What is a bond yield?

Editorial staff, J.P. Morgan Wealth Management

- Bonds offer investors a way to lend money to governments or corporations in exchange for periodic interest payments and the return of the principal at maturity.

- A bond's yield represents an investor's expected return, considering the remaining interest payments and current bond price.

- Bond yields fluctuate with market conditions, interest rates, economic trends and changes in the issuer's financial health.

What is a bond?

Think of a bond as a financial tool that allows you to lend money to a corporation or government. When you buy a bond, you're essentially giving a loan to the issuer, who promises to pay back the principal amount at a later date, known as the maturity date. The issuer also agrees to pay you interest on the loaned funds.

This interest, expressed as a percentage of the principal, is called the coupon rate. Coupon rates can be fixed or floating, linked to a policy rate. Some bonds, like short-term Treasury bills, don't pay annual interest but are issued at a discount to the principal value of the bond. Let’s take a more detailed look at how bond yields work and if they may be suitable for your portfolio.

Bond yields: Key terms

To better understand bond yields, here are a few key terms to know first:

- Bond coupon rate: The interest rate paid by the bond’s issuer.

- Annual coupon payment: The total amount of interest paid to the bondholder each year.

- Bond yield curve: A graph that plots the yields of similar-quality bonds against their maturities.

- Yield to maturity: The total return anticipated on a bond if held until it matures, considering both interest payments and capital gains or losses.

Get up to $1,000

When you open a J.P. Morgan Self-Directed Investing account, you get a trading experience that puts you in control and up to $1,000 in cash bonus.

How do bond yields work?

Now, let's talk about bond yields. Yield is the potential return on investment for owning a specific bond. It's a calculation that considers the bond's price – whether it's trading at a premium or discount to its original face value – in relation to the coupon payments. The bond issuer pays the coupon as a percentage of the original face value consistently throughout the bond's lifetime. The final principal paid at maturity also stays the same. So, your yield, or potential return, on buying a bond's coupon and final payments increases or decreases with the purchase price. In simpler terms, it's your expected annual return on investment.

Understanding the inverse relationship between bond prices and yields is key. As bond prices increase, yields decline, and vice versa. Consider a single year of interest payments. If you have a bond that pays you $50 in interest this year, buying it for $900 instead of $1,000 increases the percentage of return on your investment. You can also think about it from the perspective of holding the bond to maturity. The potential return from purchasing a bond at a discount is higher because you'll receive the entire principal back at maturity in addition to the coupon payments along the way. If you purchase a bond at a premium to its face value, you lose that additional amount you overpaid for the principal. So, the more you pay upfront for the bond, the lower your total return when the bond matures and you receive the original principal.

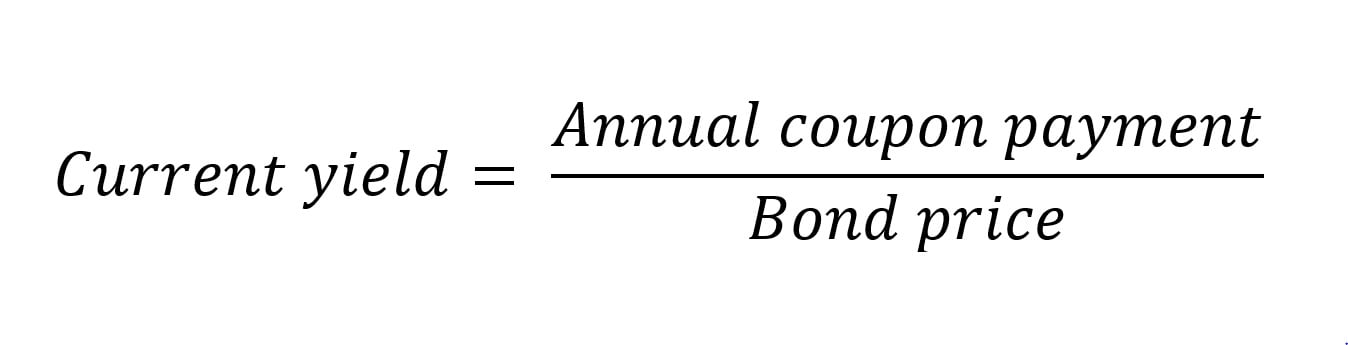

How do you calculate a bond yield?

To calculate your bond's current yield, divide the annual coupon payment by the bond price.

However, keep in mind that this calculation doesn't provide the most accurate measure of a bond's return because it overlooks the time value of money, maturity value and payment frequency. These factors all affect the bond's yield. For a more comprehensive measure, investors often use the yield to maturity, which factors in the bond's remaining lifetime and the present value of all remaining cash flows. Despite its limitations, calculating the current yield can offer a helpful estimate.

Other types of bond yields

Bond yields can be measured in a few ways to provide different insights into the bond’s performance and potential returns.

Nominal yield

The nominal yield, also known as the coupon rate, is the interest rate that the bond issuer agrees to pay bondholders. These rates are fixed and do not change throughout the life of the bond.

Current yield

Current yield is calculated by dividing the bond’s annual coupon payment by its current market price. This approximates what the bond is currently yielding. The current yield can fluctuate based on market conditions.

Yield to call

The yield to call is the yield calculated to the first callable date, rather than the maturity date. This may be important for bonds that can be “called” or repurchased by the issuer before they mature, typically at a premium price.

What can affect the price of a bond?

Bonds are market-based securities, so their prices are a factor of supply and demand. As with stocks, any number of factors can affect demand for a particular bond in the short term, from inflation expectations to market liquidity, economic events or general investor sentiment. The main two components that provide the foundation of a bond's yield are benchmark risk-free interest rates and the issuer's credit risk.

Lenders determine a borrower's initial interest rate by taking a benchmark risk-free lending rate, like U.S. Treasury bonds, and marking it up based on the borrower's riskiness. If I can lend to the U.S. government with less risk for 10 years at 4% interest, you'll have to pay a higher rate to compensate me for the extra risk of late payments or default. Once the bond is out on the market, those same factors influence the perception of the value of an issuer's debt.

Benchmark interest rates, like those on U.S. Treasury bonds, move with the perception of broader economic growth and liquidity trends, fiscal spending decisions or monetary policy changes. As broader interest rates rise, bond prices fall. This is because if you own a Treasury bond that pays a 3% coupon, but new Treasury bonds start paying 4% interest, your bond is relatively less attractive. To be able to sell your Treasury bond, you'll need to discount the price enough to turn your 3% coupon bond into a 4% yield.

Changes in the issuer's credit rating can also affect the bond's price. If it looks like the company you're lending to might default or miss an interest payment, the riskiness of holding that bond increases, and the investment becomes less attractive. The yield rises with the declining price to reflect the higher potential return for greater risk.

Changing yields represent the bond’s potential return on investment increasing or decreasing based on the perceived risk and opportunity of holding the bond to maturity.

Ready to invest?

Understanding bond yields is crucial – they reflect your potential return, changing with market conditions, interest rates and the issuer's creditworthiness. Bonds can balance your investment portfolio, offering a mix of risk and reward that suits your financial goals. Whether you're new to bonds or looking to deepen your investment strategy, consider connecting with an advisor today at J.P. Morgan Wealth Management to enhance your understanding and make informed choices.

Frequently asked questions about bond yields

High-yield bonds are just what they sound like – bonds with a higher yield relative to the rest of the market. These elevated yields act as a warning sign for investors. Higher relative interest rates often indicate a greater risk of the issuer defaulting on the loan. That's why high-yield bonds are often called junk bonds.

Lenders derive a borrower's rate by taking a baseline risk-free rate, like lending to the U.S. government, and marking it up based on the riskiness of the borrower. This compensates them for the higher possibility of losing their money. The greater the spread above the risk-free rate, the riskier the investment. These risky issuers could be corporations, developing nations or troubled local municipalities. A qualified financial advisor can help you determine if high-yield bonds might be suitable for you.

The four main types of bonds are:

- Government bonds (issued by national governments)

- Corporate bonds (issued by companies)

- Municipal bonds (issued by state and local governments)

- Agency bonds (issued by government-sponsored entities)

Each bond type has its own associated levels of risk, return and tax implications.

While the best time to buy bonds depends on your personal financial situation and investing goals, investors tend to increase their allocations to bonds in anticipation of economic uncertainty, market volatility, falling interest rates or greater income needs. However, trying to time the market is often advised against. Bonds' fixed income and principal return qualities make them a relatively lower-risk investment and valuable portfolio diversifier.

You can buy Treasury bonds directly from the U.S. government on TreasuryDirect by creating an account, selecting the bond type and placing an order. Alternatively, you can purchase them through a brokerage account like any other investment. Ensure the bonds match your goals and be aware of any fees or minimum purchase requirements.

Invest your way

Not working with us yet? Find a J.P. Morgan Advisor or explore ways to invest online.

Editorial staff, J.P. Morgan Wealth Management