4 reasons investors may benefit from staying invested

Global Investment Strategist

- "Stay invested" is a piece of financial advice you've probably heard many times.

- While it’s true that past performance is not indicative of future results, we’ve identified four reasons why it may be beneficial over the long term to stay invested.

- Ultimately, diversification, time spent in the market and a steady head can guide investors toward achieving their long-term financial goals.

“Stay invested” may sound like just another financial cliché, given how often we say it. But history shows that it may be one of the most important pieces of advice when it comes to growing your capital over the long run, in both good times and bad. Maybe you’re still thinking, “Well, if I time the market correctly, then surely I’m better off dodging the downturns and getting back in for the recovery.” That logic could work, but it is contingent on getting two things right: when to sell and when to buy back in. The odds of nailing both are, frankly, a shot in the dark.

If you’re still skeptical, stay with us. While past performance does not guarantee future returns, here are four pieces of evidence that reveal how staying (or getting) invested can potentially reward long-term investors.

Get up to $1,000

When you open a J.P. Morgan Self-Directed Investing account, you get a trading experience that puts you in control and up to $1,000 in cash bonus.

Reward can outweigh risk

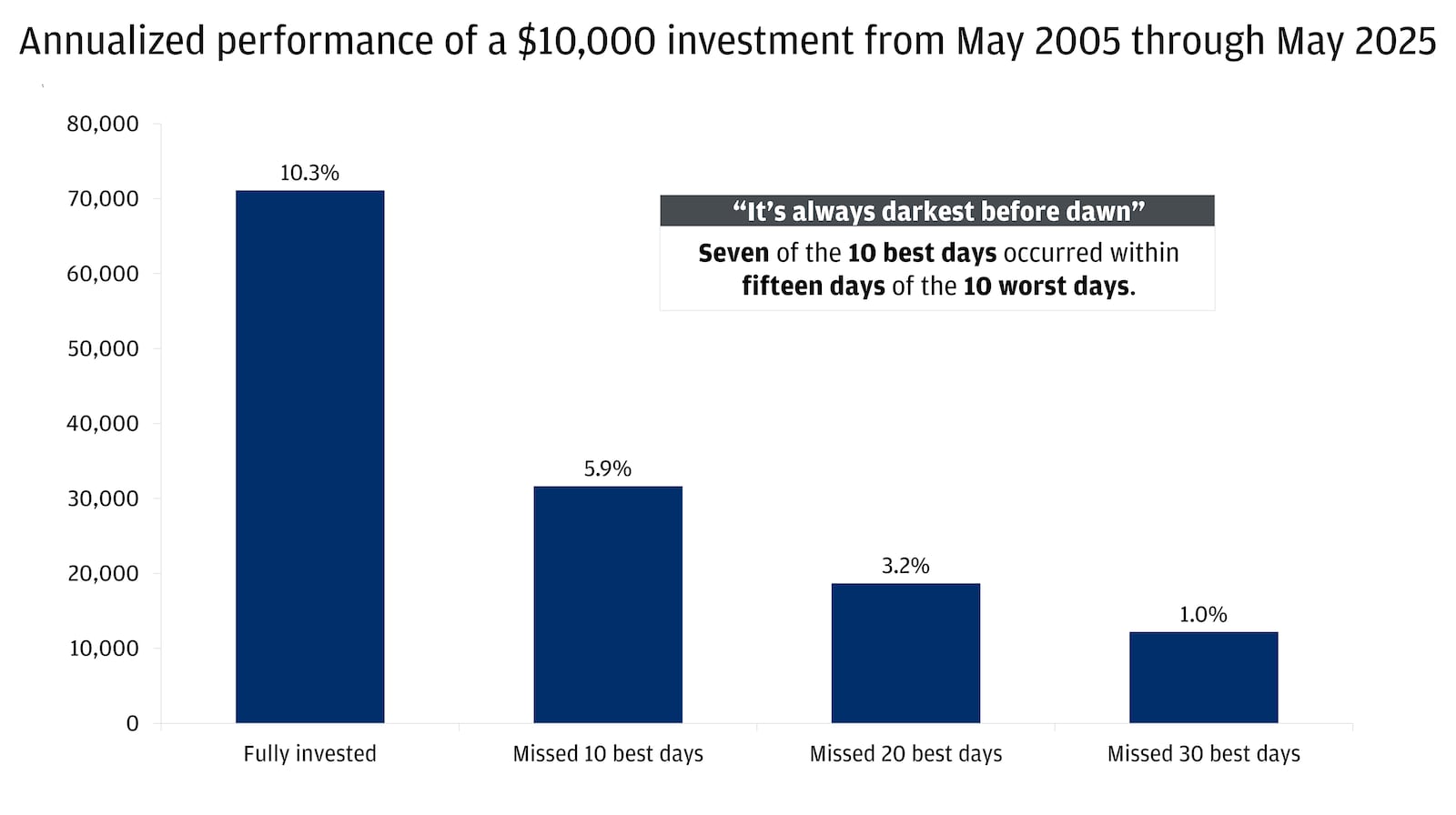

The next time market volatility feels scary enough to make you second-guess your long-term investment strategy, take a moment to consider your options before exiting the market. There is a possibility you might miss some of the best days in markets, and if you do, you are at risk of losing out on critical growth opportunities, with potentially significant consequences. The annualized performance of being fully invested in the S&P 500 over the last 20 years would have offered an average annualized return of 11.3%. But if you missed just 10 of the best days, your return would have been cut by more than half.

Performance of the S&P 500: Missing the best days

Past performance is no guarantee of future results. It is not possible to invest directly in an index.

The above is a hypothetical example for illustrative purposes only and should not be relied upon in making an investment decision. These examples do not reflect actual or future performance results of any specific vehicle, and are based solely on the hypothetical illustration cited.

Time horizon matters

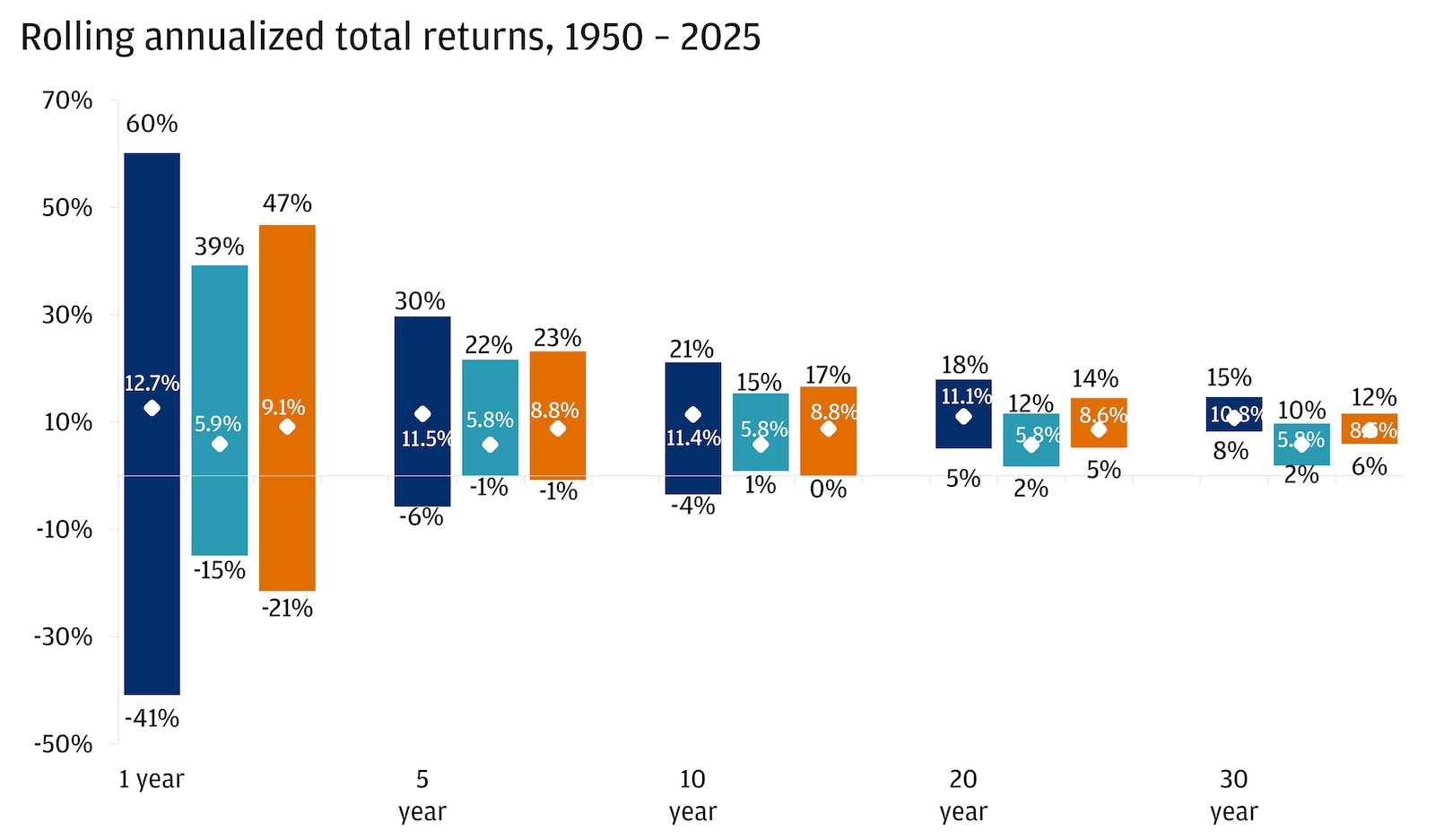

The longer you stay invested, the more confident you can feel about the probability of generating a positive return. While markets can always have a bad day, week, month or even year, history suggests that investors have been less likely to suffer losses over longer periods – especially with a diversified portfolio. While 12-month stock returns have varied widely since 1950 (from +60% to a whopping -41%), a 60/40 blend (60% stock and 40% bond allocation) has only suffered a -1% annualized return over any five-year rolling period in the data set. And the longer you stay invested, the smaller the range of outcomes.

Range of stock, bond and blended total returns

Past performance is no guarantee of future results. It is not possible to invest directly in an index.

All-time highs don’t alter the outcome

Now you may be thinking: “I get it. Volatility is normal. Long-term investors are rewarded for weathering the storm. But what about all-time highs? I should reap my rewards when things can’t get better than that.” Regardless of where the equity market stands, near an all-time low or an all-time high, longer-term outcomes actually aren’t all that different. History reveals that if you invested at an all-time high, your average return in the S&P 500 three months later is 2% and one year later is 14%. If you invested on any day, your average return is relatively similar at 3% and 12% respectively. Any way you slice it, it is often worth it to get invested and stay invested.

You’ll always have something to worry about

In 2020, worries centered on COVID-19 and the U.S. presidential election. In 2022, it was inflation and rapidly rising interest rates. Today, investors are weighing tariffs, geopolitical conflict, questions about the path of interest rates and the market impact of artificial intelligence. Reminding yourself what investors have been through, and where we are today, is important. Since the start of 2020, around the onset of COVID-19, a 60% stock and 40% bond allocation has, in some cases, returned more than 70% cumulatively. It’s not about dismissing prevailing risks, but more so about remembering that markets tend to focus on fundamentals over time.

At the end of the day, staying invested and sticking to a long-term plan may help investors to avoid emotionally driven decision-making that can result in poorly timed mistakes. Diversification, time in the market and a steady hand may play a part in achieving your long-term financial goals.

Diversification does not guarantee a profit or protect against a loss.

Invest your way

Not working with us yet? Find a J.P. Morgan Advisor or explore ways to invest online.

Global Investment Strategist