CHASE BUSINESS CREDIT JOURNEY℠

Do you know your business credit scores?

Meet Business Credit Journey, a complimentary service accessible directly from your business banking account that can help you better understand your credit health. Learn your Dun & Bradstreet® business credit scores, receive alerts when they change and view insights on how to improve them.

Screen image simulated

Take control of your business credit

Business Credit Journey helps you keep an eye on your business credit scores right from your Chase for Business account.

Be among the first to experience Business Credit Journey.

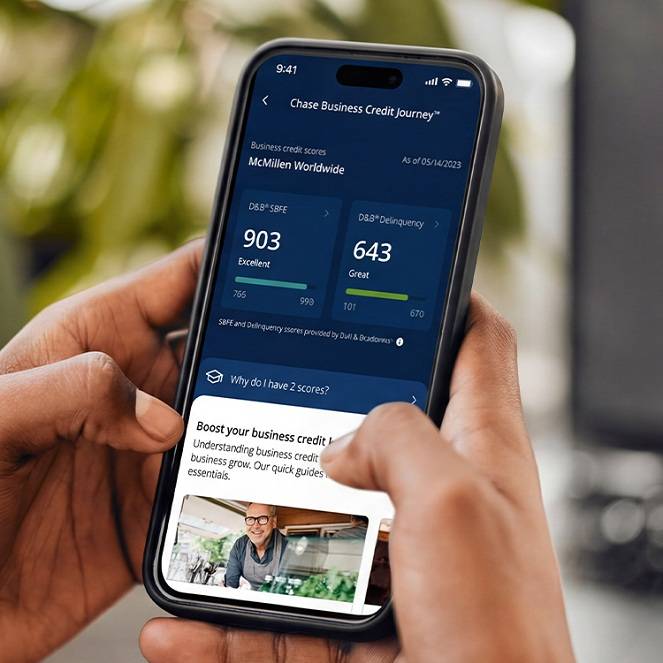

Know where you stand

Enroll and see scores without impacting your credit.

Score change alerts

Get alerts about score changes so you can stay on top of your credit profile.

Boost credit know-how

Understanding business credit can be key to helping your business grow. Our quick guides provide the essentials.

Why business credit matters

- Strong scores can help you get the money you need to run and grow your company

- Monitoring your credit can help alert you early to fraud or identify theft

- Your business credit profile is like your company’s resumé — and unlike personal scores, anyone can view it, as long as they’re willing to pay for it

- Good scores can help improve your credibility with lenders and potential vendors or partners

- Enhance your competitive advantage to influence potential partners/vendors relationships

- Building your business credit can help protect your personal assets from business liabilities, typically only with an LLC structure

Why do I have two business credit scores?

With Business Credit Journey, you receive two business credit scores, both providing insight into financial health, but differing in factors, calculations and ranges.

Dun & Bradstreet® Small Business Financial Exchange Score

Measures how reliably your business meets credit obligations.

Reflects your business’s credit performance and payment behaviors based on data from lenders and banks.

Score range: 706-999

Dun & Bradstreet® Delinquency Predictor Score

Measures the likelihood your business will pay bills late or miss payments.

Indicates how likely your business is to become severely delinquent on payments within the next 12 months.

Score range: 101 to 670

Help & Support

Find answers to questions about your business credit scores, how to contact customer service and more.

General information

You must have an existing Chase Business Checking or Business Credit Card relationship and be a single ownership business.

No. Business Credit Journey is a complimentary service accessible directly from your business banking account.

To update your contact info and other personal details, go to Profile & Settings. On mobile, choose the “Settings” tab and then “Personal details.” On desktop, choose “Personal details.”

If you want to stop using Business Credit Journey, you can unenroll.

Credit monitoring

You’ll find two scores in Business Credit Journey, including the Dun & Bradstreet® (D&B) Small Business Financial Exchange (SBFE) Score and the D&B® Delinquency Predictor Score. Your lender (including Chase) may not use the models provided in Business Credit Journey, so don’t be surprised if they provide a score that’s different from your D&B SBFE Score or your D&B Delinquency Predictor Score.

Unlike personal credit scores, business credit scores don’t share a common rating scale that goes from 300 to 850. They vary widely based on the bureau, and different credit scoring models may be used by lenders and insurers. This makes it harder for a business owner to know where their credit stands when they’re only seeing one of many available scores. In Business Credit Journey, we supply two of the more widely available Dun & Bradstreet scores.

No. We access your credit information using a soft inquiry, also known as a soft credit check, which may show up on your credit report but will not affect your scores. You can check your scores at Business Credit Journey as many times as you want without affecting them.

Lenders, suppliers, insurance underwriters and other organizations may use business credit scores to help make decisions about working with your business.

We recommend checking your scores regularly to keep track of your credit activity.

There are many factors that can influence your business credit scores. Four of the more critical factors include your payment history, the amount of credit you use, any publicly available records and legal filings involving your business, and the number of tradelines you maintain.

Yes, each unique legal business entity has its own business profile and scores.

If you don’t see a credit score when you sign in to Business Credit Journey, it may be because you’re currently building your credit and may not have enough history yet.

Dun & Bradstreet scores

The D&B SBFE Score is designed to assess your business’s overall financial health. It ranges from 706 to 999, where 999 is the “best” score (signifying a lower risk to lenders) and 706 is the “worst” score. The scoring model is calculated using data collected by D&B and data provided by the Small Business Financial Exchange (SBFE).

The D&B Delinquency Predictor Score is designed to assess the likelihood that your business will pay on time in the next 12 months. It ranges from 101 to 670, where 670 is the “best” score (indicating a greater possibility your business will pay on time) and 101 is the “worst” score. The scoring model is calculated using data collected by D&B.

You’ll need a Dun & Bradstreet D-U-N-S® Number to receive scores and reports from Dun & Bradstreet. You can register for one at their website.

To get a D-U-N-S Number, you can apply online through Dun & Bradstreet.

Generally, D&B calculates scores by analyzing information provided by your business, as well as by suppliers and lenders who report your payment information to D&B. D&B also looks at public records related to your business, such as regulatory requirements, legal filings or business tax reports. Each unique D&B credit score has its own scoring model.

There are several possible reasons why data may not be showing up in your score history. Score history data won’t display until you’ve visited Business Credit Journey during at least two of the past six months. Additionally, if you don’t visit Business Credit Journey during a calendar month, you won’t see a score for that month in your score history data. Another possible reason is that your D-U-N-S Number is under review or has changed. You can find out more about your specific situation by contacting Dun & Bradstreet.

Support

If you have questions about your scores, contact Dun & Bradstreet.

If you find a mistake, you’ll need to contact Dun & Bradstreet to let them know. The mistake could be due to a credit bureau reporting error.

Business Credit Journey is only intended for use by the owner of this business or an authorized representative. If this is not your business, please unenroll and contact Dun & Bradstreet to resolve the issue.

There are several reasons why data might be unavailable. You can find out more about your specific situation by contacting Dun & Bradstreet.

Not a Chase for Business customer?

Explore checking and credit card options to choose which fits your business needs.

Chase Business Complete Banking®

Chase business credit cards