Page has Error(s).

| ECM Approval Code | Adtrax or Nexus Approval Code | Business Approver | Content Owner(Email) | Jira # or Project Name | LOB Review Date | Manual QA Date | Manual QA Reviewer SID | Manual QA JIRA Ticket # | Manual QA ADA Testing |

|---|---|---|---|---|---|---|---|---|---|

| n/a | 3489915 | Guerra, Maxwell | maxwell.guerra@jpmorgan.com | CWO-132878 CWO-134499 CWO-135982 CWO-138562 | Jun 17, 2024 | May 06, 2024 | V028129 | CWO-132878 | true |

Article

Headline: Quick shot: Bank lending standards suggest a deep U.S. recession is very unlikely

Eyebrow: Top Market Takeaways

Blurb:

One year ago, investors were concerned that a handful of regional bank failures and rising interest rates would lead to a U.S. recession by the end of 2023.

By Line:

Publish Date: May 07, 2024

Last Modified Date:

Expiration Date: May 01, 2029

Redirect URL: https://www.chase.com/personal/investments/learning-and-insights/category/markets

302 Redirect: false

Content Type: regular

Time to Read:

Link to PDF:

Collection Image:

tmt-may-seven-twenty-four-daily-415x233.jpg Thumbnail Image

desktopLarge

415x233

desktopMedium

415x233

tablet

415x233

mobile

415x233

Collection Image AltText: Top Market Takeaways Quick Shot

Collection Image Large:

tmt-may-seven-twenty-four-daily-2560x1440.jpg Thumbnail Image Large

desktopLarge

766x430

desktopMedium

629x353

tablet

736x413

mobile

375x210

Collection Image Large AltText: Top Market Takeaways Quick Shot

Hide Collection Image Large: false

Topics

- Markets

- Investment Themes

- Top Market Takeaways

- Navigating Market Volatility

Categories

-

Market Insights

(View/Edit Category)

Disclosures

- Quick shot: Taking the heat off (View/Edit Disclosure)

- Quick shot: Myth Busting 101: The Fed and election year moves (View/Edit Disclosure)

- Quick shot: A wonder of the investing world: compounding (View/Edit Disclosure)

Content

Content Type: section

Primary Header:

Secondary Header:

Description:

One year ago, investors were concerned that a handful of regional bank failures and rising interest rates would lead to a U.S. recession by the end of 2023. At last year’s May Federal Open Market Committee (FOMC) meeting, Fed Chair Powell stated that, “tighter credit conditions are likely to weigh on economic activity, hiring and inflation. The extent of these effects remain uncertain.”

Today, we are more certain. In 2023, the U.S. economy grew by 2.5% on a year-on-year basis, inflation rose by about 3.7% and nonfarm payrolls expanded by average of 251,000 each month. Unsurprisingly, Chair Powell’s comments at this year’s May FOMC meeting stood in sharp contrast to last year’s with the Chair stating that, “Recent indicators suggest that economic activity has continued to expand at a solid pace. Job gains remained strong, and the unemployment rate has remained low. Inflation has eased over the past year but remains elevated.” This improvement in sentiment and economic resilience may not have been possible had the regional banking crisis not been ringfenced so quickly.

Fortunately, policymakers did react, and bank lending standards to small firms have improved since mid-2023. While the latest Senior Loan Officer Survey (SLOS) did show a very modest tightening of standards for small firms, it also showed a marked improvement in bank willingness to lend to consumers. This should help to support consumer spending as the year progresses. With lending conditions typically leading economic growth by about two quarters, we believe that any economic slowing ahead will likely be much milder than what was anticipated just one year ago. Forward-looking equity markets have rightly reflected that.

Section Horizontal Line:

Content Type: section

Primary Header:

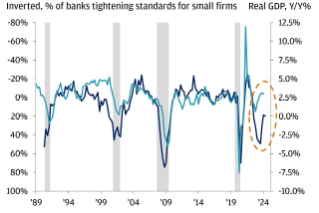

Lending standards have improved since mid-2023

Secondary Header:

Description:

Section Horizontal Line:

Secondary Images

Caption: Sources: Federal Reserve Board, Bureau of Economic Analysis, NBER, and Haver Analytics. Data as of 2Q 2024. Note: Gray shaded regions denote periods of U.S. recession.

Alt Text: This chart shows the percentage of banks reporting that they are tightening credit standards to small firms versus real U.S. gross domestic product (or GDP) from 1989 to 1Q 2024.

Long Form Text Description:

Inverted, percent of banks tightening standards for small firms - Real GDP, Year on Year percentage

This chart shows the percentage of banks reporting that they are tightening credit standards to small firms versus real U.S. gross domestic product (or GDP) from 1989 to 1Q 2024. The two data series are inversely correlated, meaning that as the percentage of banks reporting that they are tightening standards goes up, real GDP on a year-on-year basis goes down. When the percentage of banks reporting tighter standards rises above 20%, there tends to be a U.S. recession (which is highlighted on the chart). Right now, about 44% of banks are reporting that they are tightening credit standards. This implies that economic growth will likely trend lower from here. Particularly, if regional banks tighten credit further given the ongoing regional banking turmoil. The chart suggests that real GDP on a year-on-year basis could go negative in coming quarters, which would likely mark the start of a U.S. recession.

Recessions occurred from the first quarter of 1990 through the first quarter of 1991, then in the first quarter of 2001 through the fourth quarter of 2001, then again in the fourth quarter of 2007 through the second quarter of 2009, and most recently from the fourth quarter of 2019 through the second quarter of 2020.

The percentage of banks tightening was 52.7% in the second quarter of 1990 and then in the second quarter of 1992 it was -7.1% and then went to 45.5% in the first quarter of 2001 and then went to -24% in the second quarter of 2005 and then in the fourth quarter of 2008 it was at 74.5% and then in the second quarter of 2013 it was -23.1% and then it was 70% in the third quarter of 2020 as the pandemic set in, but then it improved sharply to -25.7% in the third quarter of 2021 as the economy improved and credit was widely available. Towards the end of 2022, banks began to tighten credit again as the Fed began to raise interest rates and then in the first quarter of 2023 the regional banking crisis started and made matters worse. By the third quarter of 2023, nearly 50% of banks where tightening standards to small firms. However, that trend has been improving as the supply-side dynamics led to a resilient and strengthening economy in the latter half of 2023. As of the second quarter of 2024, just 19.7% of banks reported tightening standards for small firms. Typically, a reduction in tightening occurs after an economic slowing, not after.

GDP was 4.31% in the first quarter of 1989 and then moved to -0.95% in the first quarter of 1991 and then moved to 4.12% in the fourth quarter of 1994 and then to 5.25% in the second quarter of 2000 and then to 0.17% in the fourth quarter of 2001 and then to 2.16% in the fourth quarter of 2007 and then to -4.00% in the second quarter of 2009 and then to 3.76% in the first quarter of 2015 and then to -8.35% in June of 2020 and then to 12.46% in the second quarter of 2021 and then down to 1.56% in March of 2023. Since then, real GDP has rebounded and was around 3% year-on-year as of the first quarter of 2024.

Content Type: section

Primary Header:

Secondary Header:

Description:

All market and economic data as of 05/06/24 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

Section Horizontal Line:

Content Type: ctaPublic

CTA:/content/site-services/articles/cta-library/en/invest-your-way-not-working-with-us-yet

Content Type: cta

CTA:/content/site-services/articles/cta-library/en/speak-with-a-jp-morgan-advisor-l1

Content Type: cta

CTA:/content/site-services/articles/cta-library/en/explore-more-ways-to-invest-online-l2