How to pay yourself as a business owner

You put in the work, and now it’s time to pay yourself. Learn your options. Presented by Chase for Business.

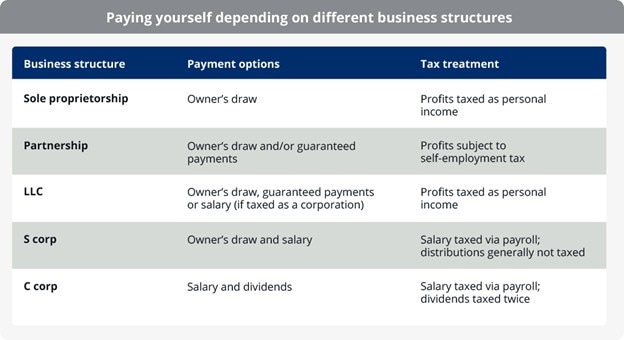

- As a business owner, you can pay yourself via an owner’s draw (where you withdraw profits from your company as needed), a W-2 salary or a combination of both.

- Knowing how to pay yourself from an LLC depends on whether your business is taxed as a corporation, which requires a “reasonable” W-2 salary matching industry standards, or as a standard LLC that uses owner’s draws.

- No matter which way you decide to pay yourself, it’s important to thoroughly review the pros and cons and steer clear of common mistakes to stay compliant.

As a committed business owner who works hard to expand your products and services, improve infrastructure and prioritize vendors and employees, you could be forgetting to invest in one of your most important assets: yourself. Whether you’re just getting started or already running a thriving business, you still need to get paid for your hard work — and you have options for how to do it.

This guide will provide you with helpful insight into the different methods of owner compensation, while breaking down the specific tax implications and benefits of each to help you choose the best option for your business.

Ways to pay yourself: Owner’s draw vs. salary

Generally, there are two ways to pay yourself as a business owner: an owner’s draw or a salary. Choosing between these methods — or using a combination of both — largely depends on your business-ownership model and your understanding of the unique advantages and tax implications of each option.

Salary

Taking a salary means you’re on your own business payroll as a W-2 employee. You receive a regular, recurring payment taxed as income by state and federal governments just as you would at any other company.

Best for: S corporations, C corporations or limited liability companies (LLCs) taxed as corporations

Tax forms: The business issues you a Form W-2 annually, and the business files Form 941 (Employer’s Quarterly Federal Tax Return).

Note: A “reasonable salary” is a legal requirement for S corporation owners and LLCs that elect S Corp status. Sole proprietors and single-member LLCs cannot pay themselves a W-2 salary. You should consult with a tax professional for guidance.

Pros:

- Business budgeting: A salary adds a stable, recurring expense into your business costs.

- Personal finances: It’s easier to track income and expenses.

- Simplified taxes: Taxes are deducted up front.

- Incentivized performance: You have the option to be paid based on a percentage of profits.

Cons:

- “Reasonable compensation” risk: If your salary is too low to not pay taxes, you risk an audit. Your salary must match “the value that would ordinarily be paid for like services by like enterprises under like circumstances,” according to the IRS guidance on paying yourselfOpens overlay. For a starting point, research what it would cost you to hire someone to do your exact job.

- Cash-flow upkeep: There’s a risk of salary instability if profits aren’t as projected. A salary and its taxes must be paid consistently regardless of cash flow.

- Tax liability: Your pay is taxed as ordinary income and includes mandatory deductions for Social Security and Medicare.

Owner’s draw

An owner’s draw, sometimes referred to as a distribution, is how most small business owners financially compensate themselves. With this method, you draw money from business profits by transferring funds to your personal account as needed. The IRS views owners of these entities as self-employed individuals rather than employees.

Best for: Sole proprietorships and partnerships

Note: For partnerships, this may include guaranteed payments, which provide partners with a fixed income regardless of the business’s current profitability.

Tax forms: Draws are reported on Schedule C (for sole proprietors) or Schedule K-1 (for partnerships and LLCs) as part of your annual tax return. Form 1040-ES is used to pay your quarterly estimated taxes.

Note: You won’t pay taxes on every draw, but it’s wise to set aside money to pay your estimated quarterly tax bill.

Pros:

- Earning potential: Your salary is flexible and can fluctuate depending on how your business is performing.

- Flexible income: You can withdraw once or multiple times using the same or different amounts.

- Reduced administrative work: You won’t need to manage a formal payroll system, withhold taxes or pay unemployment insurance for yourself.

Cons:

- Tax planning: You need to budget for a quarterly tax bill since taxes aren’t deducted up front.

- Equity reduction: An owner’s draw limits funds available for future business reinvestment or expenses.

- Self-employment (SE) tax: You are responsible for the full 15.3% SE tax on 100% of your business profits because, unlike a salary, draws aren’t subject to payroll withholding.

Combined method

Combining both methods — salary and owner’s draw — means you’re paid as both an employee with a W-2 salary for your daily work and as a shareholder with additional profit as distributions. Paying yourself a reasonable salary based on your role and industry can satisfy IRS requirements, allowing you to pay self-employment taxes only on your salary while taking the remaining profit as tax-free distributions.

Best for: S corporations and LLCs taxed as S corps

Tax forms: You’ll receive a W-2 for your salary and a Schedule K-1 for your distributions.

The business must file Form 1120-S to report these payments to the IRS.

Pros:

- Tax savings: By splitting your income, you pay the 15.3% self-employment tax only on the salaried portion.

- Adjustable income: You receive a steady paycheck with the flexibility to take more funds when the business performs well.

Cons:

- IRS compliance: Your salary must be justifiable as “reasonable” for your industry before you take any profits as distributions.

- Meticulous tracking: You need a payroll system for the salary and accurate bookkeeping for the distributions to stay compliant and reduce the risk of an audit.

Factors to consider while determining how much to pay yourself

There is no one-size-fits-all answer to how much to pay yourself, and no matter which route you choose — salary, owner’s draw or both — it can be difficult for business owners to determine a fair amount. While there are no universal statistics for the “perfect” salary, taking the following factors into consideration can help you find the ideal amount for you, striking a balance between your business requirements, legal requirements and personal needs.

- Business structure: Before you can decide on how much to pay yourself, your legal framework determines whether you can take a salary, distributions or a combination.

- Legal and regulatory considerations: For S corps and C corps, you must follow “reasonable” compensation rules based on your role and industry to lower the possibility of IRS review that puts you at risk for an audit.

- Industry standards: Research the amount it would actually cost to hire someone else to do your job. The Bureau of Labor Statistics can help you find your benchmark or “true wage.”

- Business health check: Assess your company’s overall financial health. Your take-home pay should depend on your net profit (gross revenue minus all expenses) to make sure you can continue covering all business costs.

- Safety net: Calculate your cash flow and keep enough aside to cover at least 30 days’ worth of expenses for unexpected business disruptions.

- Personal financial needs: Add up your nonnegotiable costs, like your mortgage, groceries and health care. This is your “minimum viable” pay needed to prevent personal financial stress.

- Tax cuts: Account for the 15.3% self-employment tax or payroll taxes, which will reduce your actual take-home pay.

- Future planning: Before deciding your take-home pay, set aside money for developments and improvements like new tools, marketing campaigns or vendors.

- Leadership image: Taking a high salary while the business is struggling can send a negative signal to investors or your team, whereas a transparent, fair amount demonstrates you’re a responsible leader.

Mistakes to watch out for while paying yourself as a small business owner

Once you’ve decided the correct method and amount to pay yourself, it’s important to be aware of the mistakes that go beyond simple accounting errors and may harm your long-term growth and personal well-being. Here are tips for reducing the risk of common pitfalls:

- Don’t mix finances: Keep personal and business accounts separate to reduce the risk of being held personally liable for business debts. Using business accounts for personal expenses or routing business income into personal accounts can also cause accounting complications that may hurt your credit and your ability to secure business loans.

- Don’t ignore tax requirements: With owner’s draws, taxes aren’t deducted up front. It’s best practice to set aside funds for quarterly estimated taxes so you won’t face underpayment penalties from the IRS and a much larger annual tax burden.

- Keep your payments consistent: Large, irregular withdrawals can destabilize your business financially and affect expenses and payroll. It’s a good idea to treat your financial compensation as a recurring expense.

- Don’t forget about retirement planning: If you don’t have money automatically deducted from your paycheck and invested in an employer-sponsored 401(k) plan, it’s smart to reserve a percentage of your pay for a SEP-IRA or Solo 401(k) to help prevent your money being tied up in a non-liquid business at retirement.

- Document everything: Keeping accurate, real-time records of all salary and draw payments can help simplify taxes, provide a clear audit trail and boost potential investors’ positive perceptions of the business.

FAQs about business owner compensation

Questions about how to pay yourself as a business owner? We can help.

How do you pay yourself from an LLC?

For a standard LLC, you take owner’s draws since you are considered a business owner rather than an employee. However, if your LLC is taxed as an S corp, you can receive a W-2 salary in addition to distributions.

How do you pay yourself from an S corp?

You can use a combined method of paying yourself a reasonable salary and shareholder distributions. Self-employment taxes apply only to the salaried portion of your take-home pay, which can lead to significant savings on taxes.

How do you pay yourself as a sole proprietor?

Because you and your business are treated as the same legal and tax entity, you can pay yourself only through owner’s draws and must pay self-employment taxes on your full net profit.

Can you take a salary and an owner’s draw at the same time?

Yes, but only if your business is a corporation or an LLC taxed as a corporation.

What is the most tax-efficient way to pay yourself as a small business owner?

If you are taxed as an S corp, the most tax-efficient way to pay yourself is to split your income by draws and a salary. Because you are considered both an employee and a shareholder, this method can greatly reduce self-employment taxes.