Why setting up recurring transfers could be an effective investing strategy

Editorial staff, J.P. Morgan Wealth Management

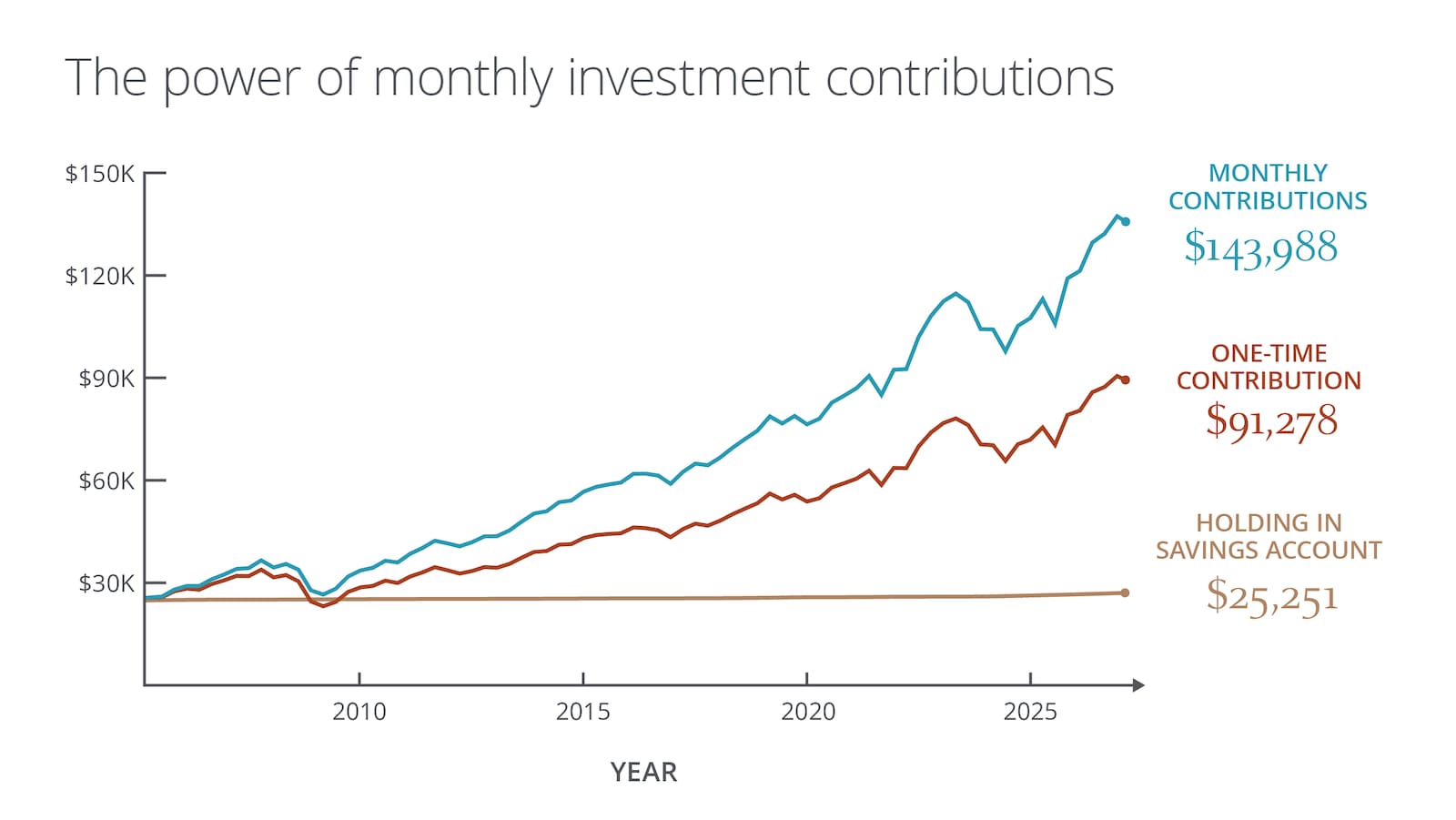

- Recurring transfers can be a great way to help you make steady progress toward long-term goals like building up an investment portfolio.

- By automating investments, you may be able to take the emotion out of investing.

- Regular contributions can also help you take advantage of dollar-cost averaging.

Be kind to your future financial self. How? One way to do that is by investing at a regular cadence.

Recurring transfers are automatic transfers set up between your bank accounts and your investment accounts. These transfers can be simple to set up online, and they can help you stay on track with your financial strategy by removing the need to move money manually between accounts.

Think about it like a garden: Regular seed planting, watering and soil checks help facilitate consistent growth, and your garden may ultimately blossom into a bountiful plot over time. You can apply the same concept to your investments.

Common types of recurring transfer strategies investors use

Fortunately for investors, there are many ways to utilize recurring transfers as an investment strategy. Consider the following options to determine which may be best for you:

- Periodic investment plans (PIPs): A fixed amount of money is invested at regular intervals (like monthly or quarterly) into mutual funds, stocks or other investment vehicles. This may involve setting up automatic transfers from a bank account.

- Dividend reinvestment plans (DRIPs): Instead of receiving dividends as a payout, the investment account holder’s dividend earnings are reinvested into additional shares of stock, an exchange-traded fund (ETF) or a mutual fund. This is often considered a recurring transfer because the investment is automatic.

- Payroll deductions: Offered by some employers, payroll deductions allow individuals to take a portion of money from their paychecks – likely pre-tax –and have it directly deposited into their employer-sponsored retirement account.

Get up to $1,000

When you open a J.P. Morgan Self-Directed Investing account, you get a trading experience that puts you in control and up to $1,000 in cash bonus.

Payroll deductions | Periodic investment plans (PIPs) | Dividend reinvestment plans (DRIPs) |

|---|---|---|

Description | ||

Likely pre-tax deductions from paychecks are used to build an investment account over time | Investments are made at regular intervals | Dividends are reinvested into more shares of stock, a mutual fund or an ETF |

Common uses | ||

To invest in an employer sponsored retirement plan | To invest in mutual funds, stocks and other vehicles | To invest dividend income in more shares of that dividend-paying investment |

Potential benefits | ||

Consistent contributions; dollar-cost averaging | Consistent contributions; dollar-cost averaging | Dollar-cost averaging; compounding growth |

Potential benefits of utilizing recurring transfers to invest

Setting up recurring transfers may provide several advantages to investors. Let’s walk through some of them.

Automation

Setting up recurring transfers can ensure you’re regularly adding to your investment portfolio, where your money may grow and benefit from the power of compounding over time. This approach may not only simplify the contribution process but can also help you stay committed (while reducing the need for manual effort on your part). By automating, you can shift your focus to other aspects of your strategy while knowing your investments are steadily building.

Taking the emotion out of investing

Recurring transfers may help to take the guesswork and emotion out of deciding when to invest, though you’ll still need to manually select the investments benefitting from your recurring transfers, including a PIP.

Dollar-cost averaging

These regular investments can help you benefit from dollar-cost averaging: If you’re a steady buyer, the cost of investments could ultimately average out over time, meaning you’ll acquire fewer shares when the market’s expensive and more when it’s cheap.

Time savings

You’ve heard it before, and it’s true: Time is money! Figuring out how much money to invest, along with how much to put toward bills or spend on discretionary items, can take a lot of time. By setting up recurring transfers as an investment strategy, you can save yourself the work of tinkering with your budget every time you want to add to your investments.

Help with large investments

Recurring transfers may also work well when it comes to larger additions you want to make to your investment portfolio, like after you receive bonus or large gift. If you know you want to invest a sizeable amount but aren’t sure how and when to do so, then coming up with a plan – say, contributing equal amounts over three months – can help you take advantage of the benefits of dollar-cost averaging. By spreading out your investments over time, you’ll reduce the risk of investing a large sum at an unfavorable time. While there are benefits to this approach, there are also downsides to consider as you may see a higher return by investing a lump sum all at once.

Potential drawbacks of utilizing recurring transfers to invest

Recurring transfers can also have their drawbacks, and investors need to be aware of them. Here are a few to consider:

Lack of flexibility

If you've set up recurring transfers into an investment account, it is important to stay aware so you can adjust as necessary. The last thing you want is to be faced with an unexpected increase in expenses (or decrease in income) and not have evaluated your ongoing transfer amounts.

Over-automation risks

Automation is great until it isn’t. It can often breed complacency, so stay on top of your transfers. You should always understand how they align both with your overall goals and with current market conditions.

Fees and costs

Some financial institutions charge fees for setting up or maintaining transfers, so be sure to know what those fees are and factor such costs into your investment strategy.

How to set up recurring transfers into an investment account

Begin by selecting the accounts involved in the transfer and decide on the frequency, such as weekly, biweekly, monthly or something else. Next, assess your budget to figure out how much you can comfortably transfer at that regular interval. Consider starting small and working your way up. It may be helpful to streamline the whole process by doing it online.

Common mistakes to avoid if you set up recurring transfers

No investment strategy is foolproof, no matter how simple it may seem. Neglect, disregard and oversight are some of the pitfalls often associated with recurring transfers. When you set up transfers, be sure not to forget about them.

Stay vigilant when your financial situation changes and adjust your transfers accordingly.

Lastly, be aware of any fees associated with recurring transfers because they can add up over time.

The bottom line

Setting up recurring transfers may be fairly straightforward, but the potential long-term impact on your portfolio can be significant. By automating these transfers, you can remove the guesswork from investing – and help build investment growth and improve your financial discipline in the process.

Once you’re comfortable with the basics of recurring transfers, you can consider further integrating, targeting and adjusting them to suit your needs, too. For example, combining your transfers with other financial tools like budgeting apps can help you better visualize where your money is going from a macro perspective. Or maybe you want to focus your transfers on a specific aim, such as retirement or education, so you can realize your goals more efficiently. Tweaking the transfer amounts – and their frequency – as your financial situation evolves is yet another easy way to help maintain flexibility.

You also might want to consider consulting with a financial advisor to ensure your strategy aligns with your overall financial goals.

Invest your way

Not working with us yet? Find a J.P. Morgan Advisor or explore ways to invest online.

Editorial staff, J.P. Morgan Wealth Management