Can a custodial account affect financial aid eligibility?

Editorial staff, J.P. Morgan Wealth Management

- Custodial accounts – including Uniform Gifts to Minors Act (UGMA) or Uniform Transfers to Minors Act (UTMA) accounts – are considered student assets on the Free Application for Federal Student Aid (FAFSA) and are assessed at a higher rate than parent assets.

- The financial aid formula assesses student assets at up to 20% (versus 5.64% for parent assets), so a well-funded custodial account could reduce financial aid eligibility.

- Families can plan ahead by spending down custodial assets before the base year or saving money in 529 plans.

When saving for your child’s future, a custodial account may seem like a straightforward way to save or invest on their behalf. But when it comes time to apply for financial aid for higher education, these accounts can have more impact than many families expect.

Custodial accounts are considered assets owned by the child, which means they carry more weight in financial aid calculations than assets owned by a parent. Understanding how custodial accounts are treated in financial aid calculations can give your family the chance to plan ahead.

How custodial accounts work

A custodial account is a financial account opened by an adult (the custodian) on behalf of a minor (the beneficiary) and allows the adult to manage money or investments on behalf of the minor. They can be bank or investment accounts, and the two most common types are UGMA and UTMA accounts. A UGMA account holds cash and financial securities, while a UTMA account allows for a broader range of assets, including real estate and other property.

When the child reaches the age of majority – typically 18 or 21, but sometimes up to 25 depending on the state, account type and age chosen when the account is opened – the child takes over the account and has full control. And because of the way custodial accounts are structured, once money is contributed, it becomes an irrevocable gift to the child and cannot be taken back for the adult’s own use – so it’s all the child’s once they reach the age of majority.

Custodial accounts can be used for a variety of goals, such as college savings, a head start on retirement savings or something else for the child’s future. They can be easy and inexpensive to set up and may be more flexible in how the funds can be used than other accounts, making them an appealing option for many families.

Custodial accounts, unlike 529 plans, do not offer significant tax benefits and can impact the child’s financial aid eligibility. However, they can be used for any purpose that benefits the child. 529 plans, on the other hand, are tailored specifically for educational expenses, allow tax-free growth and withdrawals for qualified costs, and are usually owned by parents. Any “nonqualified” use of the funds, usually for purposes unrelated to education, may incur an additional tax as well as ordinary income tax.

Save and invest for a child’s milestones

Explore self-directed investing and managed UTMA (custodial) accounts to help you save, invest and gift assets for a child’s future, with no contribution limits.

How financial aid calculations work

To fully grasp how a custodial account affects financial aid, it’s important to understand how aid eligibility is determined in the first place. The main method is the Free Application for Federal Student Aid (FAFSA), which most colleges use to assess need-based financial aid. In addition, some private colleges and scholarship programs require the College Scholarship Service (CSS) Profile, a separate form that has a fee (which can be waived for students whose families earn less than $100,000 per year). Before completing the CSS Profile, students should check whether their intended college or scholarship program requires it.

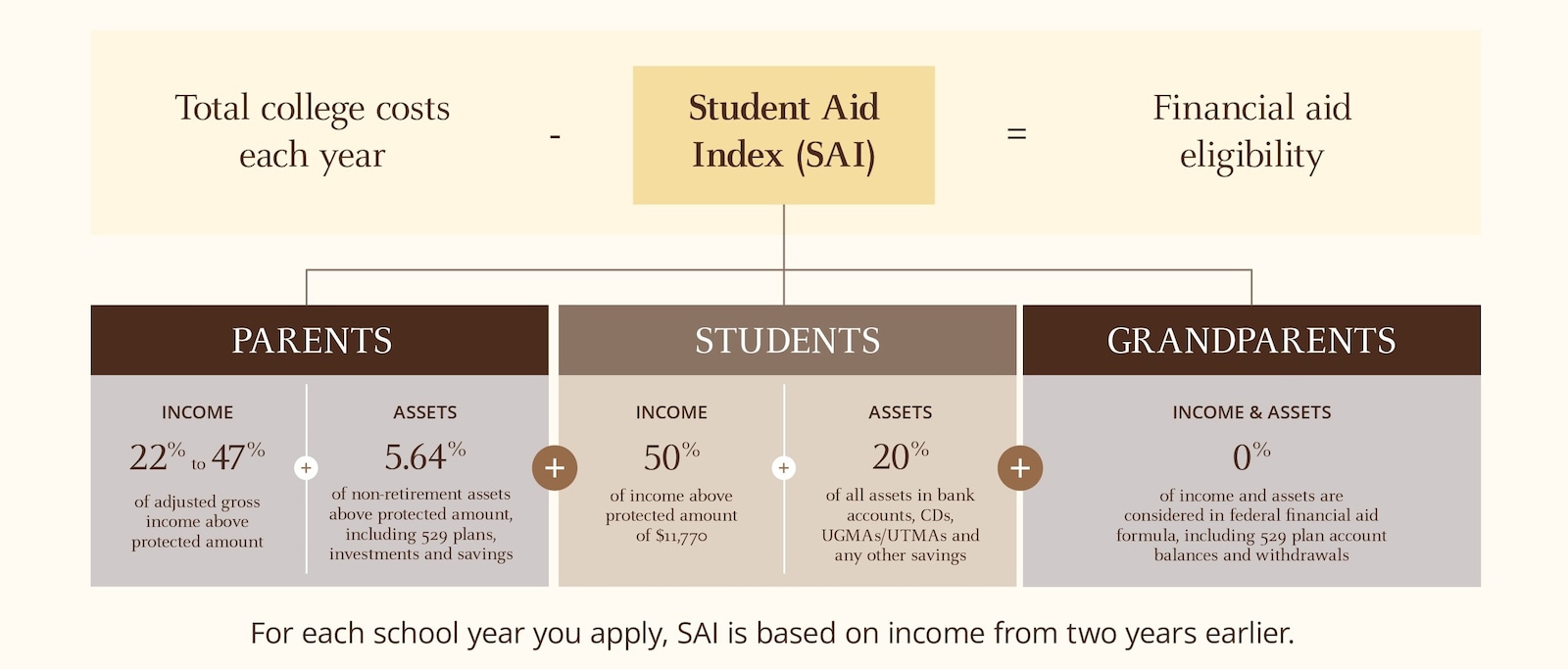

When you submit the FAFSA, the result is a number called the Student Aid Index (SAI), essentially a financial aid eligibility score that schools use to determine how much federal aid you may qualify for. The number is calculated from the tax information you provide, most of which is pulled directly from the IRS. One important thing to know: The SAI isn’t a dollar amount your family may owe – it’s just an index number. For example, a negative SAI actually works in your favor, signaling greater financial need.

You might also have come across the term “expected family contribution” (EFC) in the past. To be clear, the EFC isn’t a different or an extra number – it’s simply the old name for what’s now the SAI. The SAI replaced the EFC and serves the same purpose in financial aid calculations. If you want a rough idea of your number before filing, the Federal Student Aid EstimatorOpens overlay is a great place to start.

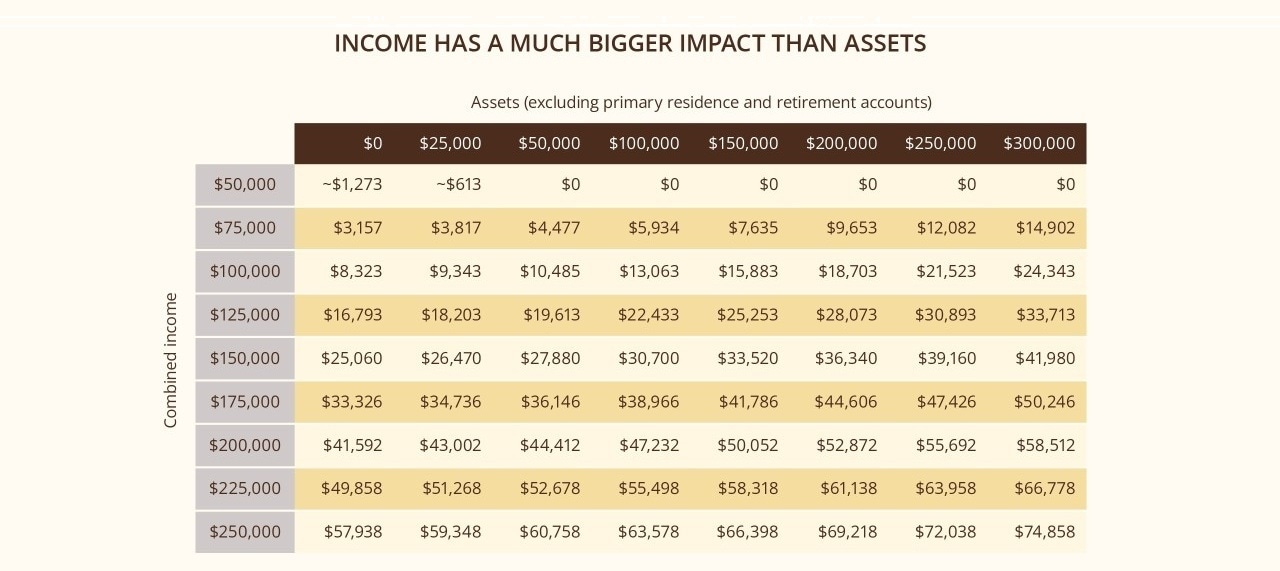

Example Annual Student Aid Index (SAI)

Custodial accounts and their impact on aid eligibility

One critical factor in the financial aid calculation is how assets are treated depending on who owns them. That is, parent and student assets are not weighed equally. Because the assets in a custodial account legally belong to the child, they are reported as student assets on the FAFSA. Student assets are assessed at a rate of up to 20%, while parent assets are assessed at a much lower rate of 5.64%. That is, students are expected to use up to 20% of their assets to pay for higher education; parents are only expected to use up to 5.64% of their countable assets. Because students are expected to contribute a larger portion of their own assets toward college expenses, this difference can significantly affect the amount of financial aid a student is eligible to receive.

Here’s an example of how that could work: If a student has $10,000 in a custodial account, the FAFSA formula could reduce their aid eligibility by as much as 20%, or $2,000. If that same $10,000 were held in a parent-owned account, the reduction in aid eligibility would be closer to $564 because the parent rate is 5.64%. That’s a difference of more than $1,400 from the same amount of money, simply based on who owns the account.

Families of students applying to private colleges that use the CSS Profile should know that this form may treat assets even more broadly. For example, the CSS Profile requires all 529 plans listing the student as a beneficiary to be reported regardless of who owns the plan. The CSS Profile may also factor in sibling assets under certain conditions.

Federal financial aid eligibility

Strategies to minimize impact on financial aid

The good news is that families who plan ahead have real options. There are several strategies worth knowing about.

One approach is to spend down the minor’s custodial assets before the base year, which is the tax year the FAFSA uses to assess finances and which is two years before the child expects to go to college. (For example, 2024 is the base year for the 2026–27 FAFSA.) The FAFSA considers asset values at the time of application, so using custodial account funds for legitimate expenses related to the child before that window can reduce the balance that gets reported. Just be sure to spend the money in the child’s custodial account on expenses that directly benefit the child.

Another option is to redirect savings into accounts with more favorable implications for financial aid. Prepaid tuition plans, 529 plans and Coverdell education savings accounts controlled by parents are assessed at the parent-owned asset rate rather than the student rate, making them more efficient vehicles from a financial aid standpoint.

Assets owned by grandparents (or anyone other than the student and the student’s parents) do not count as resources on the FAFSA, although they might on the CSS Profile. And although they used to count against the student for financial aid purposes, under current law, distributions from grandparent-owned 529 plans do not count as student income and so are completely neutral when it comes to financial aid.

Working with a financial professional who understands the relationship between savings strategies and financial aid eligibility is the most reliable way to optimize your specific situation.

Other considerations: Legal and tax implications

Beyond financial aid, there are a few other things to consider with regard to custodial accounts. Once assets are transferred into a custodial account, that transfer is irrevocable. When the child reaches the age of majority, they gain full legal control of the funds and can use them however they choose, regardless of the original intent of the account.

On the tax side, income generated in a custodial account is subject to what’s commonly known as the “kiddie tax.” For 2026, the first $1,350 of a child’s unearned income (usually interest, dividends and capital gains) is tax-free, the next $1,350 is taxed at the child’s rate and any unearned income above $2,700 is taxed at the parent’s marginal rate – regardless of whether the income is reported on the child’s separate tax return or is included on the parents’ return. If the kiddie tax applies, the child typically files IRS Form 8615Opens overlay with their tax return. This form calculates how much of the child’s income is taxed at the parent’s rate.

So, putting a large amount of assets in your child’s name won’t give you much of a tax break, especially if you’re in a higher income bracket.

These legal and tax factors highlight why custodial accounts should be considered within the context of your overall family financial plan, not simply on their own. While these accounts can offer real flexibility, they also present important considerations that families should weigh carefully.

The bottom line

Custodial accounts can offer valuable savings opportunities, especially for families seeking flexibility in how the funds may be used in the future. However, their classification as student-owned assets on the FAFSA means they are assessed more heavily in financial aid calculations than parent-owned savings vehicles. The difference in assessment rates between student and parent assets is significant enough that a well-funded custodial account could meaningfully reduce a child’s eligibility for need-based aid when applying for college.

Frequently asked questions about custodial accounts and financial aid

A custodial account (UGMA or UTMA) is owned by the child and managed by an adult. The money in the account can be used for virtually any expense that benefits the child and then for anything they choose once they reach the age of majority and have full control of the account. A 529 plan is designed specifically for education costs and offers tax-free growth and withdrawals for qualified education-related expenses (and assesses tax and potentially penalties for nonqualified withdrawals). From a financial aid perspective, parent-owned 529 plans are assessed at a lower rate than custodial accounts. Grandparent-owned 529 plans are not included in the calculation of the Student Aid Index.

Custodial accounts are reported as student assets on the FAFSA because the child is the legal owner of the assets in the account. Student assets are assessed at up to 20% of their value when calculating a student’s expected contribution to college costs, which is considerably higher than the maximum 5.64% rate applied to parent assets. This can reduce the amount of need-based aid a student is eligible to receive.

Yes. You can liquidate custodial account assets and contribute the proceeds to a custodial 529 plan, where the student remains the account beneficiary but the funds receive more favorable financial aid treatment. Keep in mind that liquidating assets may trigger capital gains taxes, and control of the 529 plan still becomes the child’s at the age of majority. A financial professional can help you with this decision and transfer if you feel it’s right for your family’s situation.

Yes. Custodial accounts have no restrictions on how funds are used, as long as the spending benefits the child. This might include a car, travel, extracurricular activities or any other legitimate expense. Once the child reaches the age of majority, they can use the funds for anything they choose, with no conditions attached.

Invest your way

Not working with us yet? Find a J.P. Morgan Advisor or explore ways to invest online.

Editorial staff, J.P. Morgan Wealth Management