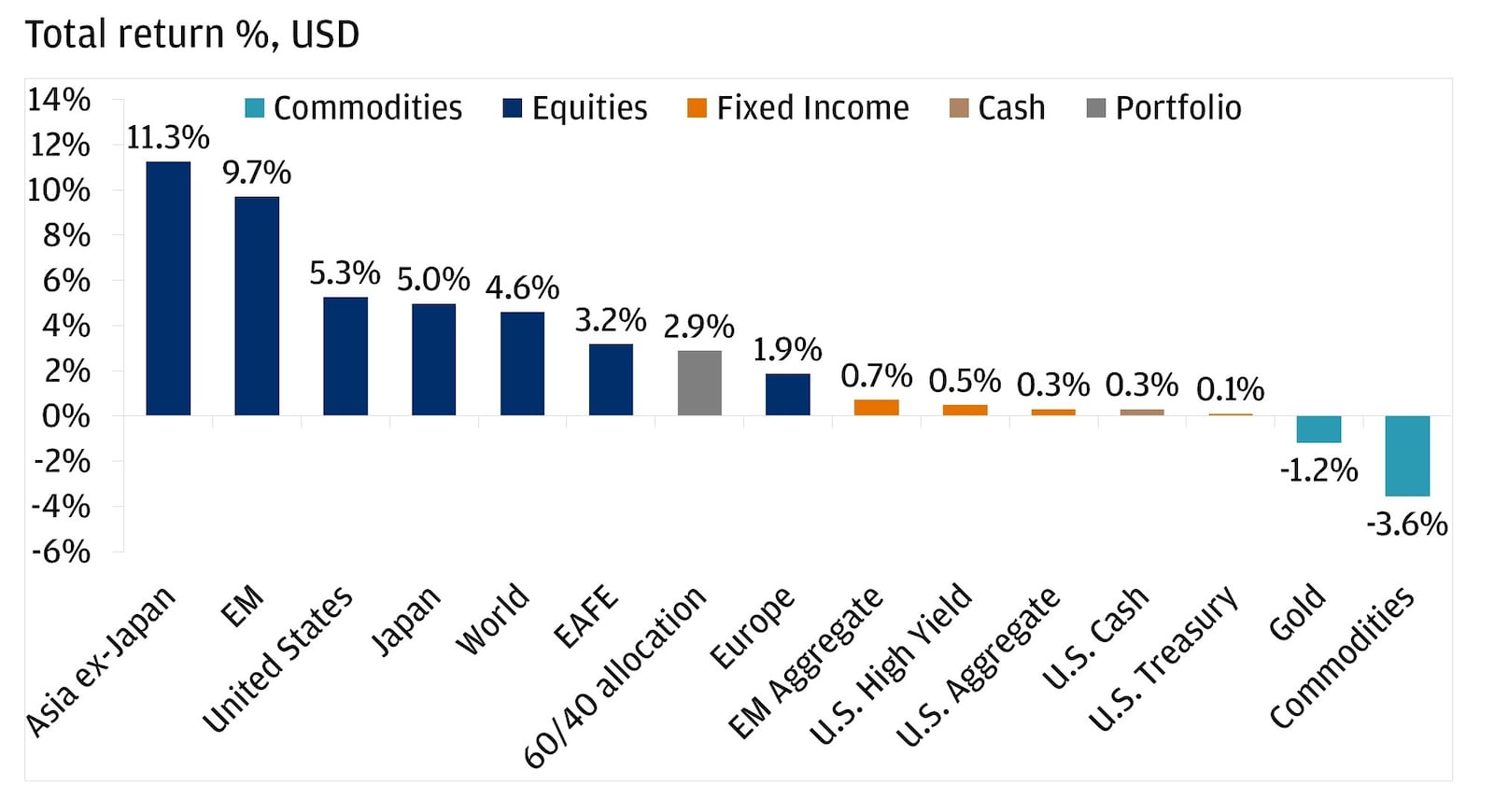

May picked up where April left off in markets, as investors experienced a continued global equity rally (Asia ex-Japan +11.3%, emerging markets +9.7%, and U.S. equities +5.3%), fixed-income returns were relatively flat (U.S. Aggregate +0.3%, U.S. Treasuries +0.1%) and gold underperformed (-1.2%).

The market moves investors witnessed in May were shaped by a combination of factors, including ongoing hopes for a resolution to the Iran war evolving Federal Reserve policy expectations and resilient U.S. corporate earnings.

Global equities deliver impressive May rally

Below, we discuss how these developments impacted markets in May.

Middle East conflict: A persistent problem, but the global shock is fading

Geopolitical risk remained a defining theme for May, with the ongoing Iran war continuing to shape the macro backdrop. The Strait of Hormuz, a chokepoint for roughly 20% of the global oil and liquefied natural gas (LNG) trade, has remained effectively closed since the conflict began, with only a limited number of vessels moving through the strait each day.

The most direct impact of the conflict on markets continues to be via energy prices. Elevated oil prices have trickled into inflation data, with April’s Consumer Price Index (CPI) showing headline inflation ticking up to around 3.8% year over year. The increase has been driven largely by energy costs rather than a broad-based acceleration across the economy.

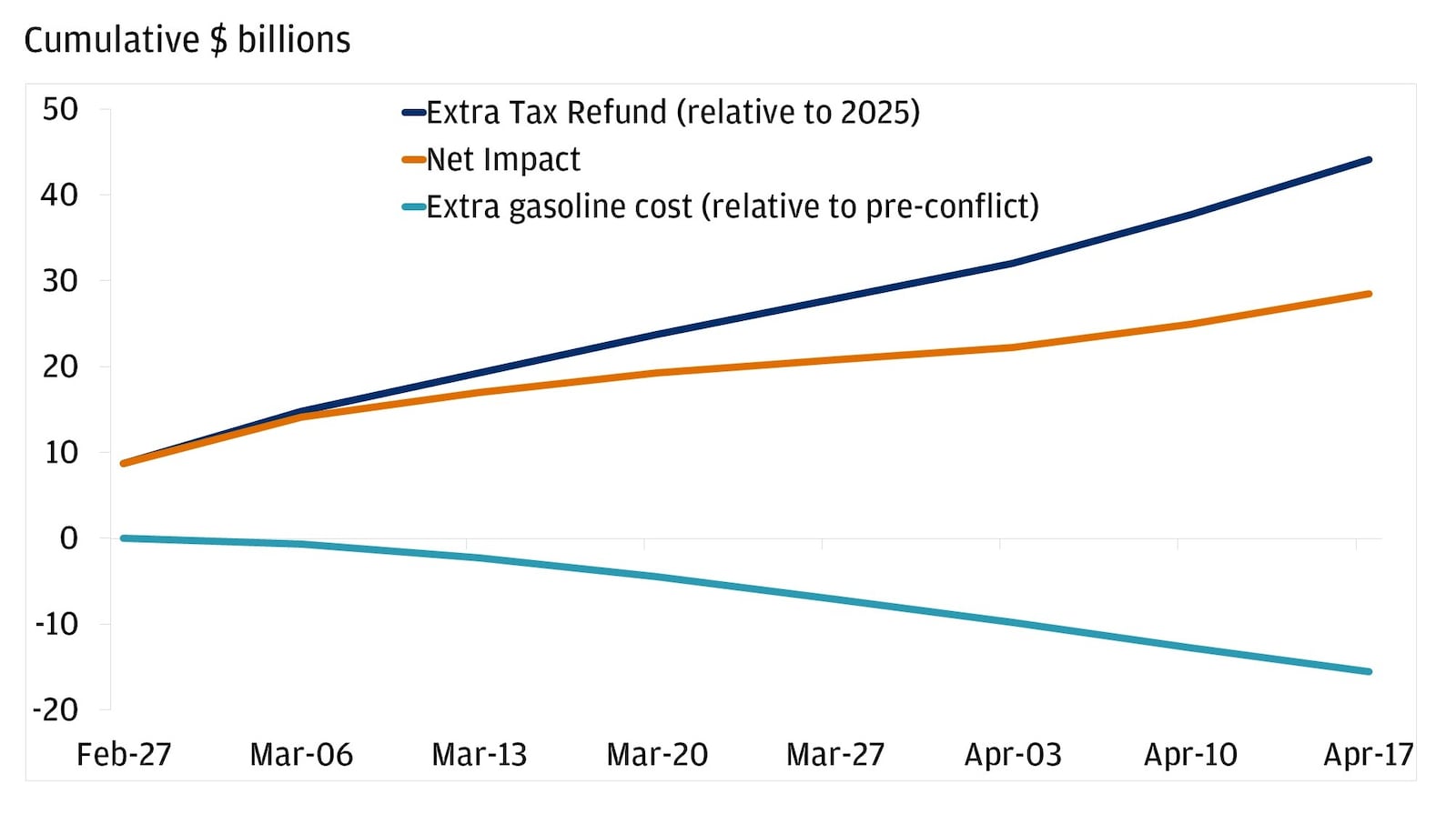

While higher gasoline prices have seemingly created a drag on household budgets, that pinch has so far been offset by elevated tax refunds stemming from the One Big Beautiful Bill Act’s changes to the U.S. tax code. As summer approaches and the temporary refund boost fades, whether energy prices continue to be elevated will become increasingly important to watch. If the conflict continues on the path of de-escalation and the Strait of Hormuz reopens, oil supply could normalize, helping to potentially move energy prices lower and ease inflation pressures, but that outcome isn’t certain.

Higher gasoline mitigating a third of tax refund boost so far

Our base case remains a gradual and uneven de-escalation of the conflict, with oil prices moving back toward the $80-per-barrel range this year. As headlines swirled in May about a potential extension of the ceasefire, Brent crude fell nearly 20% – one of its largest declines since the COVID-era swings – and by the end of May was in the range of $90–$95 per barrel. The pullback in oil prices suggests investors aren’t as worried about severe supply disruption scenarios.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

Bond market volatility emerges

With the direct shock of the conflict fading, investor focus in May shifted to the bond market and the outlook for Federal Reserve (Fed) policy. Earlier in the year, markets were expecting the Fed to deliver 50 basis points of rate cuts by year-end. However, elevated inflation stemming from the Iran war, combined with resilient economic data, led markets to reprice a more cautious path for monetary policy, with current expectations now including the possibility of a rate hike by the end of 2026.

This shift in expectations sparked volatility in the bond market. U.S. Treasury yields climbed to multiyear highs, with the 10-year reaching approximately 4.67% and the 30-year touching 5.18% in mid-May. These moves were partially driven by elevated inflation and steady economic growth.

The rise in yields has prompted some investors to have concerns about a potential repeat of 2022, when surging inflation and aggressive Fed rate hikes led to broad losses across both equities and bonds. At that time, inflation was widespread across goods and services, wage growth was accelerating and policy rates were rising rapidly from historically low levels.

We believe today’s environment looks materially different from 2022. Inflation pressures, while elevated, remain more concentrated in energy rather than broad-based across the economy. Wage growth has moderated, and the labor market is no longer exhibiting the same degree of overheating. At the same time, yields are starting from a much higher base, providing a built-in income cushion that was largely absent earlier in the cycle. Our current base case expects the Fed to stay on hold this year.

Earnings drive markets

Despite higher yields, elevated inflation and ongoing geopolitical conflict, equities moved higher across regions in May, underscoring that markets are largely driven by fundamentals.

A robust earnings season helped the S&P 500 achieve more than 10 all-time highs in May. First-quarter results marked the sixth consecutive quarter of double-digit earnings growth for the index. Notably, the strength was not limited to tech: Ten of the S&P’s 11 sectors reported positive year-over-year earnings growth.

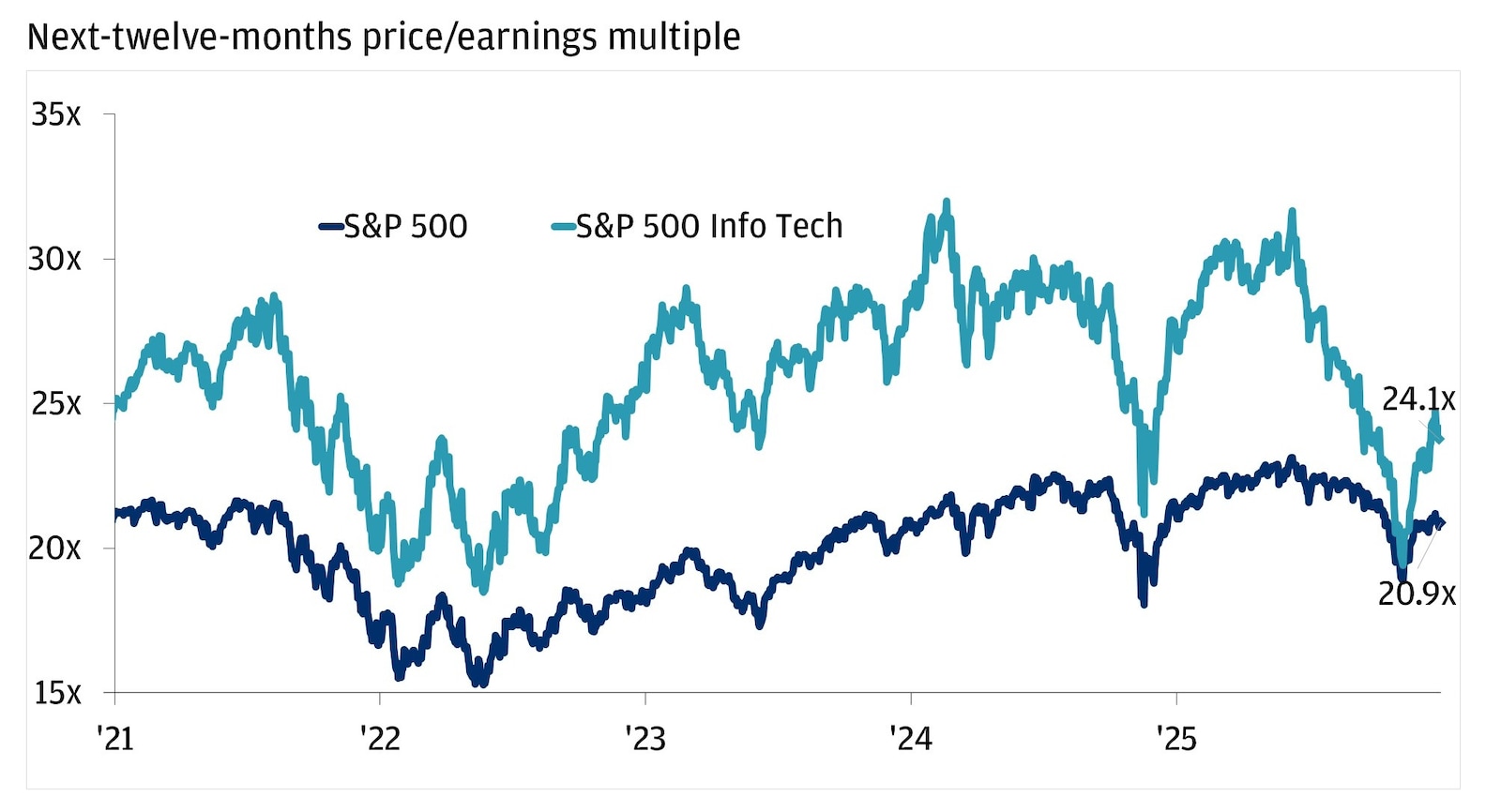

Importantly, valuations remain reasonable. While the S&P 500 is trading near all-time highs, its price-to-earnings multiple is only slightly above the five-year average at 21x and has actually contracted since the end of last year as earnings growth has outpaced price appreciation. This suggests that the rally is being driven more by improving fundamentals than by increasing investor risk appetite.

Tech valuations remain below the 5-year average

International equities also delivered impressive results. Asia ex-Japan led global markets, up 11.3%, with Korea and Taiwan benefiting from strong demand for semiconductors and technology related to artificial intelligence. Even Europe (+1.9%), which has been more vulnerable to recent energy price shocks, managed a positive total return in May as oil prices pulled back and investors grew more comfortable with the macro outlook.

We continue to see earnings as the primary driver of equity markets. As long as companies can deliver on profit growth, even in the face of persistent macro risks, markets are likely to remain supported by fundamentals rather than sentiment alone.

Fundamentals carried markets in May, but risks remain

May’s rally serves as a reminder that strong earnings and fundamentals drive markets, even as risks from geopolitical conflict and elevated inflation persist. As we move into June, a key question for investors will be whether the Iran war moves closer to a resolution. However, investors who stay diversified and committed to their strategy are often in the best position to achieve their goals regardless of how the environment evolves.

Invest your way

Not working with us yet? Find a J.P. Morgan Advisor or explore ways to invest online.

Global Investment Strategist